11. Appendiceal Topics#

This chapter is different from the rest because it is not about any specific topic. Instead it is a collection of different topics that provide support for the rest of the book by complementing topics discussed in other chapters. These topics are here for readers who are interested in going deeper into each of the methods and theory. In terms of writing style it will be a little bit more theoretical and abstract than other chapters.

11.1. Probability Background#

The Spanish word azahar (the flower of certain critics) and azar (randomness) are not similar out of pure luck. They both come from the Arabic language [1]. From ancient times, and even today, certain games of chance use a bone that it has two flat sides. This bone is similar to a coin or a two-side die. To make it easier to identify one side from the other, at least one side has a distinctive mark, for example, ancient Arabs commonly used a flower. With the passage of time Spanish adopted the term azahar for certain flowers and azar to mean randomness. One of the motivation to the development of probability theory can be track back to understanding games of chance and probably trying to make an small fortune in the process. So let us start this brief introduction to some of the central concepts in probability theory[2] imagining a 6-sided die. Each time we roll the die it is only possible to obtain an integer from 1 to 6 without preference of one over another. Using Python we can program a die like this in the following way:

def die():

outcomes = [1, 2, 3, 4, 5, 6]

return np.random.choice(outcomes)

Suppose we suspect that the die is biased. What could we do to evaluate this possibility? A scientific way to answer this question is to collect data and analyze it. Using Python we can simulate the data collection as in Code Block experiment.

def experiment(N=10):

sample = [die() for i in range(N)]

for i in range(1, 7):

print(f"{i}: {sample.count(i)/N:.2g}")

experiment()

1: 0

2: 0.1

3: 0.4

4: 0.1

5: 0.4

6: 0

The numbers in the first column are the possible outcomes. Those in the

second column correspond to the frequency with which each number

appears. Frequency is the number of times each of the possible outcomes

appears divided by N, the total number of times we roll the die.

There are at least two things to take note of in this example. First if

we execute experiment() several times, we will see that we obtain a

different result each time. This is precisely the reason for using dice

in games of chance, every time we roll them we get a number that we

cannot predict. Second, if we roll the same die many times, the ability

to predict each single outcome does not improve. Nevertheless, data

collection and analysis can actually help us to estimate the list of

frequencies for the outcomes, in fact the ability improves as the value

of N increases. Run the experiment for N=10000 times you will see

that the frequencies obtained are approximately \(0.17\) and it turns out

that \(0.17 \approx \frac{1}{6}\) which is what we would expect if each

number on the die had the same chance.

These two observations are not restricted to dice and games of chance. If we weigh ourselves every day we would obtain different values, since our weight is related to the amount of food we eat, the water we drink, how many times we went to the bathroom, the precision of the scale, the clothes we wear and many other factors. Therefore, a single measurement may not be representative of our weight. Of course it could be that the variations are small and we do not consider them important, but we are getting ahead of ourselves. At this point what matters is that the data measurement and/or collection is accompanied by uncertainty. Statistics is basically the field concerned with how to deal with uncertainty in practical problems and Probability theory is one of the theoretical pillars of statistics. Probability theory help us formalize discussion like the one we just had and extend them beyond dice. This is so we can better ask and answer questions related to expected outcomes, such as what happens when we increase the number of experiments, what event has higher chance than another, etc.

11.1.1. Probability#

Probability is the mathematical device that allow us to quantify uncertainty in a principled way. Like other mathematical objects and theories, they can be justified entirely from a pure mathematical perspective. Nevertheless, from a practical point of view we can justify them as naturally arising from performing experiments, collecting observational data and even when doing computational simulations. For simplicity we will talk about experiments, knowing we are using this term in a very broad sense. To think about probabilities we can think in terms of mathematical sets. The sample space \(\mathcal{X}\) is the set of all possible events from an experiment. An event \(A\) is a subset of \(\mathcal{X}\). We say \(A\) happens when we perform an experiment and we get \(A\) as the outcome. For a typical 6 face die we can write:

We may define the event \(A\) as any subset of \(\mathcal{X}\), for example, getting an even number, \(A = \{2, 4, 6\}\). We can associate probabilities to events. If we want to indicate the probability of the event \(A\) we write \(P(A=\{2, 4, 6\})\) or to be more concise \(P(A)\). The probability function \(P\) takes an event \(A\) which is a subset of \(\mathcal{X}\) as input and returns \(P(A)\). Probabilities, like \(P(A)\), can take any number in the interval 0 to 1 (including both extremes), using interval notation we write this is as \([0, 1]\), the brackets meaning inclusive bounds. If the event never happens then the probability of that event is 0, for example \(P(A=-1)=0\), if the event always happens then it has probability 1, for example \(P(A=\{1,2,3,4,5,6\})=1\). We say events are disjoint if they can not happen together, for example, if the event \(A_1\) represent odds numbers and \(A_2\) even numbers, then the probability of rolling a die an getting both \(A_1\) and \(A_2\) is 0. If the event \(A_1, A_2, \cdots A_n\) are disjoint, meaning they can not happen at the same time, then \(\sum_i^n P(A_i) = 1\). Continuing with the example of \(A_1\) representing odd numbers and \(A_2\) even numbers, then the probability of rolling a die and getting either \(A_1\) or \(A_2\) is 1. Any function that satisfies these properties is a valid probability function. We can think of probability as a positive, conserved quantity that is allocated across the possible events [3].

As we just saw, probabilities have a clear mathematical definition. How we interpret probabilities is a different story with different schools of thought. As Bayesian we tend to interpret probabilities as degrees of uncertainty. For example, for a fair die, the probability of getting an odd number when rolling a die is \(0.5\), meaning we are half-sure we will get an odd number. Alternatively we can interpret this number as saying if we roll a die infinite times, half the time we will get odd numbers and half the time even numbers. This is the frequentist interpretation which is also a useful way of thinking about probabilities. If you do not want to roll the die infinite times you can just roll it a large number of times and say that you will approximately get odds half of the time. This is in fact what we did in Code Block experiment. Finally, we notice that for a fair die we expect the probability of getting any single number to be \(\frac{1}{6}\), but for a non-fair die this probability may be different. The equiprobability of the outcomes is just a special case.

If probabilities reflect uncertainty, then is natural to ask what is the probability that the mass of Mars is \(6.39 \times 10^{23}\) kg, or the probability of rain on May 1 in Helsinki, or the probability that capitalism gets replaced by a different socio-economical system in the next 3 decades. We say this definition of probability is epistemic, since it is not about a property of the real world (whatever that is) but a property about our knowledge about that world. We collect data and analyze it, because we think that we can update our internal knowledge state based on external information.

We notice that what can happen in the real world is determined by all the details of the experiments, even those we do not control or are not aware of. On the contrary the sample space is a mathematical object that we define either implicitly or explicitly. For example, by defining the sample space of our die as in Equation (11.1) we are ruling out the possibility of the die landing on an edge, which is actually possible when rolling dice in a non-flat surface. Elements from the sample space may be excluded on purpose, for example, we may have designed the experiment in such a way that we roll the die until we get one integer from \(\{1, 2, 3, 4, 5, 6\}\). Or by omission, like in a survey we may ask people about their gender, but if we only include female or male as options in the possible response, we may force people to choose between two non-adequate answers or completely miss their answers as they may not feel interested in responding to the rest of the survey. We must be aware that the platonic world of ideas which includes all mathematical concepts is different from the real world, in statistical modeling we constantly switch back and forth between these two worlds.

11.1.2. Conditional Probability#

Given two events \(A\) and \(B\) with \(P(B) > 0\), the probability of \(A\) given \(B\), which we write as \(P(A \mid B)\) is defined as :

\(P(A, B)\) is the probability that the events \(A\) and \(B\) occur, it is also usually written as \(P(A \cap B)\) (the symbol \(\cap\) indicates intersection of sets), the probability of the intersection of the events \(A\) and \(B\).

\(P(A \mid B)\) it is known as conditional probability, and it is the probability that event \(A\) occurs, conditioned by the fact that we know (or assume, imagine, hypothesize, etc) that \(B\) has occurred. For example, the probability that a sidewalk is wet is different from the probability that such a sidewalk is wet given that it is raining.

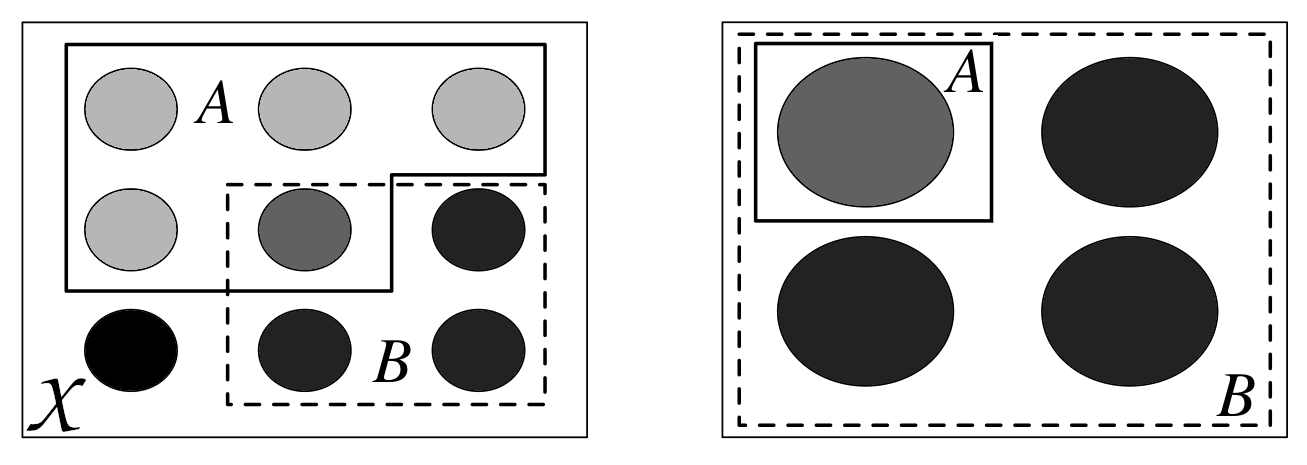

A conditional probability can be viewed as the reduction or restriction of the sample space. Fig. 11.1 shows how we went from having the events \(A\) and \(B\) in the sample space \(\mathcal{X}\), on the left, to having \(B\) as the sample space and a subset of \(A\), the one being compatible with \(B\). When we say that \(B\) has occurred we are not necessarily talking about something in the past, it is just a more colloquial way of saying, once we have conditioned on \(B\) or once we have restricted the sample space to agree with the evidence \(B\).

Fig. 11.1 Conditioning is redefining the sample space. On the left we see the sample \(\mathcal{X}\), each circle represent a possible outcome. We have two events, \(A\) and \(B\). On the right we have represented \(P(A \mid B)\), once we know \(B\) we can rule out all events not in \(B\). This figure was adapted from Introduction to Probability [5].#

The concept of conditional probability is at the heart of statistics and is central to thinking about how we should update our knowledge of an event in the light of new data. All probabilities are conditional, with respect to some assumption or model. Even when we do not express it explicitly, there are no probabilities without context.

11.1.3. Probability Distribution#

Instead of calculating the probability of obtaining the number 5 when rolling a die, we may be more interested in finding out the list of probabilities for all numbers on a die. Once this list is computed we can display it or use it to compute other quantities like the probability of getting the number 5, or the probability of getting a number equal or larger than 5. The formal name of this list is probability distribution.

Using Code Block experiment we obtained an empirical probability distribution of a die, that is, a distribution calculated from data. But there are also theoretical distributions, which are central in statistics among other reasons because they allow the construction of probabilistic models.

Theoretical probability distributions have precise mathematical formulas, similar to how circles have a precise mathematical definition. A circle is the geometric space of points on a plane that are equidistant from another point called the center. Given the parameter radius, a circle is perfectly defined [4]. We could say that there is not a single circumference, but a family of circumferences where each member differs from the rest only by the value of the parameter radius, since once this parameter is also defined, the circumference is defined.

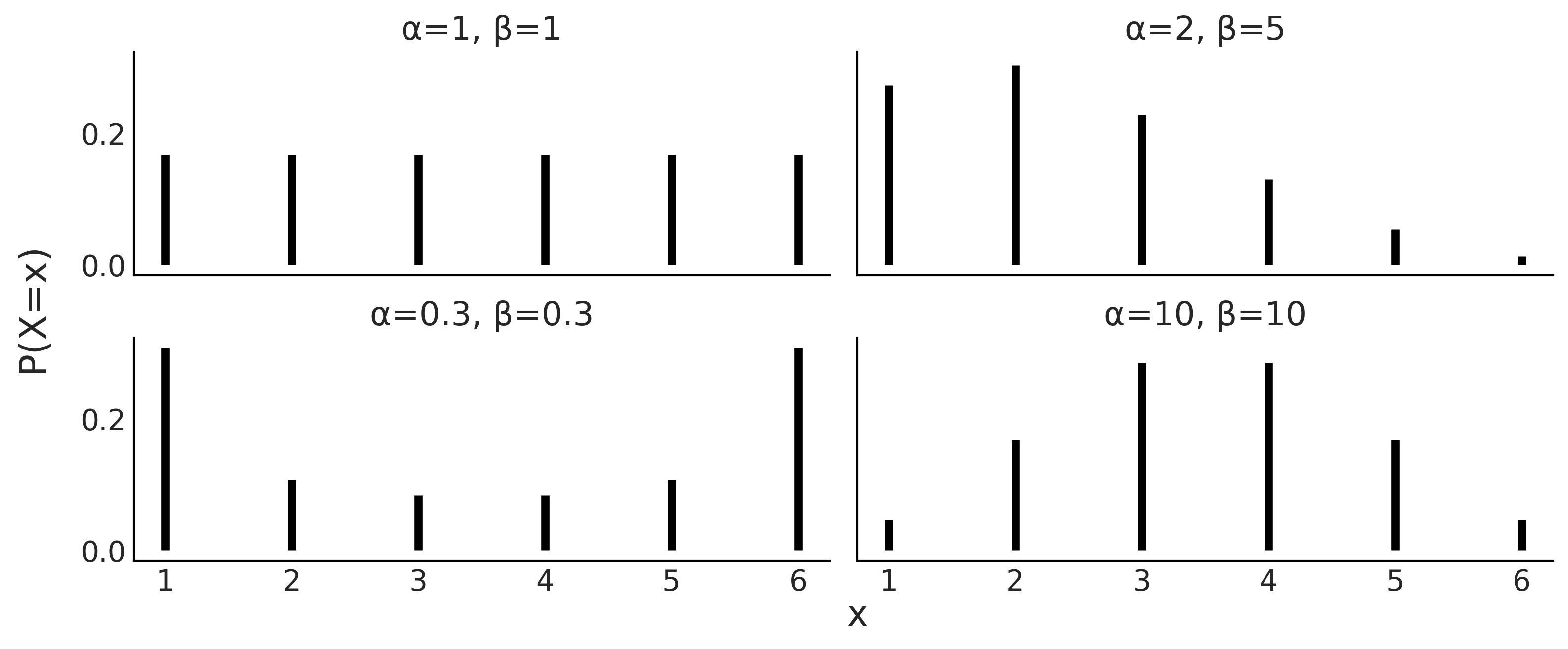

Similarly, probability distributions come in families, whose members are perfectly defined by one or more parameters. It is common to write the parameter names with letters of the Greek alphabet, although this is not always the case. Fig. 11.2 is an example of such families of distributions, that we may use to represent a loaded die. We can see how this probability distribution is controlled by two parameters \(\alpha\) and \(\beta\). If we change them the shape of the distribution changes, we can make it flat or concentrated towards one side, push most of the mass the extremes, or concentrated the mass in the middle. As the radius of the circumference is restricted to be positive, the parameters of distributions also have restrictions, in fact \(\alpha\) and \(\beta\) must both be positive.

Fig. 11.2 Four members of a family of discrete distributions with parameters \(\alpha\) and \(\beta\). The height of the bars represents the probability of each \(x\) value. The values of \(x\) not drawn have probability 0 as they are out of the support of the distribution.#

11.1.4. Discrete Random Variables and Distributions#

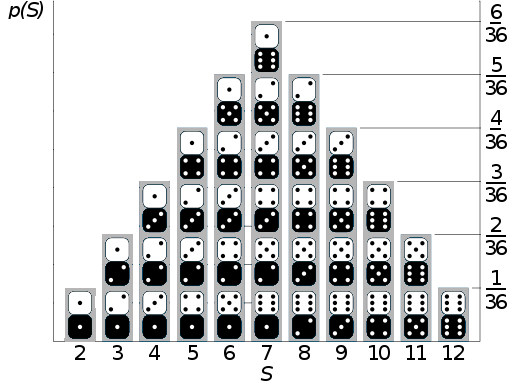

A random variable is a function that maps the sample space into the real numbers \(\mathbb{R}\). Continuing with the die example if the events of interest were the number of the die, the mapping is very simple, we associate \(\LARGE \unicode{x2680}\) with the number 1, \(\LARGE \unicode{x2681}\) with 2, etc. With two dice we could have an \(S\) random variable as the sum of the outcomes of both dice. Thus the domain of the random variable \(S\) is \(\{2, 3, 4, 5, 6, 7, 8, 9, 10, 11, 12\}\), and if both dice are fair then their probability distribution is depicted in Fig. 11.3.

Fig. 11.3 If the sample space is the set of possible numbers rolled on two dice, and the random variable of interest is the sum \(S\) of the numbers on the two dice, then \(S\) is a discrete random variable whose distribution is described in this figure with the probability of each outcome represented as the height of the columns. This figure has been adapted from https://commons.wikimedia.org/wiki/File:Dice_Distribution_(bar).svg#

.svg){kind=link}

We could also define another random variable \(C\) with sample space \(\{\text{red}, \text{green}, \text{blue}\}\). We could map the sample space to \(\mathbb{R}\) in the following way:

This encoding is useful, because performing math with numbers is easier than with strings regardless of whether we are using analog computation on “pen and paper” or digital computation with a computer.

As we said a random variable is a function, and given that the mapping between the sample space and \(\mathbb{R}\) is deterministic it is not immediately clear where the randomness in a random variable comes from. We say a variable is random in the sense that if we perform an experiment, i.e. we ask the variable for a value like we did in Code Block die and experiment we will get a different number each time without the succession of outcomes following a deterministic pattern. For example, if we ask for the value of random variable \(C\) 3 times in a row we may get red, red, blue or maybe blue, green, blue, etc.

A random variable \(X\) is said to be discrete if there is a finite list of values \(a_1, a_2, \dots, a_n\) or an infinite list of values \(a_1, a_2, \dots\) such that the total probability is \(\sum_j P(X=a_j) = 1\). If \(X\) is a discrete random variable then a finite or countably infinite set of values \(x\) such that \(P(X = x) > 0\) is called the support of \(X\).

As we said before we can think of a probability distribution as a list associating a probability with each event. Additionally a random variable has a probability distribution associated to it. In the particular case of discrete random variables the probability distribution is also called a Probability Mass Function (PMF). It is important to note that the PMF is a function that returns probabilities. The PMF of \(X\) is the function \(P(X=x)\) for \(x \in \mathbb{R}\). For a PMF to be valid, it must be non-negative and sum to 1, i.e. all its values should be non-negative and the sum over all its domain should be 1.

It is important to remark that the term random in random variable does not implies that any value is allowed, only those in the sample space. For example, we can not get the value orange from \(C\), nor the value 13 from \(S\). Another common source of confusion is that the term random implies equal probability, but that is not true, the probability of each event is given by the PMF, for example, we may have \(P(C=\text{red}) = \frac{1}{2}, P(C=\text{green}) = \frac{1}{4}, P(C=\text{blue}) = \frac{1}{4}\). The equiprobability is just a special case.

We can also define a discrete random variable using a cumulative distribution function (CDF). The CDF of a random variable \(X\) is the function \(F_X\) given by \(F_X(x) = P(X \le x)\). For a CDF to be valid, it must be monotonically increasing [5], right-continuous [6], converge to 0 as \(x\) approaches to \(- \infty\), and converge to 1 as \(x\) approaches \(\infty\).

In principle, nothing prevents us from defining our own probability distribution. But there are many already defined distributions that are so commonly used, they have their own names. It is a good idea to become familiar with them as they appear quite often. If you check the models defined in this book you will see that most of them use combinations of predefined probability distributions and only a few examples used custom defined distribution. For example, in Section Approximating Moving Averages Code Block MA2_abc we used a Uniform distribution and two potentials to define a 2D triangular distribution.

Figures Fig. 11.4, Fig. 11.5, and Fig. 11.6, are example of some common discrete distribution represented with their PMF and CDF. On the left we have the PMFs, the height of the bars represents the probability of each \(x\). On the right we have the CDF, here the jump between two horizontal lines at a value of \(x\) represents the probability of \(x\). The figure also includes the values of the mean and standard deviation of the distributions, is important to remark that these values are properties of the distributions, like the length of a circumference, and not something that we compute from a finite sample (see Section Expectations for details).

Another way to describe random variables is to use stories. A story for \(X\) describes an experiment that could give rise to a random variable with the same distribution as \(X\). Stories are not formal devices, but they are useful anyway. Stories have helped humans to make sense of their surrounding for millennia and they continue to be useful today, even in statistics. In the book Introduction to Probability [5] Joseph K. Blitzstein and Jessica Hwang make extensive use of this device. They even use story proofs extensively, these are similar to mathematical proof but they can be more intuitive. Stories are also very useful devices to create statistical models, you can think about how the data may have been generated, and then try to write that down in statistical notation and/or code. We do this, for example, in Chapter 9 with our flight delay example.

11.1.4.1. Discrete Uniform Distribution#

This distribution assigns equal probability to a finite set of consecutive integers from interval a to b inclusive. Its PMF is:

for values of \(x\) in the interval \([a, b]\), otherwise \(P(X = x) = 0\), where \(n=b-a+1\) is the total number values that \(x\) can take.

We can use this distribution to model, for example, a fair die. Code Block scipy_unif shows how we can use Scipy to define a distribution and then compute useful quantities such as the PMF, CDF, and moments (see Section Expectations).

a = 1

b = 6

rv = stats.randint(a, b+1)

x = np.arange(1, b+1)

x_pmf = rv.pmf(x) # evaluate the pmf at the x values

x_cdf = rv.cdf(x) # evaluate the cdf at the x values

mean, variance = rv.stats(moments="mv")

Using Code Block scipy_unif plus a few lines of Matplotlib we generate Fig. 11.4. On the left panel we have the PMF where the height of each point indicates the probability of each event, we use points and dotted lines to highlight that the distribution is discrete. On the right we have the CDF, the height of the jump at each value of \(x\) indicates the probability of that value.

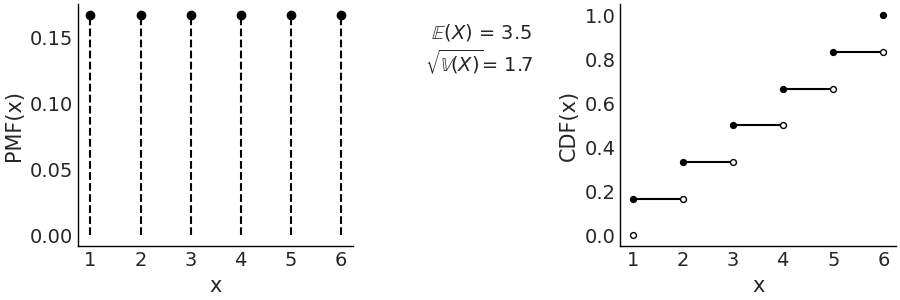

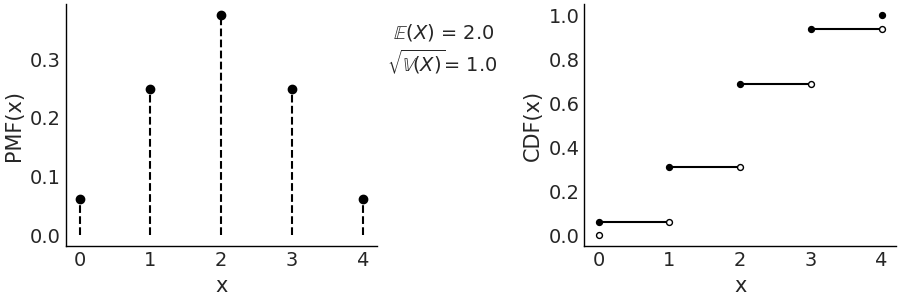

Fig. 11.4 Discrete Uniform with parameters (1, 6). On the left the PMF. The height of the lines represents the probabilities for each value of \(x\). On the right the CDF. The height of the jump at each value of \(x\) represent its probability. Values outside of the support of the distribution are not represented. The filled dots represent the inclusion of the CDF value at a particular \(x\) value, the open dots reflect the exclusion.#

In this specific example the discrete Uniform distribution is defined on the interval \([1, 6]\). Therefore, all values less than 1 and greater than 6 have probability 0. Being a Uniform distribution, all the points have the same height and that height is \(\frac{1}{6}\). There are two parameters of the Uniform discrete distribution, the lower limit \(a\) and upper limit \(b\).

As we already mentioned in this chapter if we change the parameters of a

distribution the particular shape of the distribution will change (try

for example, replacing stats.randint(1, 7) in Code Block

scipy_unif with stats.randint(1, 4). That

is why we usually talk about family of distributions, each member of

that family is a distribution with a particular and valid combination of

parameters. Equation (11.3) defines the family of discrete

Uniform distributions as long as \(a < b\) and both \(a\) and \(b\) are

integers.

When using probability distributions to create statistical applied models it is common to link the parameters with quantities that make physical sense. For example, in a 6 sided die it makes sense that \(a=1\) and \(b=6\). In probability we generally know the values of these parameters while in statistics we generally do not know these values and we use data to infer them.

11.1.4.2. Binomial Distribution#

A Bernoulli trial is an experiment with only two possible outcomes yes/no (success/failure, happy/sad, ill/healthy, etc). Suppose we perform \(n\) independent [7] Bernoulli trials, each with the same success probability \(p\) and let us call \(X\) the number of success. Then the distribution of \(X\) is called the Binomial distribution with parameters \(n\) and \(p\), where \(n\) is a positive integer and \(p \in [0, 1]\). Using statistical notation we can write \(X \sim Bin(n, p)\) to mean that \(X\) has the Binomial distribution with parameters \(n\) and \(p\), with the PMF being:

The term \(p^x(1-p)^{n-x}\) counts the number of \(x\) success in \(n\) trials. This term only considers the total number of success but not the precise sequence, for example, \((0,1)\) is the same as \((1,0)\), as both have one success in two trials. The first term is known as Binomial Coefficient and computes all the possible combinations of \(x\) elements taken from a set of \(n\) elements.

The Binomial PMFs are often written omitting the values that return 0, that is the values outside of the support. Nevertheless it is important to be sure what the support of a random variable is in order to avoid mistakes. A good practice is to check that PMFs are valid, and this is essential if we are proposing a new PMFs instead of using one off the shelf.

When \(n=1\) the Binomial distribution is also known as the Bernoulli distribution. Many distributions are special cases of other distributions or can be obtained somehow from other distributions.

Fig. 11.5 \(\text{Bin}(n=4, p=0.5)\) On the left the PMF. The height of the lines represents the probabilities for each value of \(x\). On the right the CDF. The height of the jump at each value of \(x\) represent its probability. Values outside of the support of the distribution are not represented.#

11.1.4.3. Poisson Distribution#

This distribution expresses the probability that \(x\) events happen during a fixed time interval (or space interval) if these events occur with an average rate \(\mu\) and independently from each other. It is generally used when there are a large number of trials, each with a small probability of success. For example

Radioactive decay, the number of atoms in a given material is huge, the actual number that undergo nuclear fission is low compared to the total number of atoms.

The daily number of car accidents in a city. Even when we may consider this number to be high relative to what we would prefer, it is low in the sense that every maneuver that the driver performs, including turns, stopping at lights, and parking, is an independent trial where an accident could occur.

The PMF of a Poisson is defined as:

Notice that the support of this PMF are all the natural numbers, which is an infinite set. So we have to be careful with our list of probabilities analogy, as summing an infinite series can be tricky. In fact Equation (11.5) is a valid PMF because of the Taylor series \(\sum_0^{\infty} \frac{\mu^{x}}{x!} = e^{\mu}\)

Both the mean and variance of the Poisson distribution are defined by \(\mu\). As \(\mu\) increases, the Poisson distribution approximates to a Normal distribution, although the latter is continuous and the Poisson is discrete. The Poisson distribution is also closely related to the Binomial distribution. A Binomial distribution can be approximated with a Poisson, when \(n >> p\) [8], that is, when the probability of success (\(p\)) is low compared with the number o trials (\(n\)) then \(\text{Pois}(\mu=np) \approx \text{Bin}(n, p)\). For this reason the Poisson distribution is also known as the law of small numbers or the law of rare events. As we previously mentioned this does not mean that \(\mu\) has to be small, but instead that \(p\) is low with respect to \(n\).

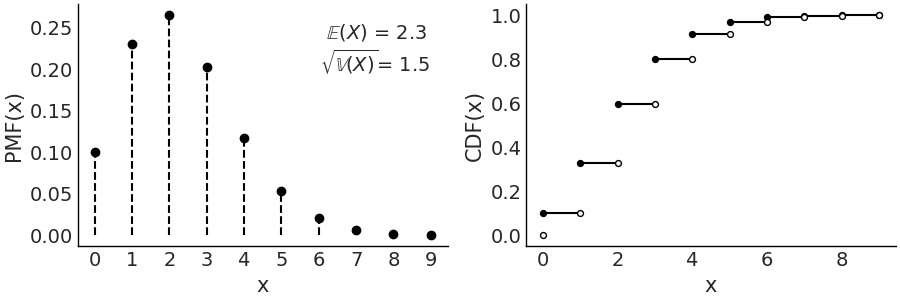

Fig. 11.6 \(\text{Pois}(2.3)\) On the left the PMF. The height of the lines represents the probabilities for each value of \(x\). On the right the CDF. The height of the jump at each value of \(x\) represent its probability. Values outside of the support of the distribution are not represented.#

11.1.5. Continuous Random Variables and Distributions#

So far we have seen discrete random variables. There is another type of random variable that is widely used called continuous random variables, whose support takes values in \(\mathbb {R}\). The most important difference between discrete and continuous random variables is that the latter can take on any \(x\) value in an interval, although the probability of any \(x\) value is exactly 0. Introduced this way you may think that these are the most useless probability distributions ever. But that is not the case, the actual problem is that our analogy of treating a probability distribution as a finite list is a very limited analogy and it fails badly with continuous random variables [9].

In Figures Fig. 11.4, Fig. 11.5, and Fig. 11.6, to represent PMFs (discrete variables), we used the height of the lines to represent the probability of each event. If we add the heights we always get 1, that is, the total sum of the probabilities. In a continuous distribution we do not have lines but rather we have a continuous curve, the height of that curve is not a probability but a probability density and instead of of a PMF we use a Probability Density Function (PDF). One important difference is that height of \(\text{PDF}(x)\) can be larger than 1, as is not the probability value but a probability density. To obtain a probability from a PDF instead we must integrate over some interval:

Thus, we can say that the area below the curve of the PDF (and not the height as in the PMF) gives us a probability, the total area under the curve, i.e. evaluated over the entire support of the PDF, must integrate to 1. Notice that if we want to find out how much more likely the value \(x_1\) is compared to \(x_2\) we can just compute \(\frac{pdf(x_1)}{pdf(x_2)}\).

In many texts, including this one, it is common to use the symbol \(p\) to talk about the \(pmf\) or \(pdf\). This is done in favour of generality and hoping to avoid being very rigorous with the notation which can be an actual burden when the difference can be more or less clear from the context.

For a discrete random variable, the CDF jumps at every point in the support, and is flat everywhere else. Working with the CDF of a discrete random variable is awkward because of this jumpiness. Its derivative is almost useless since it is undefined at the jumps and 0 everywhere else. This is a problem for gradient-based sampling methods like Hamiltonian Monte Carlo (Section Inference Methods). On the contrary for continuous random variables, the CDF is often very convenient to work with, and its derivative is precisely the probability density function (PDF) that we have discussed before.

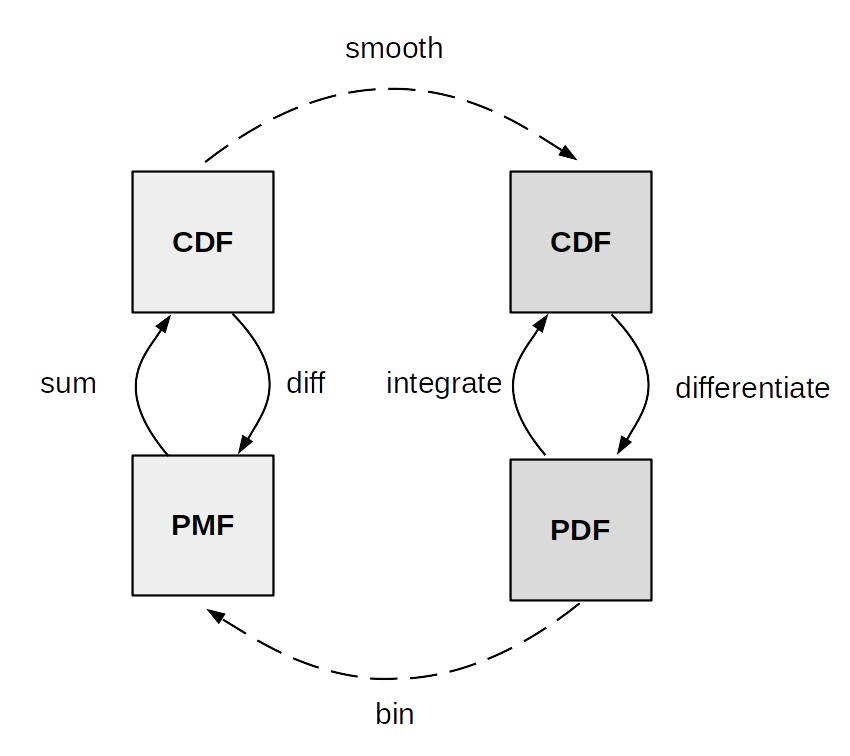

Fig. 11.7 summarize the relationship between the CDF,

PDF and PMF. The transformations between discrete CDF and PMF on one

side and continuous CDF and PMF on the other are well defined and thus

we used arrows with solid lines. Instead the transformations between

discrete and continuous variables are more about numerical approximation

than well defined mathematical operations. To approximately get from a

discrete to a continuous distribution we use a smoothing method. One

form of smoothing is to use a continuous distribution instead of a

discrete one. To go from continuous to discrete we can discretize or bin

the continuous outcomes. For example, a Poisson distribution with a

large value of \(\mu\) approximately Gaussian [10], while still being

discrete. For those cases using a scenarios using a Poisson or a

Gaussian maybe be interchangeable from a practical point of view. Using

ArviZ you can use az.plot_kde with discrete data to approximate a

continuous functions, how nice the results of this operation look

depends on many factors. As we already said it may look good for a

Poisson distribution with a relatively large value of \(\mu\). When

calling az.plot_bpv(.) for a discrete variable, ArviZ will smooth it,

using an interpolation method, because the probability integral

transform only works for continuous variables.

Fig. 11.7 Relationship between the CDF, PDF and PMF. Adapted from the book Think Stats [132].#

As we did with the discrete random variables, now we will see a few example of continuous random variables with their PDF and CDF.

11.1.5.1. Continuous Uniform Distribution#

A continuous random variable is said to have a Uniform distribution on the interval \((a, b)\) if its PDF is:

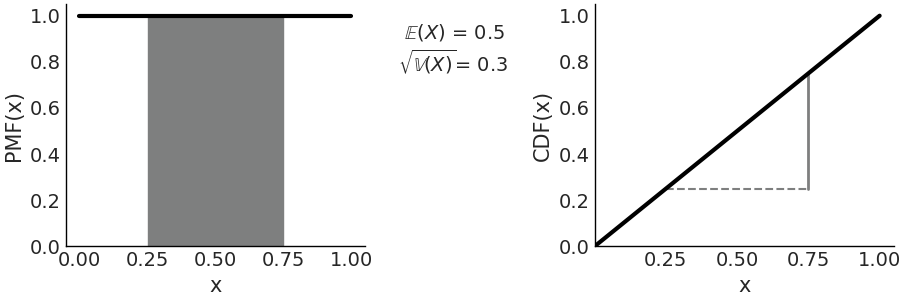

Fig. 11.8 \(\mathcal{U}(0, 1)\) On the left the PDF, the black line represents the probability density, the gray shaded area represents the probability \(P(0.25 < X < 0.75) =0.5\). On the right the CDF, the height of the gray continuous segment represents \(P(0.25 < X < 0.75) =0.5\). Values outside of the support of the distribution are not represented.#

The most commonly used Uniform distribution in statistics is \(\mathcal{U}(0, 1)\) also known as the standard Uniform. The PDF and CDF for the standard Uniform are very simple: \(p(x) = 1\) and \(F_{(x)} = x\) respectively, Fig. 11.8 represents both of them, this figure also indicated how to compute probabilities from the PDF and CDF.

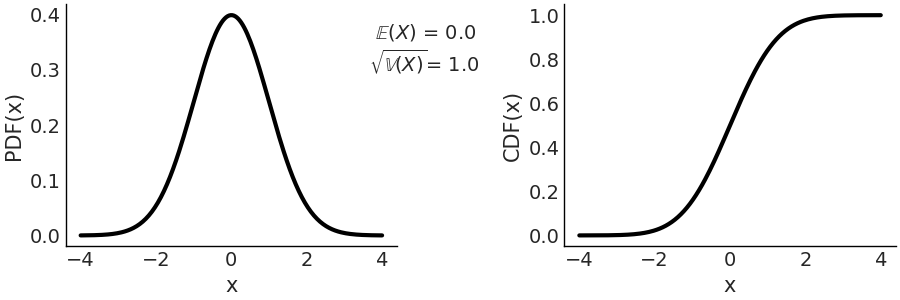

11.1.5.2. Gaussian or Normal Distribution#

This is perhaps the best known distribution [11]. On the one hand, because many phenomena can be described approximately using this distribution (thanks to central limit theorem, see Subsection The Central Limit Theorem below). On the other hand, because it has certain mathematical properties that make it easier to work with it analytically.

The Gaussian distribution is defined by two parameters, the mean \(\mu\) and the standard deviation \(\sigma\) as shown in Equation (11.8). A Gaussian distribution with \(\mu=0\) and \(\sigma=1\) is known as the standard Gaussian distribution.

On the left panel of Fig. 11.9 we have the PDF, and on the right we have the CDF. Both the PDF and CDF are represented for the invertal -4, 4, but notice that the support of the Gaussian distribution is the entire real line.

Fig. 11.9 Representation of \(\mathcal{N}(0, 1)\), on the left the PDF, on the right the CDF. The support of the Gaussian distribution is the entire real line.#

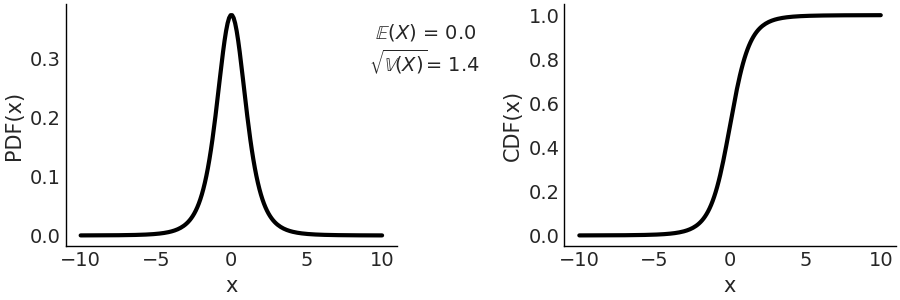

11.1.5.3. Student’s t-distribution#

Historically this distribution arose to estimate the mean of a normally distributed population when the sample size is small [12]. In Bayesian statistics, a common use case is to generate models that are robust against aberrant data as we discussed in Section Robust Regression.

where \(\Gamma\) is the gamma function [13] and \(\nu\) is commonly called degrees of freedom. We also like the name degree of normality, since as \(\nu\) increases, the distribution approaches a Gaussian. In the extreme case of \(\lim_{\nu \to \infty}\) the distribution is exactly equal to a Gaussian distribution with the same mean and standard deviation equal to \(\sigma\).

When \(\nu=1\) we get the Cauchy distribution [14]. Which is similar to a Gaussian but with tails decreasing very slowly, so slowly that this distribution does not have a defined mean or variance. That is, it is possible to calculate a mean from a data set, but if the data came from a Cauchy distribution, the spread around the mean will be high and this spread will not decrease as the sample size increases. The reason for this strange behavior is that distributions, like the Cauchy, are dominated by the tail behavior of the distribution, contrary to what happens with, for example, the Gaussian distribution.

For this distribution \(\sigma\) is not the standard deviation, which as already said could be undefined, \(\sigma\) is the scale. As \(\nu\) increases the scale converges to the standard deviation of a Gaussian distribution.

On the left panel of Fig. 11.10 we have the PDF, and on the right we have the CDF. Compare with Fig. 11.9, a standard normal and see how the tails are heavier for the Student T distribution with parameter \(\mathcal{T}(\nu=4, \mu=0, \sigma=1)\)

Fig. 11.10 \(\mathcal{T}(\nu=4, \mu=0, \sigma=1)\) On the left the PDF, on the right the CDF. The support of the Students T distribution is the entire real line.#

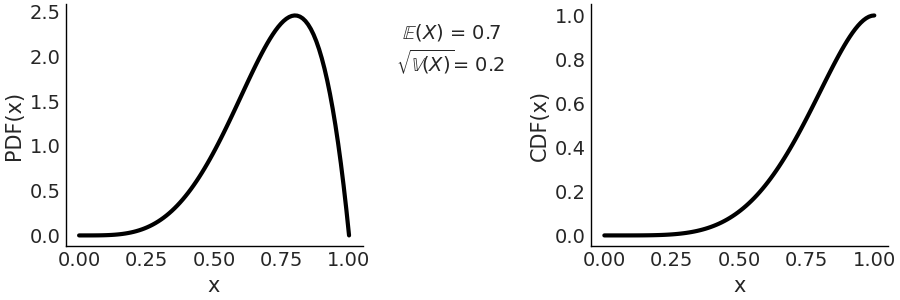

11.1.5.4. Beta Distribution#

The Beta distribution is defined in the interval \([0, 1]\). It can be used to model the behavior of random variables limited to a finite interval, for example, modeling proportions or percentages.

The first term is a normalization constant that ensures that the PDF integrates to 1. \(\Gamma\) is the Gamma function. When \(\alpha = 1\) and \(\beta = 1\) the Beta distribution reduces to the standard Uniform distribution. In Fig. 11.11 we show a \(\text{Beta}(\alpha=5, \beta=2)\) distribution.

Fig. 11.11 \(\text{Beta}(\alpha=5, \beta=2)\) On the left the PDF, on the right the CDF. The support of the Beta distribution is on the interval \([0, 1]\).#

If we want to express the Beta distribution as a function of the mean and the dispersion around the mean, we can do it in the following way. \(\alpha = \mu \kappa\), \(\beta = (1 - \mu) \kappa\) where \(\mu\) the mean and \(\kappa\) a parameter called concentration as \(\kappa\) increases the dispersion decreases. Also note that \(\kappa = \alpha + \beta\).

11.1.6. Joint, Conditional and Marginal Distributions#

Let us assume we have two random variables \(X\) and \(Y\) with the same PMF \(\text{Bin}(1, 0.5)\). Are they dependent or independent? If \(X\) represent heads in on coin toss and \(Y\) heads in another coin toss then they are independent. But if they represent heads and tails, respectively, on the same coin toss, then they are dependent. Thus even when individual (formally known as univariate) PMFs/PDFs fully characterize individual random variables, they do not have information about how the individual random variables are related to other random variables. To answer that question we need to know the joint distribution, also known as multivariate distributions. If we consider that \(p(X)\) provides all the information about the probability of finding \(X\) on the real line, in a similar way \(p(X, Y)\), the joint distribution of \(X\) and \(Y\), provides all the information about the probability of finding the tuple \((X, Y)\) on the plane. Joint distributions allow us to describe the behavior of multiple random variables that arise from the same experiment, for example, the posterior distribution is the joint distribution of all parameters in the model after we have conditioned the model on observed data.

The joint PMF is given by

The definition for \(n\) discrete random variable is similar, we just need to include \(n\) terms. Similarly to univariate PMFs valid joint PMFs must be nonnegative and sum to 1, where the sum is taken over all possible values.

In a similar way the joint CDF of \(X\) and \(Y\) is

Given the joint distribution of \(X\) and \(Y\), we can get the distribution of \(X\) by summing over all the possible values of \(Y\):

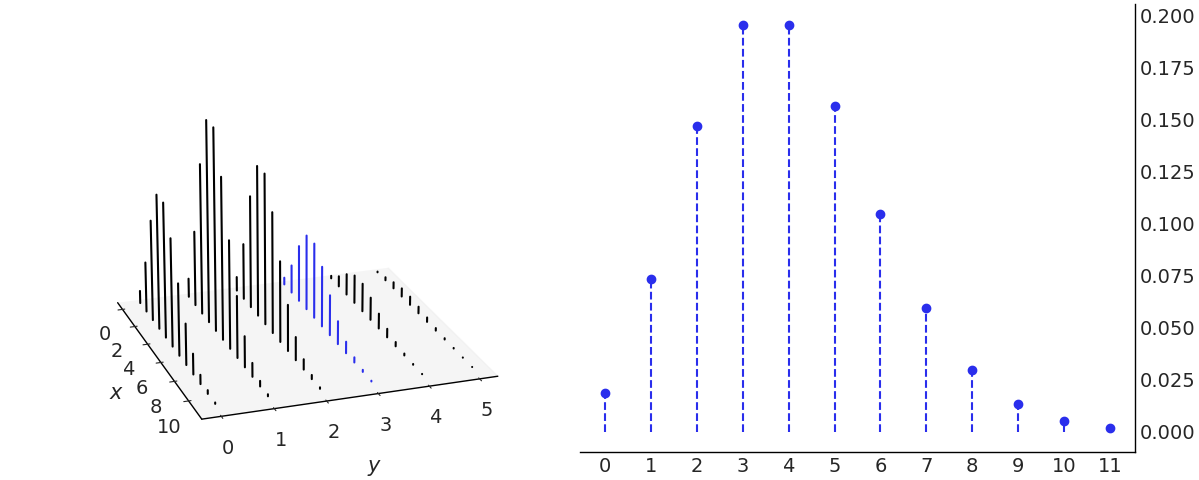

Fig. 11.12 The black lines represent the joint distribution of \(x\) and \(y\). The blue lines in the marginal distribution of \(x\) are obtained by adding the heights of the lines along the y-axis for every value of \(x\).#

In previous section we called \(P(X=x)\) the PMF of \(X\), or just the distribution of \(X\), when working with joint distributions we often call it the marginal distribution of \(X\). We do this to emphasize we are talking about the individual \(X\), without any reference to \(Y\). By summing over all the possible values of \(Y\) we get rid of \(Y\). Formally this process is known as marginalizing out \(Y\). To obtain the PMF of \(Y\) we can proceed in a similar fashion, but summing over all possible values of \(X\) instead. In the case of a joint distribution of more than 2 variables we just need to sum over all the other variables. Fig. 11.12 illustrates this.

Given the joint distribution it is straightforward to get the marginals. But going from the marginals to the joint distribution is not generally possible unless we make further assumptions. In Fig. 11.12 we can see that there is just one way to add heights of the bars along the y-axis or x-axis, but to do the inverse we must split bars and there are infinite ways of making this split.

We already introduced conditional distributions in Section Conditional Probability, and in Fig. 11.1 we show that conditioning is redefining the sample space. Fig. 11.13 demonstrates conditioning in the context of a joint distribution of \(X\) and \(Y\). To condition on \(Y=y\) we take the joint distribution at the \(Y=y\) value and forget about the rest. i.e. those for which \(Y \ne y\), this is similar as indexing a 2d array and picking a single column or row. The remaining values of \(X\), those in bold in Fig. 11.13 needs to sum 1 to be a valid PMF, and thus we re-normalize by dividing by \(P(Y=y)\)

Fig. 11.13 On the left the joint distribution of \(x\) and \(y\). The blue lines represent the conditional distribution \(p(x \ mid y=3)\). On the right we plot the same conditional distribution separately. Notice that there are as many conditional PMF of \(x\) as values of \(y\) and vice versa. We are just highlighting one possibility.#

We define continuous joint CDFs as in Equation (11.13) the same as with discrete variables and the joint PDFs as the derivative of the CDFs with respect to \(x\) and \(y\). We require valid joint PDFs to be nonnegative and integrate to 1. For continuous variables we can marginalize variables out in a similar fashion we did for discrete ones, with the difference that instead of a sum we need to compute an integral.

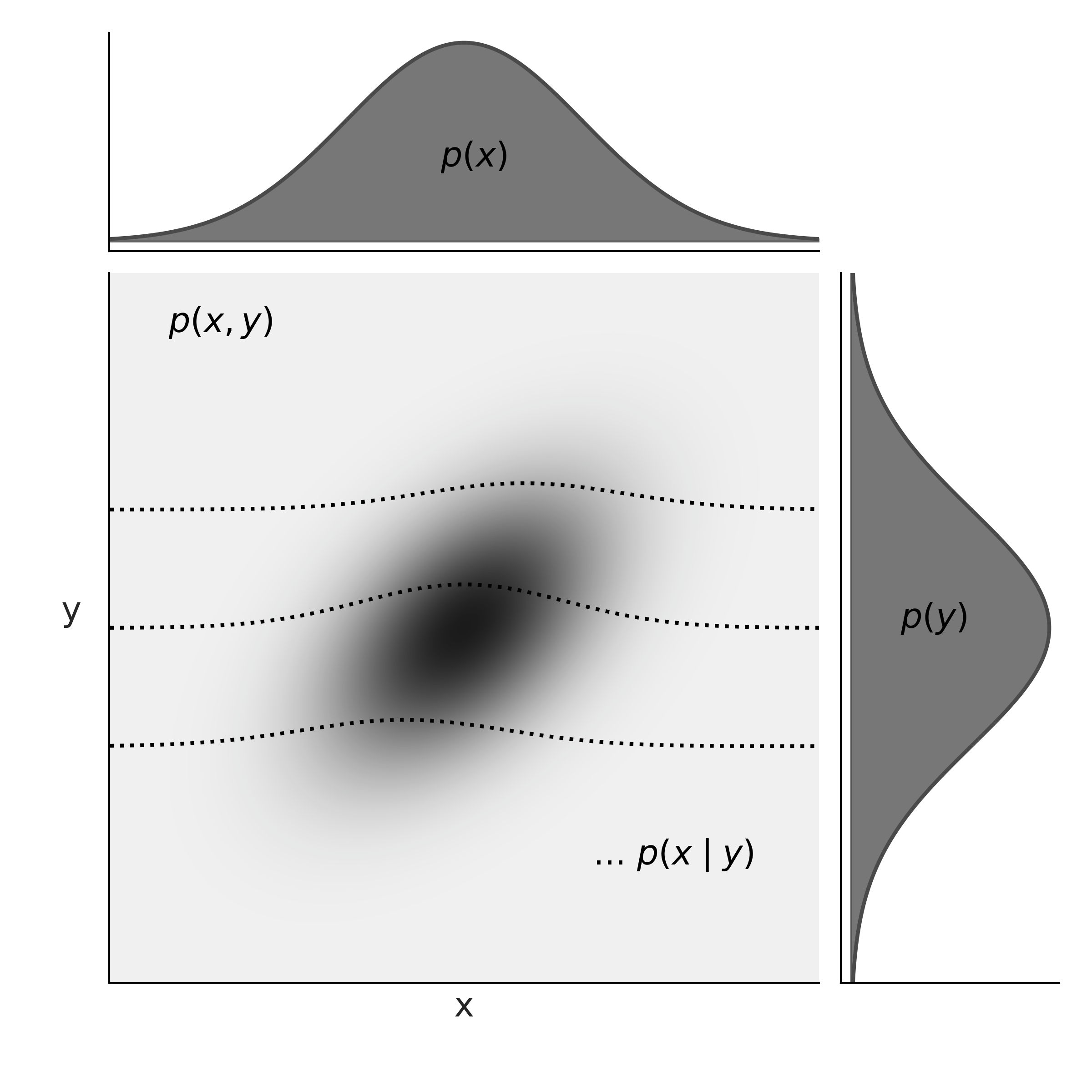

Fig. 11.14 At the center of the figure we have the joint probability \(p(x, y)\) represented with a gray scale, darker for higher probability density. At the top and right margins we have the marginal distributions \(p(x)\) and \(p(y)\) respectively. The dashed lines represents the conditional probability \(p(x \mid y)\) for 3 different values of \(y\). We can think of these as (renormalized) slices of the joint \(p(x, y)\) at a given value of \(y\).#

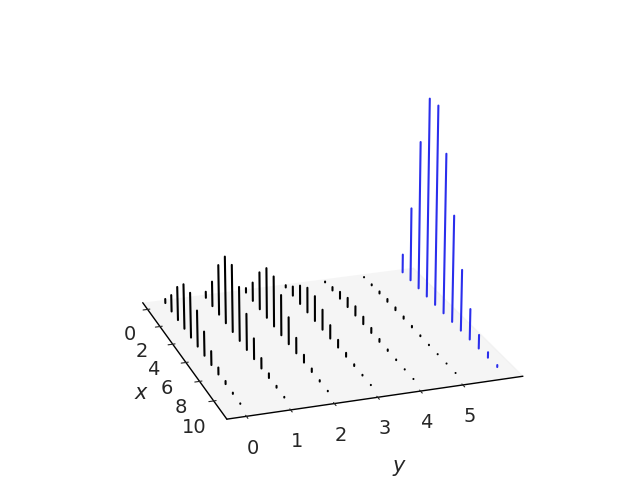

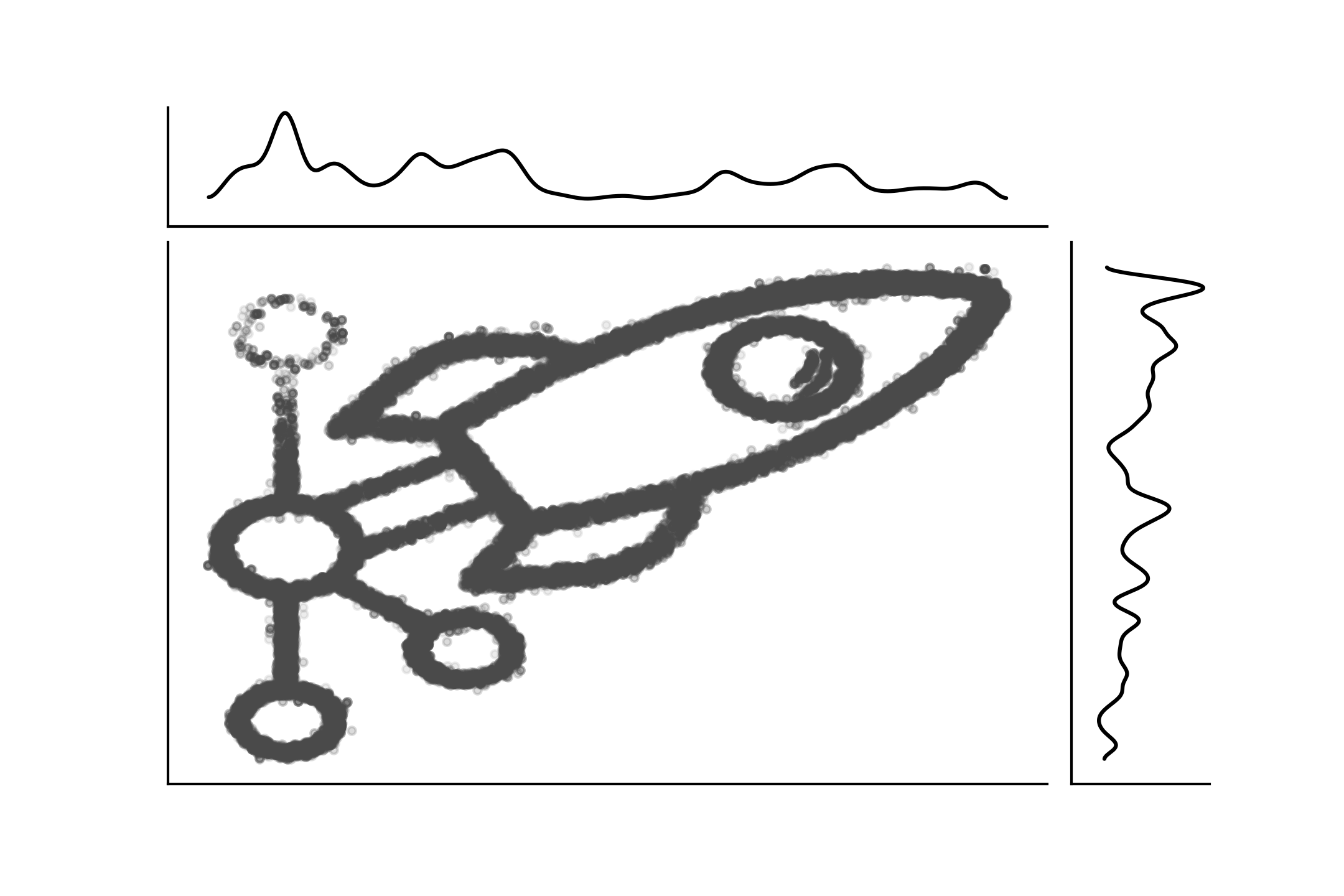

Fig. 11.15 show another example of a a join distribution with its marginals distribution. This is also a clear example that going from the joint to the marginals is straightforward, as there is a unique way of doing it, but the inverse is not possible unless we introduce further assumptions. Joint distributions can also be a hybrid of discrete and continuous distributions. Fig. 11.16 shows an example.

Fig. 11.15 The PyMC3 logo as a sample from a joint distribution with its marginals. This figure was created with imcmc ColCarroll/imcmc a library for turning 2D images into probability distributions and then sampling from them to create images and gifs.#

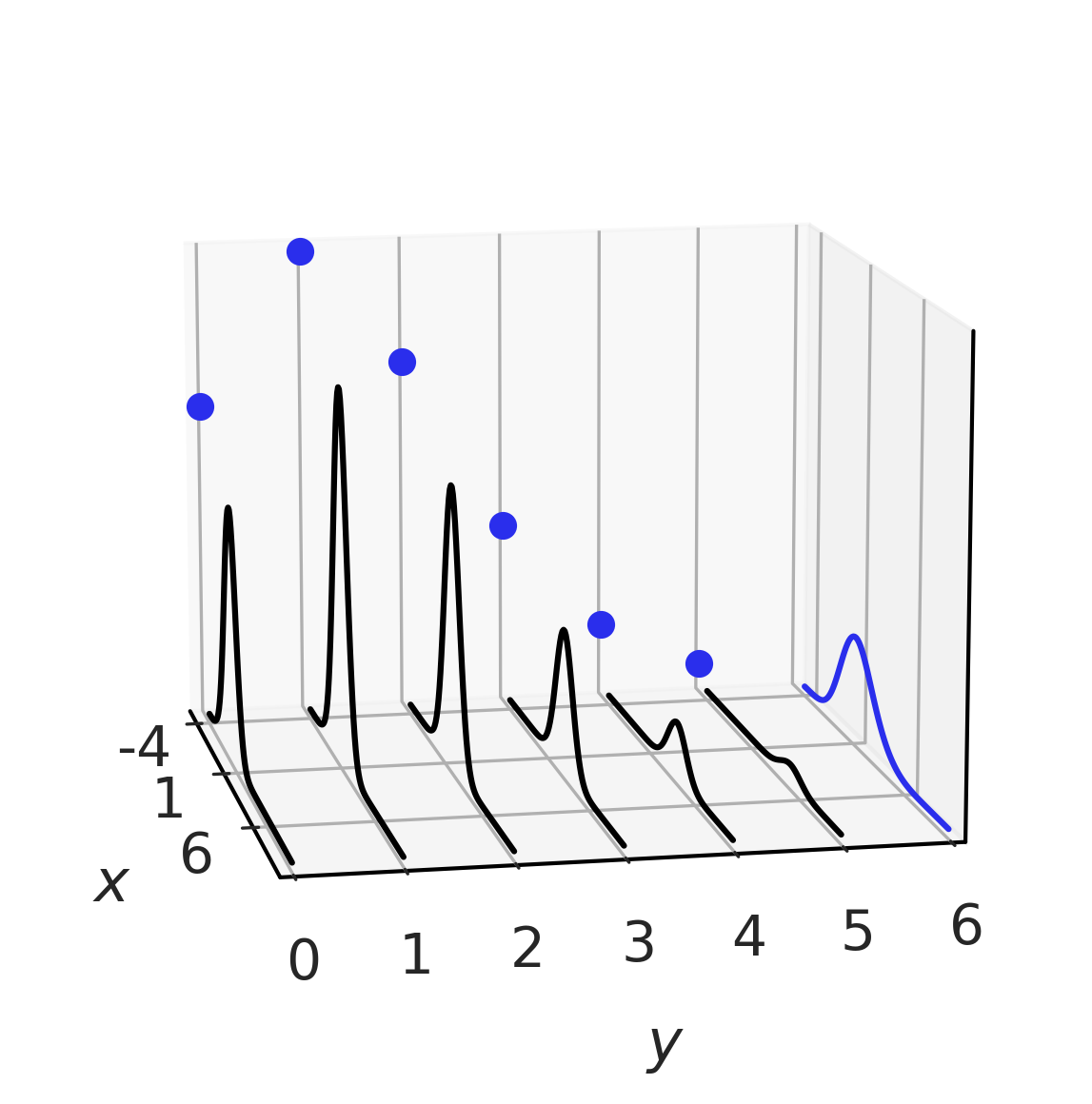

Fig. 11.16 A hybrid joint distribution in black. The marginals are represented in blue, with \(X\) being distributed as a Gaussian and \(Y\) as a Poisson. It is easy to see how for each value of \(Y\) we have a (Gaussian) conditional distribution.#

11.1.7. Probability Integral Transform (PIT)#

The probability integral transform (PIT), also known as the universality of the Uniform distribution, states that given a random variable \(X\) with a continuous distribution with cumulative distribution \(F_X\), we can compute a random variable \(Y\) with standard Uniform distribution as:

We can see this is true as follows, by the definition of the CDF of \(Y\)

Replacing Equation (11.16) in the previous one

Taking the inverse of \(F_X\) to both sides of the inequality

By the definition of CDF

Simplifying, we get the CDF of a standard Uniform distribution \(\mathcal{U}\)(0, 1).

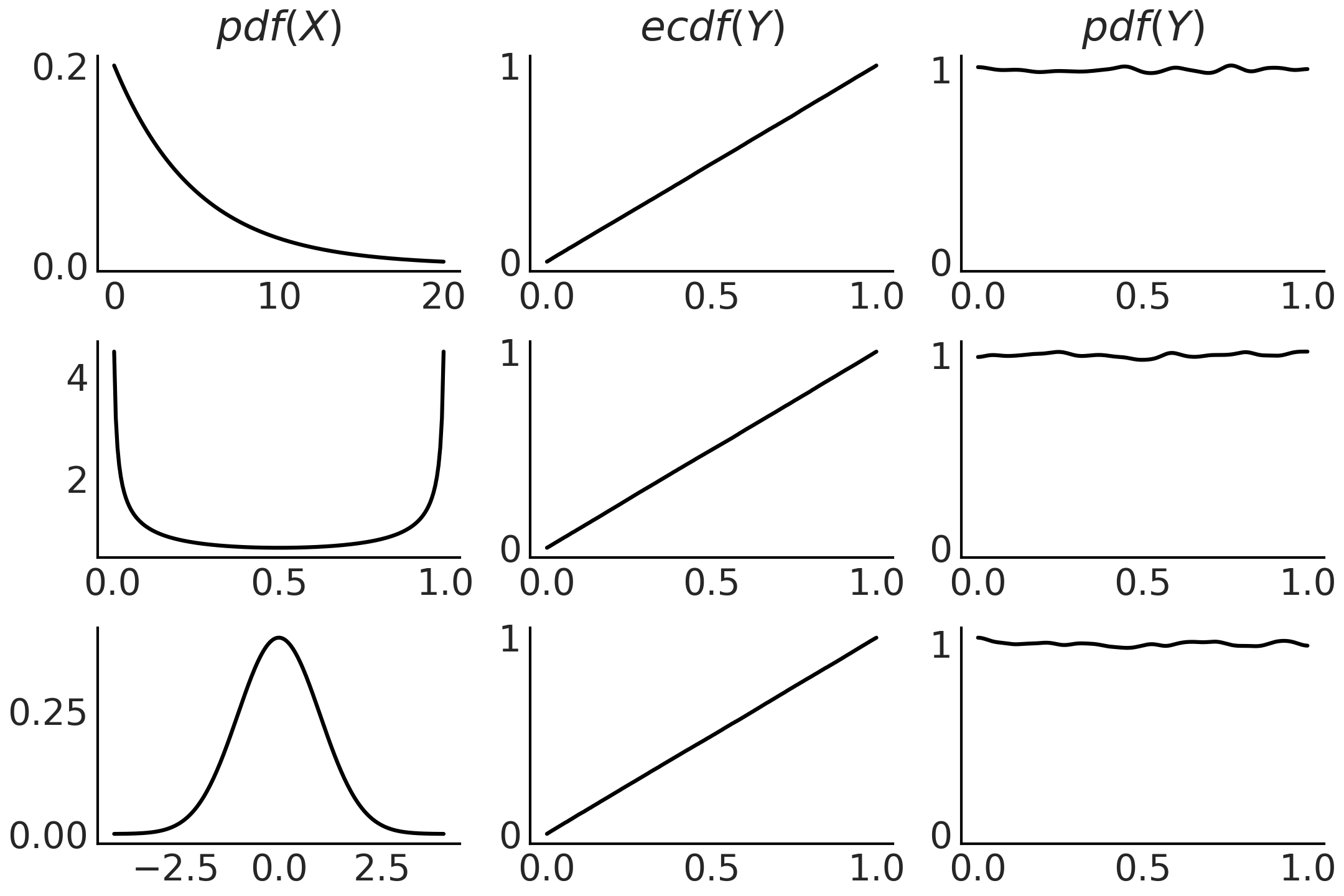

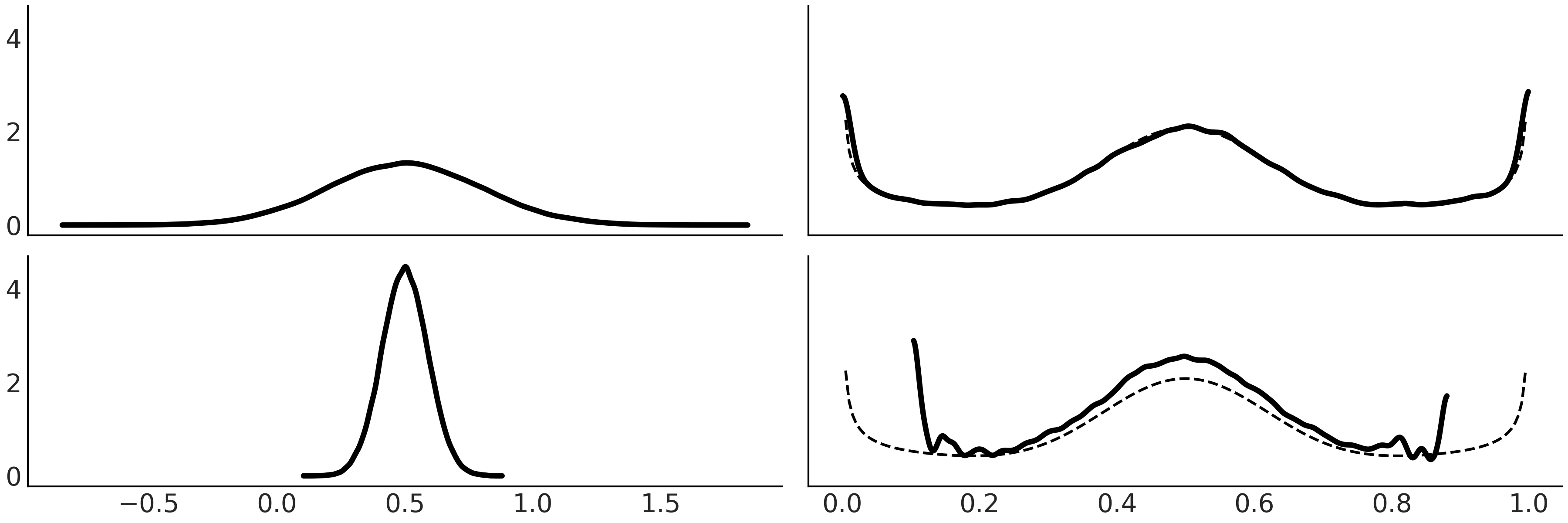

If we do not know the CDF \(F_X\) but we have samples from \(X\) we can approximate it with the empirical CDF. Fig. 11.17 shows example of this property generated with Code Block pit

xs = (np.linspace(0, 20, 200), np.linspace(0, 1, 200), np.linspace(-4, 4, 200))

dists = (stats.expon(scale=5), stats.beta(0.5, 0.5), stats.norm(0, 1))

_, ax = plt.subplots(3, 3)

for idx, (dist, x) in enumerate(zip(dists, xs)):

draws = dist.rvs(100000)

data = dist.cdf(draws)

# PDF original distribution

ax[idx, 0].plot(x, dist.pdf(x))

# Empirical CDF

ax[idx, 1].plot(np.sort(data), np.linspace(0, 1, len(data)))

# Kernel Density Estimation

az.plot_kde(data, ax=ax[idx, 2])

Fig. 11.17 On the first column we have the PDF of 3 different distributions. To generate the plots in the middle column, we take 100000 draws from the corresponding PDF compute the CDF for those draws. We can see these are the CDF for the Uniform distribution. The last column is similar to the middle one, except that instead of plotting the empirical CDF we use a a kernel density estimator to approximate the PDF, which we can see that is approximately Uniform. The figure was generated with Code Block pit.#

The probability integral transform is used as part of tests to evaluate

if a given dataset can be modeled as arising from a specified

distribution (or probabilistic model). In this book we have seen PIT

used behind both visual test az.plot_loo_pit() and

az.plot_pbv(kind="u_values").

PIT can also be used to sample from distributions. If the random

variable \(X\) is distributed as \(\mathcal{U}(0,1)\), then \(Y = F^{-1}(X)\)

has the distribution \(F\). Thus to obtain samples from a distribution we

just need (pseudo)random number generator like np.random.rand() and

the inverse CDF of the distribution of interest. This may not be the

most efficient method, but its generality and simplicity are difficult

to beat.

11.1.8. Expectations#

The expectation is a single number summarizing the center of mass of a distribution. For example, if \(X\) is a discrete random variable, then we can compute its expectation as:

As is often the case in statistics we want to also measure the spread, or dispersion, of a distribution, for example, to represent uncertainty around a point estimate like the mean. We can do this with the variance, which itself is also an expectation:

The variance often appears naturally in many computations, but to report results it is often more useful to take the square root of the variance, called the standard deviation, as this will be in the same units as the random variable.

Figures Fig. 11.4, Fig. 11.5, Fig. 11.6, Fig. 11.8, Fig. 11.9, Fig. 11.10, and Fig. 11.11 show the expectation and the standard deviations for different distributions. Notice that these are not values computed from samples but properties of theoretical mathematical objects.

Expectation is linear, meaning that:

where \(c\) is a constant and

which are true even in the case that \(X\) and \(Y\) are dependent. Instead, the variance is not linear:

and in general:

except, for example, when \(X\) and \(Y\) are independent.

We denote the \(n\)th moment of a random variable \(X\) is \(\mathbb{E}(X^n)\), thus the expected value and the variance are also known as the first and second moments of a distribution. The third moment, the skew, tells us about the asymmetry of a distribution. The skewness of a random variable \(X\) with mean \(\mu\) and variance \(\sigma^2\) is the third (standardized moment) of \(X\):

The reason to compute the skew as a standardized quantity, i.e. to subtract the mean and divide by the standard deviation is to make the skew independent of the localization and scale of \(X\), this is reasonable as we already have that information from the mean and variance and also it will make the skewness independent of the units of \(X\), so it becomes easier to compare skewness.

For example, a \(\text{Beta}(2, 2)\) has a 0 skew while for \(\text{Beta}(2, 5)\) the skew is positive and for \(\text{Beta}(5, 2)\) negative. For unimodal distributions, a positive skew generally means that the right tail is longer, and the opposite for a negative skew. This is not always the case, the reason is that a 0 skew means that the total mass at the tails on both sides is balanced. So we can also balance the mass by having one long thin tail an another short and fat tail.

The fourth moment, known as kurtosis, tells us about the behavior of the tails or the extreme values [133]. It is defined as

The reason to subtract 3 is to make the Gaussian have 0 kurtosis, as it is often the case that kurtosis is discussed in comparison with the Gaussian distribution, but sometimes it is often computed without the \(-3\), so when in doubt ask, or read, for the exact definition used in a particular case. By examining the definition of kurtosis in Equation (11.29) we can see that we are essentially computing the expected value of the standardized data raised to the fourth power. Thus any standardized values less than 1 contribute virtually nothing to the kurtosis. Instead the only values that has something to contribute are the extreme values.

As we increase increase the value of \(\nu\) in a Student t distribution the kurtosis decreases (it is zero for a Gaussain distribution) and the kurtosis increases as we decrease \(\nu\). The kurtosis is only defined when \(\nu > 4\), in fact for the Student T distribution the \(n\)th moment is only defined for \(\nu > n\).

The stats module of SciPy offers a method stats(moments) to compute

the moments of distributions as you can see in Code Block

scipy_unif where it is used to obtain the

mean and variance. We notice that all we have discussed in this section

is about computing expectation and moments from probability

distributions and not from samples, thus we are talking about properties

of theoretical distributions. Of course in practice we usually want to

estimate the moments of a distribution from data and for that reason

statisticians have studies estimators, for example, the sample mean and

the sample median are estimators of \(\mathbb{E}(X)\).

11.1.9. Transformations#

If we have a random variable \(X\) and we apply a function \(g\) to it we obtain another random variable \(Y = g(X)\). After doing so we may ask, given that we know the distribution of \(X\) how can we find out the distribution of \(Y\). One easy way of doing it, is by sampling from \(X\) applying the transformation and then plotting the results. But of course there are formals ways of doing it. One such way is applying the change of variables technique.

If \(X\) is a continuous random variable and \(Y = g(X)\), where \(g\) is a differentiable and strictly increasing or decreasing function, the PDF of \(Y\) is:

We can see this is true as follows. Let \(g\) be strictly increasing, then the CDF of \(Y\) is:

and then by the chain rule, the PDF of \(Y\) can be computed from the PDF of \(X\) as:

The proof for \(g\) strictly decreasing is similar but we end up with a minus sign on the right hand term and thus the reason we compute the absolute value in Equation (11.30).

For multivariate random variables (i.e in higher dimensions) instead of the derivative we need to compute the Jacobian determinant, and thus it is common to refer the term \(\left| \frac{dx}{dy} \right|\) as the Jacobian even in the one dimensional case. The absolute value of the Jacobian determinant at a point \(p\) gives us the factor by which a function \(g\) expands or shrinks volumes near \(p\). This interpretation of the Jacobian is also applicable to probability densities. If the transformation \(g\) is not linear then the affected probability distribution will shrink in some regions and expand in others. Thus we need to properly take into account these deformations when computing \(Y\) from the known PDF of \(X\). Slightly rewriting Equation (11.30) like below also helps:

As we can now see that the probability of finding \(Y\) in a tiny interval \(p_Y(y)dy\) is equal to the probability of finding \(X\) in a tiny interval \(p_X(x)dx\). So the Jacobian is telling us how we remap probabilities in the space associated to \(X\) with those associated with \(Y\).

11.1.10. Limits#

The two best known and most widely used theorems in probability are the law of large numbers and the central limit theorem. They both tell us what happens to the sample mean as the sample size increases. They can both be understood in the context of repeated experiments, where the outcome of the experiment could be viewed as a sample from some underlying distribution.

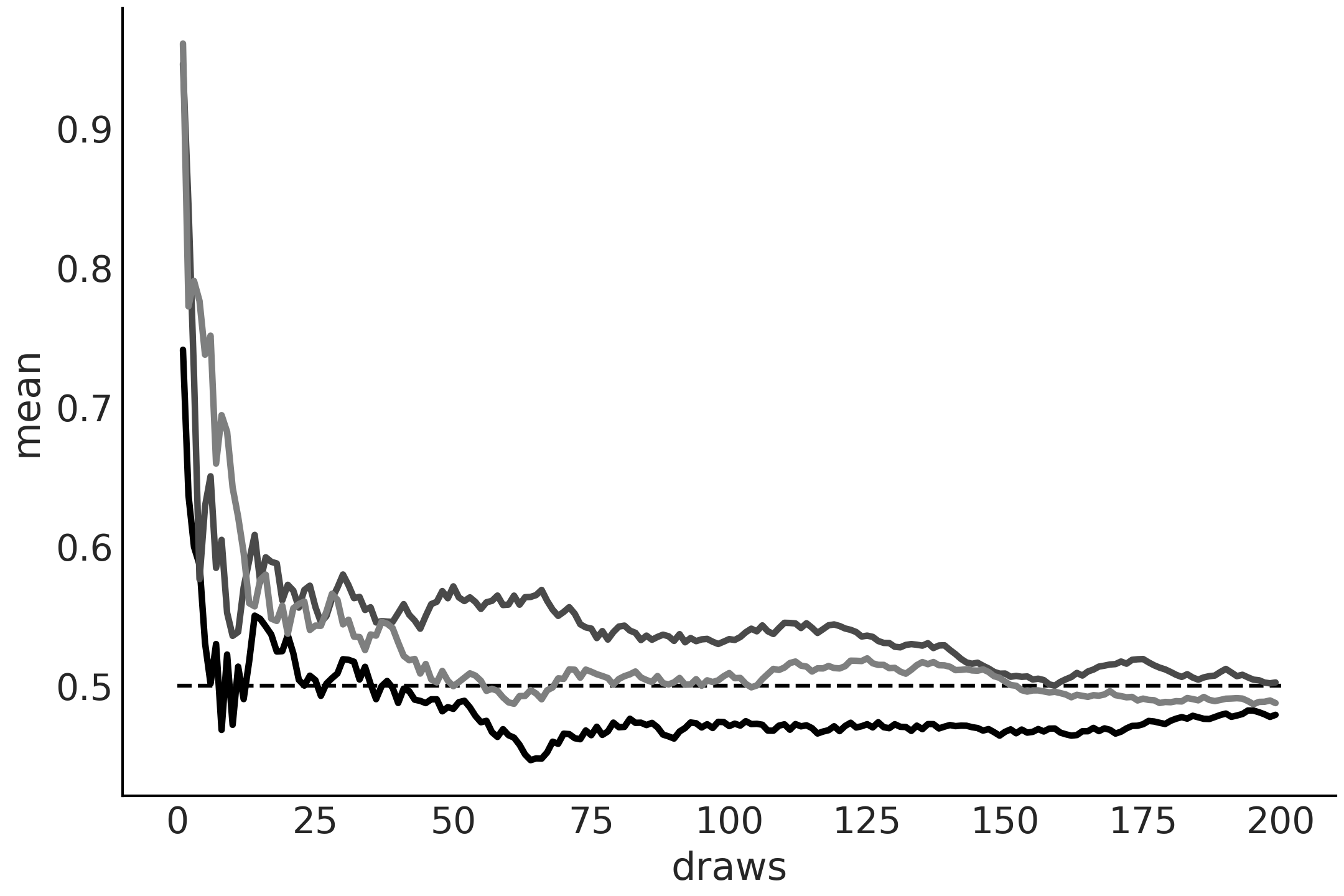

11.1.10.1. The Law of Large Numbers#

The law of large number tells us that the sample mean of an iid random variable converges, as the number of samples increase, to the expected value of the random variable. This is not true for some distributions such as the Cauchy distribution (which has no mean or finite variance).

The law of large numbers is often misunderstood, leading to the gambler’s fallacy. An example of this paradox is believing that it is smart to bet in the lottery on a number that has not appeared for a long time. The erroneous reasoning here is that if a particular number has not appeared for a while then there is must be some kind of force that increases the probability of that number in the next draws. A force that re-establish the equiprobability of the numbers and the natural order of the universe.

Fig. 11.18 Running values from a \(\mathcal{U}(0, 1)\) distribution. The dashed line at 0.5 represent the expected value. As the number of draws increases, the empirical mean approaches the expected value. Each line represents a different sample.#

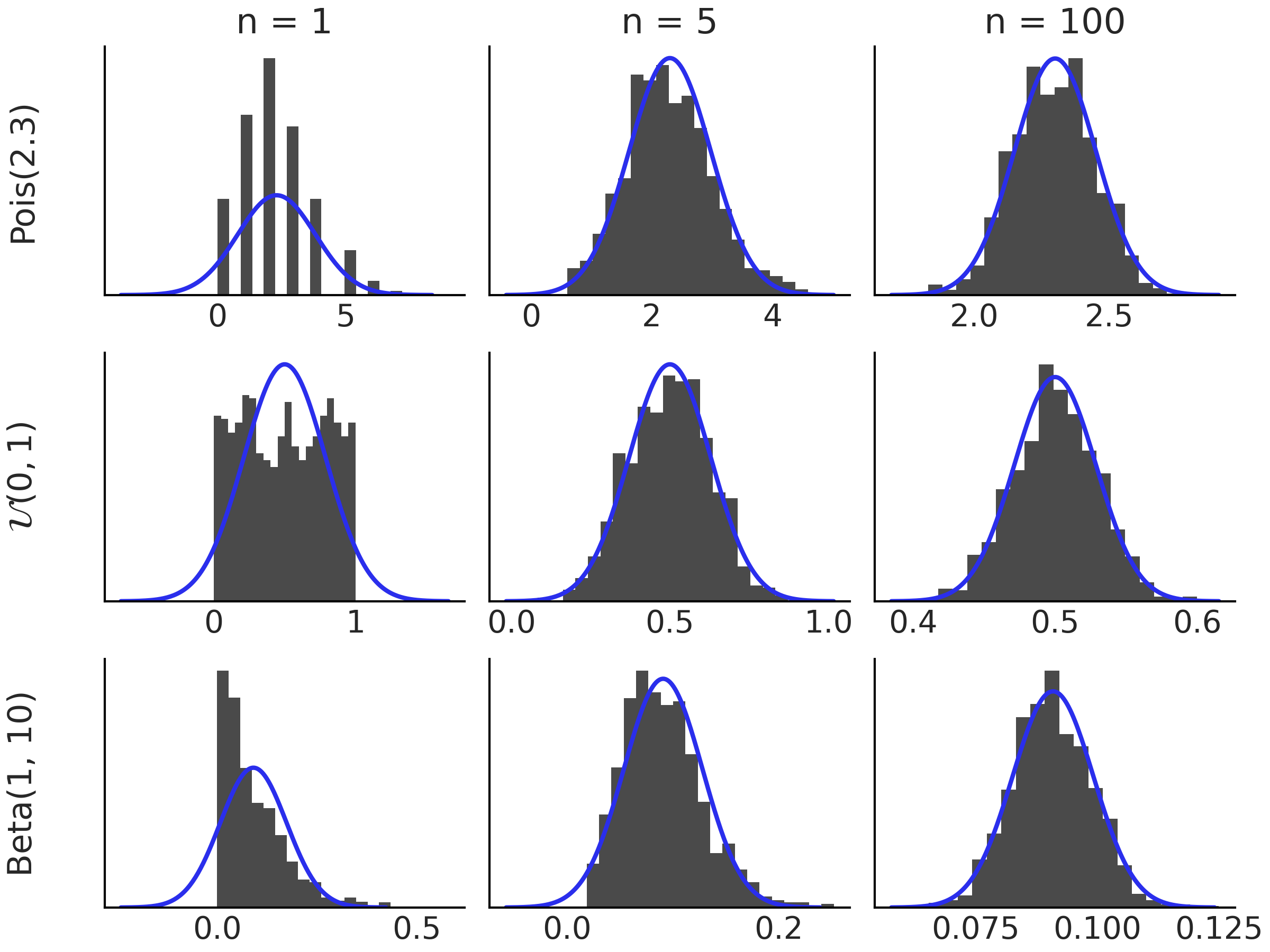

11.1.10.2. The Central Limit Theorem#

The central limit theorem states that if we sample \(n\) values independently from an arbitrary distribution the mean \(\bar X\) of those values will distribute approximately as a Gaussian as \({n \rightarrow \infty}\):

where \(\mu\) and \(\sigma^2\) are the mean and variance of the arbitrary distribution.

For the central limit theorem to be fulfilled, the following assumptions must be met:

The values are sampled independently

Each value come from the same distribution

The mean and standard deviation of the distribution must be finite

Criteria 1 and 2 can be relaxed quite a bit and we will still get roughly a Gaussian, but there is no way to escape from Criterion 3. For distributions such as the Cauchy distribution, which do not have a defined mean or variance, this theorem does not apply. The average of \(N\) values from a Cauchy distribution do not follow a Gaussian but a Cauchy distribution.

The central limit theorem explains the prevalence of the Gaussian distribution in nature. Many of the phenomena we study can be explained as fluctuations around a mean, or as the result of the sum of many different factors.

Fig. 11.19 shows the central limit theorem in action for 3 different distributions, \(\text{Pois}(2.3)\), \(\mathcal{U}(0, 1)\), \(\text{Beta}(1, 10)\), as \(n\) increases.

Fig. 11.19 Histograms of the distributions indicated on the left margin. Each histogram is based on 1000 simulated values of \(\bar{X_n}\). As we increase \(n\) the distribution of \(\bar{X_n}\) approach a Normal distribution. The black curve corresponds to a Gaussian distribution according to the central limit theorem.#

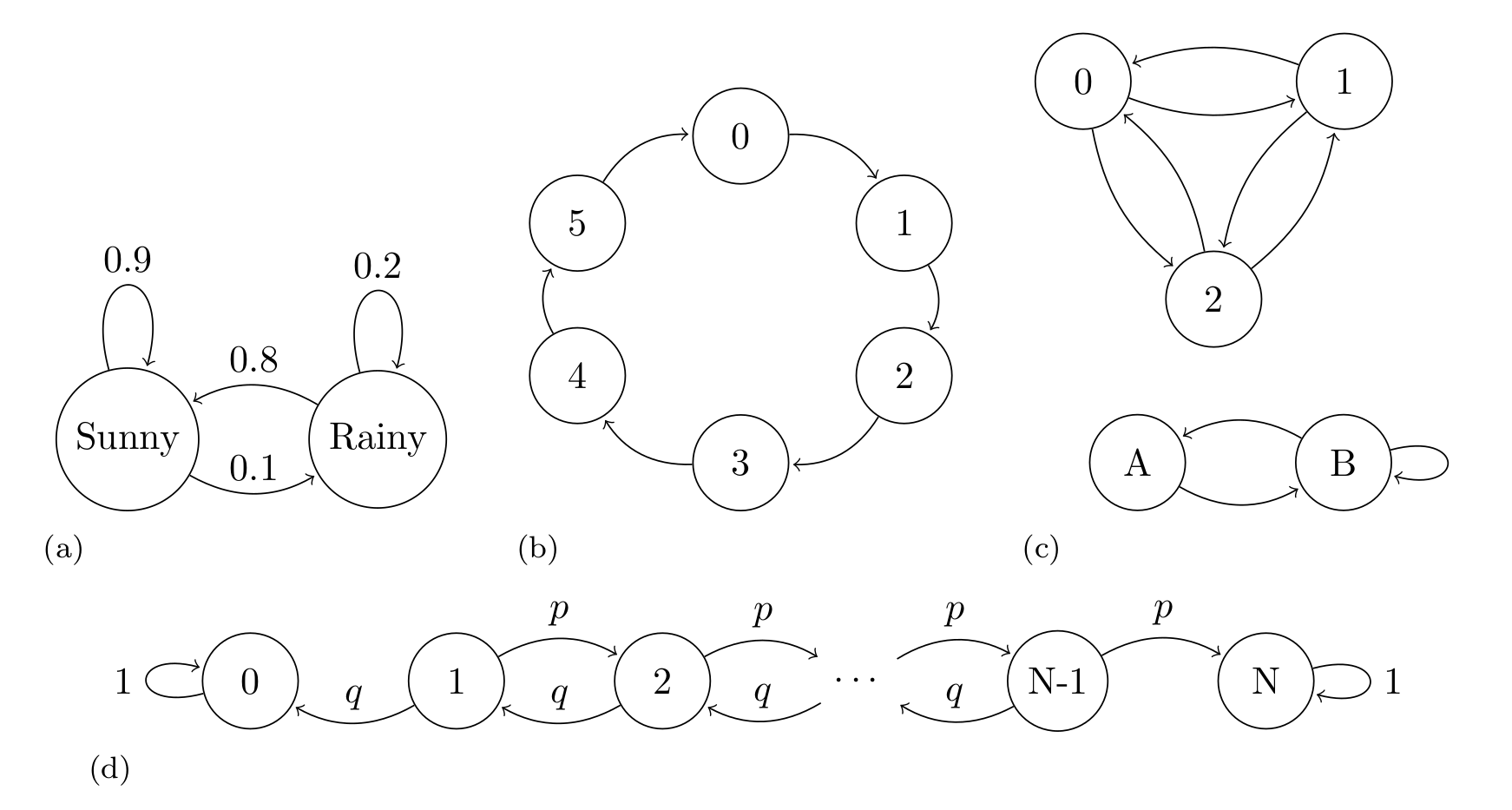

11.1.11. Markov Chains#

A Markov Chain is a sequence of random variables \(X_0, X_1, \dots\) for which the future state is conditionally independent from all past ones given the current state. In other words, knowing the current state is enough to know the probabilities for all future states. This is known as the Markov property and we can write it as:

A rather effective way to visualize Markov Chains is imagining you or some object moving in space [15]. The analogy is easier to grasp if the space is finite, for example, moving a piece in a square board like checkers or a salesperson visiting different cities. Given this scenarios you can ask questions like, how likely is to visit one state (specific squares in the board, cities, etc)? Or maybe more interesting if we keep moving from state to state how much time will we spend at each state in the long-run?

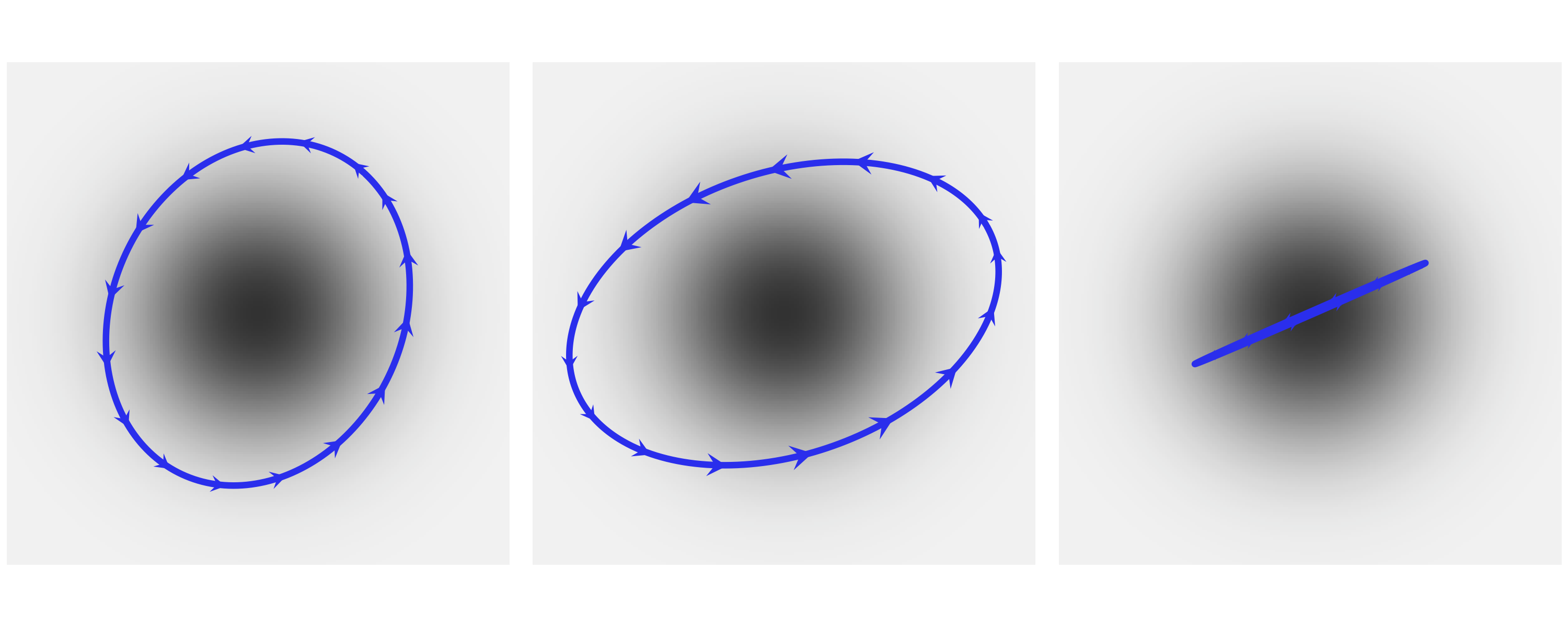

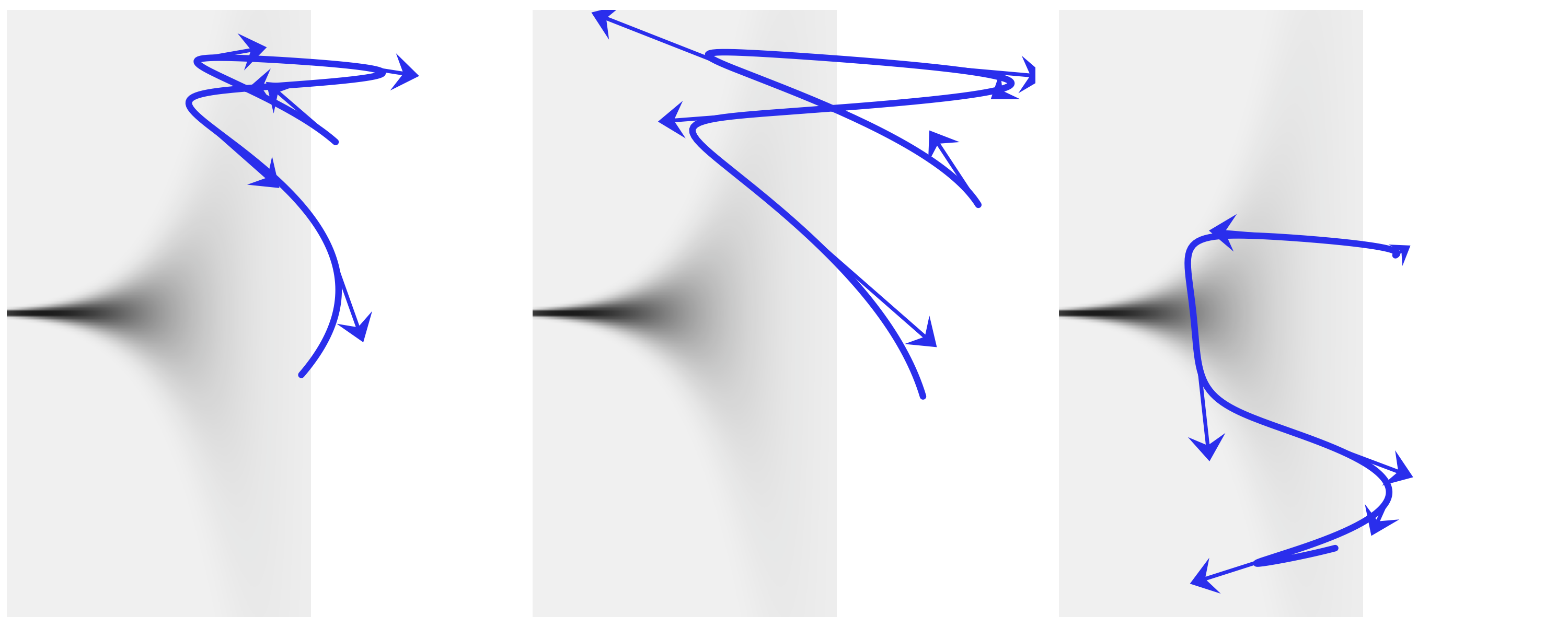

Fig. 11.20 shows four examples of Markov Chains, the first one show a classical example, an oversimplified weather model, where the states are rainy or sunny, the second example shows a deterministic die. The last two example are more abstract as we have not assigned any concrete representation to them.

Fig. 11.20 Markov Chains examples. (a) An oversimplified weather model, representing the probability of a rainy or sunny day, the arrows indicate the transition between states, the arrows are annotated with their corresponding transition probabilities. (b) An example of periodic Markov Chain. (c) An example of a disjoint chain. The states 1, 2, and 3 are disjoint from states A and B. If we start at the state 1, 2, or 3 we will never reach state A or B and vice versa. Transition probabilities are omitted in this example. (d) A Markov chain representing the gambler’s ruin problem, two gamblers, A and B, start with \(i\) and \(N-i\) units of money respectively. At any given money they bet 1 unit, gambler A has probability \(p\) of and probability \(q = 1 - p\) of losing. If \(X_n\) is the total money of gambler A at time \(n\). Then \(X_0, X_1, \dots\) is a Markov chain as the one represented.#

A convenient way to study Markov Chains is to collect the probabilities of moving between states in one step in a transition matrix \(\mathbf{T} = (t_{ij})\). For example, the transition matrix of example A in Fig. 11.20 is

and, for example, the transition matrix of example B in Fig. 11.20 is

The \(i\)th row of the transition matrix represents the conditional probability distribution of moving from state \(X_{n}\) to the state \(X_{n+1}\). That is, \(p(X_{n+1} \mid X_n = i)\). For example, if we are at state sunny we can move to sunny (i.e. stay at the same state) with probability 0.9 and move to state rainy with probability 0.1. Notice how the total probability of moving from sunny to somewhere is 1, as expected for a PMF.

Because of the Markov property we can compute the probability of \(n\) consecutive steps by taking the \(n\)th power of \(\mathbf{T}\).

We can also specify the starting point of the Markov chain, i.e. the initial conditions \(s_i = P(X_0 = i)\) and let \(\mathbf{s}=(s_1, \dots, s_M)\). With this information we can compute the marginal PMF of \(X_n\) as \(\mathbf{s}\mathbf{T}^n\).

When studying Markov chains it makes sense to define properties of individual states and also properties on the entire chain. For example, if a chain returns to a state over and over again we call that state recurrent. Instead a transient state is one that the chain will eventually leave forever, in example (d) in Fig. 11.20 all states other than 0 or \(N\) are transient. Also, we can call a chain irreducible if it is possible to get from any state to any other state in a finite number of steps example (c) in Fig. 11.20 is not irreducible, as states 1,2 and 3 are disconnected from states A and B.

Understanding the long-term behavior of Markov chains is of interest. In fact, they were introduced by Andrey Markov with the purpose of demonstrating that the law of large numbers can be applied also to non-independent random variables. The previously mentioned concepts of recurrence and transience are important for understanding this long-term run behavior. If we have a chain with transient and recurrent states, the chain may spend time in the transient states, but it will eventually spend all the eternity in the recurrent states. A natural question we can ask is how much time the chain is going to be at each state. The answer is provided by finding the stationary distribution of the chain.

For a finite Markov chain, the stationary distribution \(\mathbf{s}\) is a PMF such that \(\mathbf{s}\mathbf{T} = \mathbf{s}\) [16]. That is a distribution that is not changed by the transition matrix \(\mathbf{T}\). Notice that this does not mean the chain is not moving anymore, it means that the chain moves in such a way that the time it will spend at each state is the one defined by \(\mathbf{s}\). Maybe a physical analogy could helps here. Imagine we have a glass not completely filled with water at a given temperature. If we seal it with a cover, the water molecules will evaporate into the air as moisture. Interestingly it is also the case that the water molecules in the air will move to the liquid water. Initially more molecules might be going one way or another, but at a given point the system will find a dynamic equilibrium, with the same amount of water molecules moving to the air from the liquid water, as the number of water molecules moving from the liquid water to the air. In physics/chemistry this is called a steady-state, locally things are moving, but globally nothing changes [17]. Steady state is also an alternative name to stationary distribution.

Interestingly, under various conditions, the stationary distribution of a finite Markov chain exists and is unique, and the PMF of \(X_n\) converges to \(\mathbf{s}\) as \(n \to \infty\). Example (d) in Fig. 11.20 does not have a unique stationary distribution. We notice that once this chain reaches the states 0 or \(N\), meaning gambler A or B lost all the money, the chain stays in that state forever, so both \(s_0=(1, 0, \dots , 0)\) and \(s_N=(0, 0, \dots , 1)\) are both stationary distributions. On the contrary example B in Fig. 11.20 has a unique stationary distribution which is \(s=(1/6, 1/6, 1/6, 1/6, 1/6, 1/6)\), event thought the transition is deterministic.

If a PMF \(\mathbf{s}\) satisfies the reversibility condition (also known as detailed balance), that is \(s_i t_{ij} = s_j t_{ji}\) for all \(i\) and \(j\), we have the guarantee that \(\mathbf{s}\) is a stationary distribution of the Markov chain with transition matrix \(\mathbf{T} = t_{ij}\). Such Markov chains are called reversible. In Section Inference Methods we will use this property to show why Metropolis-Hastings is guaranteed to, asymptotically, work.

Markov chains satisfy a central limit theorem which is similar to Equation (11.34) except that instead of dividing by \(n\) we need to divide by the effective sample size (ESS). In Section Effective Sample Size we discussed how to estimate the effective sample size from a Markov Chain and how to use it to diagnose the quality of the chain. The square root of \(\frac{\sigma^2} {\text{ESS}}\) is the Monte Carlo standard error (MCSE) that we also discussed in Section Monte Carlo Standard Error.

11.2. Entropy#

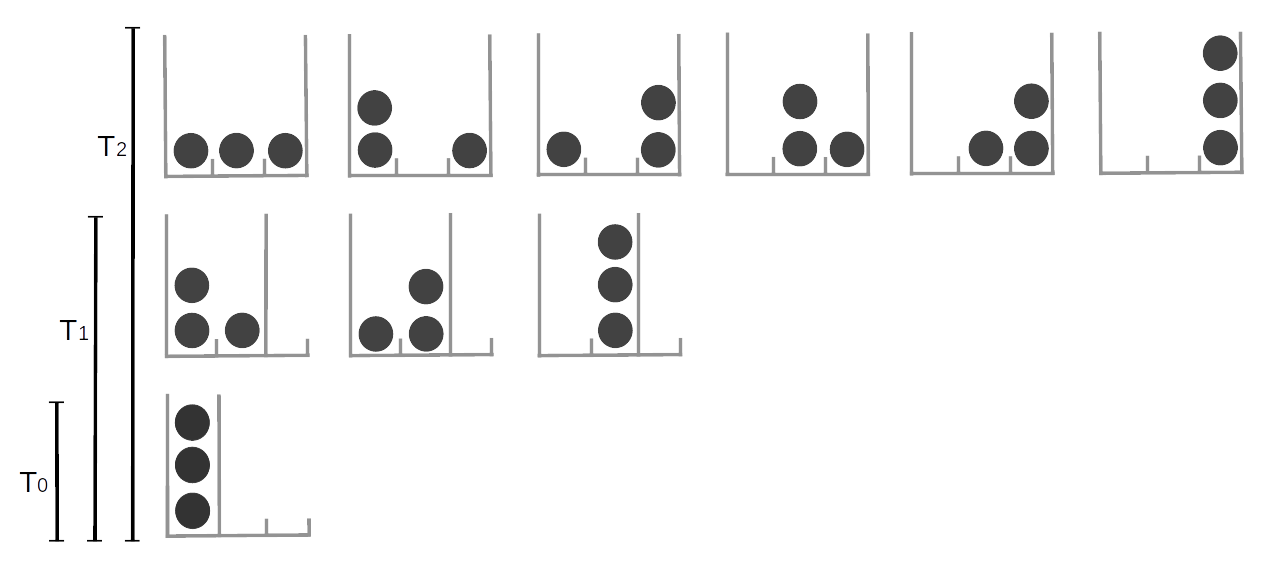

In the Zentralfriedhof, Vienna, we can find the grave of Ludwig Boltzmann. His tombstone has the legend \(S = k \log W\), which is a beautiful way of saying that the second law of thermodynamics is a consequence of the laws of probability. With this equation Boltzmann contributed to the development of one of the pillars of modern physics, statistical mechanics. Statistical mechanics describes how macroscopic observations such as temperature are related to the microscopic world of molecules. Imagine a glass with water, what we perceive with our senses is basically the average behavior of a huge number water molecules inside that glass [18]. At a given temperature there is a given number of arrangements of the water molecules compatible with that temperature (Figure Fig. 11.21). As we decrease the temperature we will find that less and less arrangements are possible until we find a single one. We have just reached 0 Kelvin, the lowest possible temperature in the universe! If we move into the other direction we will find that molecules can be found in more and more arrangements.

Fig. 11.21 The number of possible arrangements particles can take is related to the temperature of the system. Here we represent discrete system of 3 equivalent particles, the number of possible arrangements is represented by the available cells (gray high lines). increasing the temperature is equivalent to increasing the number of available cells. At \(T=0\) only one arrangement is possible, as the temperature increase the particles can occupy more and more states.#

We can analyze this mental experiment in terms of uncertainty. If we know a system is at 0 Kelvin we know the system can only be in a single possible arrangement, our certainty is absolute [19], as we increase the temperature the number of possible arrangements will increase and then it will become more and more difficult to say, “Hey look! Water molecules are in this particular arrangement at this particular time!” Thus our uncertainty about the microscopic state will increase. We will still be able to characterize the system by averages such the temperature, volume, etc, but at the microscopic level the certainty about particular arrangements will decrease. Thus, we can think of entropy as a way of measuring uncertainty.

The concept of entropy is not only valid for molecules. It could also be applies to arrangements of pixels, characters in a text, musical notes, socks, bubbles in a sourdough bread and more. The reason that entropy is so flexible is because it quantifies the arrangements of objects - it is a property of the underlying distributions. The larger the entropy of a distribution the less informative that distribution will be and the more evenly it will assign probabilities to its events. Getting an answer of “\(42\)” is more certain than “\(42 \pm 5\)”, which again more certain than “any real number”. Entropy can translate this qualitative observation into numbers.

The concept of entropy applies to continue and discrete distributions, but it is easier to think about it using discrete states and we will see some example in the rest of this section. But keep in mind the same concepts apply to the continuous cases.

For a probability distribution \(p\) with \(n\) possible different events which each possible event \(i\) having probability \(p_i\), the entropy is defined as:

Equation (11.36) is just a different way of writing the entropy engraved on Boltzmann’s tombstone. We annotate entropy using \(H\) instead of \(S\) and set \(k=1\). Notice that the multiplicity \(W\) from Boltzmann’s version is the total number of ways in which different outcomes can possibly occur:

You can think of this as rolling a t-sided die \(N\) times, where \(n_i\) is the number of times we obtain side \(i\). As \(N\) is large we can use Stirling’s approximation \(x! \approx (\frac{x}{e})^x\).

noticing that \(p_i = \frac{n_i}{N}\) we can write:

And finally by taking the logarithm we obtain

which is exactly the definition of entropy.

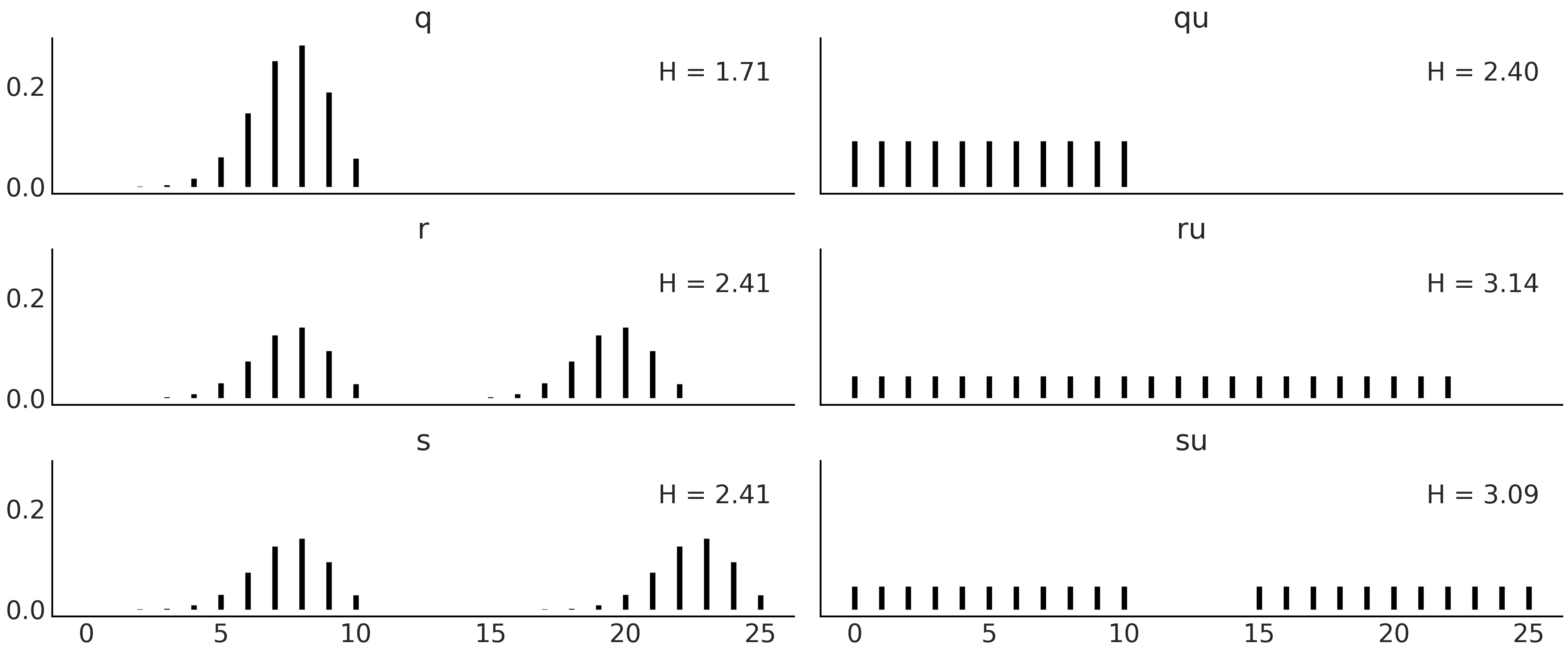

We will now show how to compute entropy in Python using Code Block entropy_dist, with the result shown in Fig. 11.22.

x = range(0, 26)

q_pmf = stats.binom(10, 0.75).pmf(x)

qu_pmf = stats.randint(0, np.max(np.nonzero(q_pmf))+1).pmf(x)

r_pmf = (q_pmf + np.roll(q_pmf, 12)) / 2

ru_pmf = stats.randint(0, np.max(np.nonzero(r_pmf))+1).pmf(x)

s_pmf = (q_pmf + np.roll(q_pmf, 15)) / 2

su_pmf = (qu_pmf + np.roll(qu_pmf, 15)) / 2

_, ax = plt.subplots(3, 2, figsize=(12, 5), sharex=True, sharey=True,

constrained_layout=True)

ax = np.ravel(ax)

zipped = zip([q_pmf, qu_pmf, r_pmf, ru_pmf, s_pmf, su_pmf],

["q", "qu", "r", "ru", "s", "su"])

for idx, (dist, label) in enumerate(zipped):

ax[idx].vlines(x, 0, dist, label=f"H = {stats.entropy(dist):.2f}")

ax[idx].set_title(label)

ax[idx].legend(loc=1, handlelength=0)

Fig. 11.22 Discrete distributions defined in Code Block entropy_dist and their entropy values \(H\).#

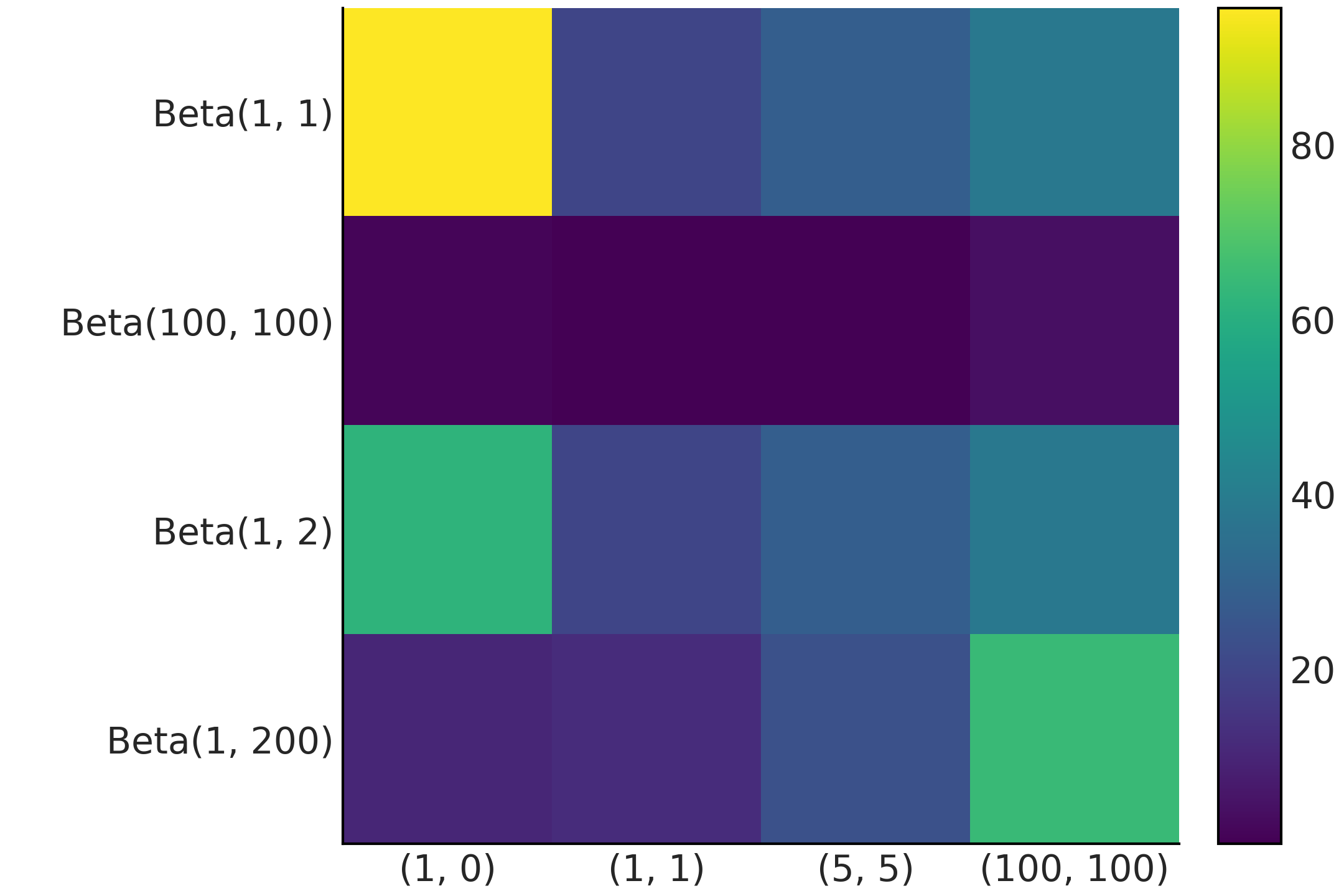

Fig. 11.22 shows six distributions, one per subplot with its corresponding entropy. There are a lot of things moving on in this figure, so before diving in be sure to set aside an adequate amount of time (this maybe a good time to check your e-mails before going on). The most peaked, or least spread distribution is \(q\), and this is the distribution with the lowest value of entropy among the six plotted distributions. \(q \sim \text{binom}({n=10, p=0.75})\), and thus there are 11 possible events. \(qu\) is a Uniform distribution with also 11 possible events. We can see that the entropy of \(qu\) is larger than \(q\), in fact we can compute the entropy for binomial distributions with \(n=10\) and different values of \(p\) and we will see that none of them have larger entropy than \(qu\). We will need to increase \(n\) \(\approx 3\) times to find the first binomial distribution with larger entropy than \(qu\). Let us move to the next row. We generate distribution \(r\) by taking \(q\) and shifting it to the right and then normalizing (to ensure the sum of all probabilities is 1). As \(r\) is more spread than \(q\) its entropy is larger. \(ru\) is the Uniform distribution with the same number of possible events as \(r\) (22), notice we are including as possible values those in the valley between both peaks. Once again the entropy of the Uniform version is the one with the largest entropy. So far entropy seems to be proportional to the variance of a distribution, but before jumping to conclusions let us check the last two distributions in Fig. 11.22. \(s\) is essentially the same as \(r\) but with a more extensive valley between both peaks and as we can see the entropy remains the same. The reason is basically that entropy does not care about those events in the valley with probability zero, it only cares about possible events. \(su\) is constructed by replacing the two peaks in \(s\) with \(qu\) (and normalizing). We can see that \(su\) has lower entropy than \(ru\) even when it looks more spread, after a more careful inspection we can see that \(su\) spread the total probability between fewer events (22) than \(ru\) (with 23 events), and thus it makes totally sense for it to have lower entropy.

11.3. Kullback-Leibler Divergence#

It is common in statistics to use one probability distribution \(q\) to represent another one \(p\), we generally do this when we do not know \(p\) but can approximate it with \(q\). Or maybe \(p\) is complex and we want to find a simpler or more convenient distribution \(q\). In such cases we may ask how much information are we losing by using \(q\) to represent \(p\), or equivalently how much extra uncertainty are we introducing. Intuitively, we want a quantity that becomes zero only when \(q\) is equal to \(p\) and be a positive value otherwise. Following the definition of entropy in Equation (11.36), we can achieve this by computing the expected value of the difference between \(\log(p)\) and \(\log(q)\). This is known as the Kullback-Leibler (KL) divergence:

Thus the \(\mathbb{KL}(p \parallel q)\) give us the average difference in log probabilities when using \(q\) to approximate \(p\). Because the events appears to us according to \(p\) we need to compute the expectation with respect to \(p\). For discrete distributions we have:

Using logarithmic properties we can write this into probably the most common way to represent KL divergence:

We can also arrange the term and write the \(\mathbb{KL}(p \parallel q)\) as:

and when we expand the above rearrangement we find that:

As we already saw in previous section, \(H(p)\) is the entropy of \(p\). \(H(p,q) = - \mathbb{E}_p[\log{q}]\) is like the entropy of \(q\) but evaluated according to the values of \(p\).

Reordering above we obtain:

This shows that the KL divergences can be effectively interpreted as the extra entropy with respect to \(H(p)\), when using \(q\) to represent \(p\).

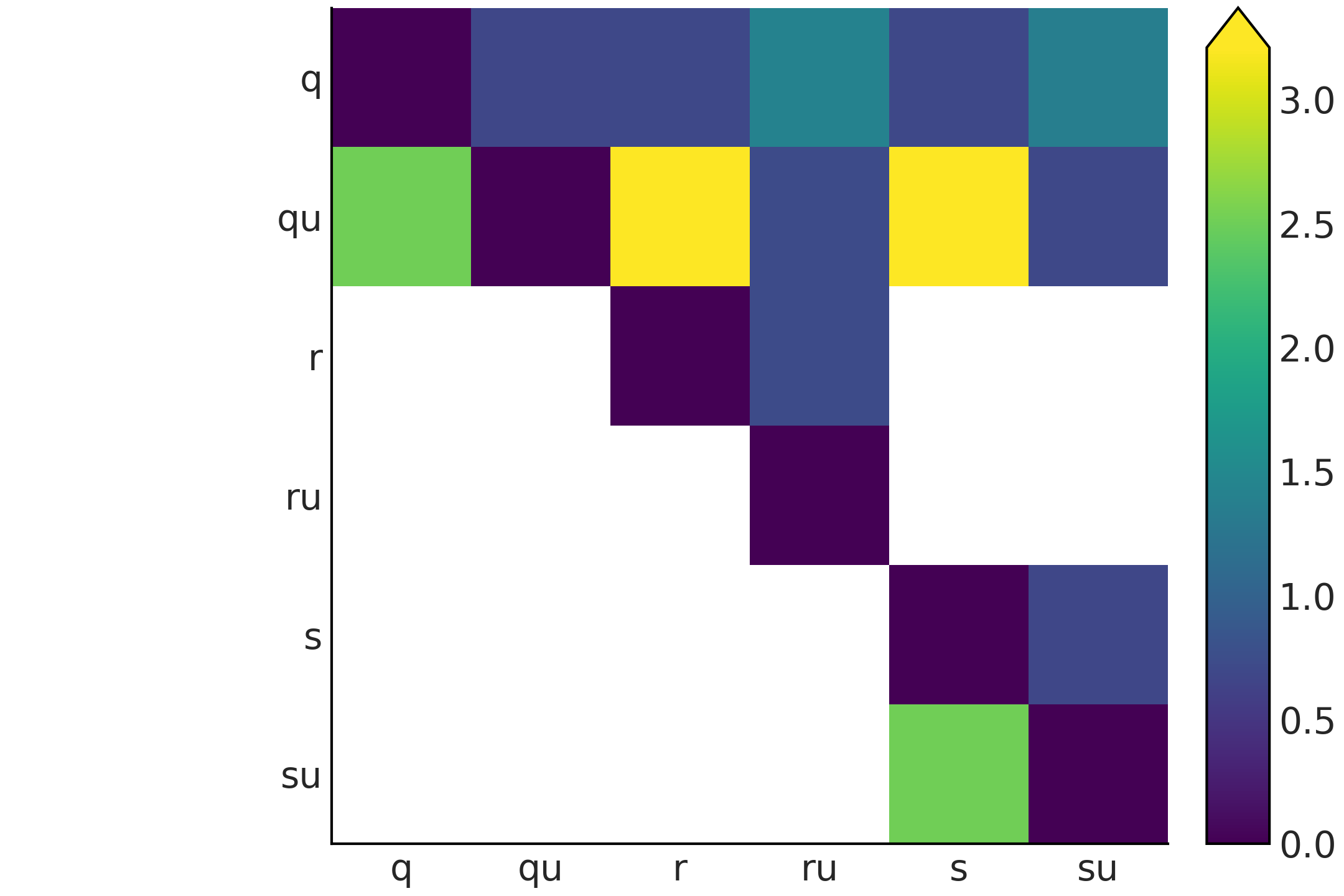

To gain a little bit of intuition we are going to compute a few values for the KL divergence and plot them., We are going to use the same distributions as in Fig. 11.22.

dists = [q_pmf, qu_pmf, r_pmf, ru_pmf, s_pmf, su_pmf]

names = ["q", "qu", "r", "ru", "s", "su"]

fig, ax = plt.subplots()

KL_matrix = np.zeros((6, 6))

for i, dist_i in enumerate(dists):

for j, dist_j in enumerate(dists):

KL_matrix[i, j] = stats.entropy(dist_i, dist_j)

im = ax.imshow(KL_matrix, cmap="cet_gray")

The result of Code Block kl_varies_dist is shown in Fig. 11.23. There are two features of Fig. 11.23 that immediately pop out. First, the figure is not symmetric, the reason is that \(\mathbb{KL}(p \parallel q)\) is not necessarily the same as \(\mathbb{KL}(q \parallel p)\). Second, we have many white cells. They represent \(\infty\) values. The definition of the KL divergence uses the following conventions [134]:

Fig. 11.23 KL divergence for all the pairwise combinations of the distributions q, qu, r, ru, s, and su shown in Fig. 11.22, the white color is used to represent infinity values.#

We can motivate the use of a log-score in computing expected log pointwise predictive density (introduced in Chapter 2 Equation (2.5)) based on the KL divergence. Let us assume we have \(k\) models posteriors \(\{q_{M_1}, q_{M_2}, \cdots q_{M_k}\}\), let further assume we know the true model \(M_0\) then we can compute:

This may seems a futile exercise as in real life we do not know the true model \(M_0\). The trick is to realize that as \(p_{M_0}\) is the same for all comparisons, thus building a ranking based on the KL-divergence is equivalent to doing one based on the log-score.

11.4. Information Criterion#

An information criterion is a measure of the predictive accuracy of a statistical model. It takes into account how well the model fits the data and penalizes the complexity of the model. There are many different information criterion based on how they compute these two terms. The most famous family member, especially for non-Bayesians, is the Akaike Information Criterion (AIC) [135]. It is defined as the sum of two terms. The \(\log p(y_i \mid \hat{\theta}_{mle})\) measures how well the model fits the data and the penalization term \(p_{AIC}\) to account for the fact that we use the same data to fit the model and to evaluate the model.

where \(\hat{\theta}_{mle}\) is the maximum-likelihood estimation of \(\boldsymbol{\theta}\) and \(p_{AIC}\) is just the number of parameters in the model.

AIC is quite popular in non-Bayesian settings, but is not well equipped to deal with the generality of Bayesian models. It does not use the full posterior distribution, thus discarding potentially useful information. On average, AIC will behave worse and worse as we move from flat prior into weakly-informative or informative priors, and/or if we add more structure into our model, like with hierarchical models. AIC assumes that the posterior can be well represented (at least asymptotically) by a Gaussian distribution, but this is not true for a number of models, including hierarchical models, mixture models, neural networks, etc. In summary we want to use some better alternatives.

The Widely applicable Information Crieria (WAIC [20]) [136] can be regarded as a fully Bayesian extension of AIC. It also contains two terms, roughly with the same interpretation as the Akaike criterion. The most important difference is that the terms are computed using the full posterior distribution.

The first term in Equation (11.50) is just the log-likelihood as in AIC but evaluated pointwise, i.e, at each \(i\) observed data-point over the \(n\) observations. We are taking into account the uncertainty in the posterior by taking the average over the \(s\) samples from the posterior. This first term is a practical way to compute the theoretical expected log pointwise predictive density (ELPD) as defined in Equation (2.4) and its approximation in Equation (2.5).

The second term might look a little bit weird, as is the variance over the \(s\) posterior samples (per observation). Intuitively, we can see that for each observation the variance will be low if the log-likelihood across the posterior distribution is similar and it will be larger if the log-likelihood varies more for different samples from the posterior distribution. The more observations we find to be sensitive to the details of the posterior the larger the penalization will be. We can also see this from another equivalent perspective; A more flexible model is one that can effectively accommodate more datasets. For example, a model that included straight but also upward curves is more flexible than one that only allows straight lines; and thus the log-likelihood of those observation evaluated across the posterior on the later model will have, on average, a higher variance. If the more flexible model is not able to compensate this penalization with a higher estimated ELPD then the simpler model will we ranked as a better choice. Thus the variance term in Equation (11.50) prevents overfitting by penalizing an overly complex model and it can be loosely interpreted as the effective number of parameters as in AIC.

Neither AIC nor WAIC are attempting to measure whether the model is true, they are only a relative measure to compare alternative models. From a Bayesian perspective the prior is part of the model, but WAIC is evaluated over the posterior, and the prior effect is only indirectly taken into account by the way it affects the resulting posterior. There are other information criteria like BIC and WBIC that attempts to answer that question and can be seen as approximations to the Marginal Likelihood, but we do not discuss them in this book.

11.5. LOO in Depth#

As discussed in Section Cross-validation and LOO in this book we use the term LOO to refer to a particular method to approximate Leave-One-Out Cross-Validation (LOO-CV) known as Pareto Smooth Importance Sampling Leave Once Out Cross Validation (PSIS-LOO-CV). In this section we are going to discuss a few details of this method.

LOO is an alternative to WAIC, in fact it can be shown that asymptotically they converge to the same numerical value [136, 137]. Nevertheless, LOO presents two importance advantages for practitioners. It is more robust in finite samples settings, and it provides useful diagnostics during computation [16, 137].

Under LOO-CV the expected log pointwise predictive density for a new dataset is:

where \(y_{-i}\) represents the dataset excluding the \(i\) observation.

Given that in practice we do not know the value of \(\boldsymbol{\theta}\) we can approximate Equation \(\ref{eq:elpd_loo_cv}\) using \(s\) samples from the posterior:

Notice that this term looks similar to the first term in Equation (11.50), except we are computing \(n\) posteriors removing one observation each time. For this reason, and contrary to WAIC, we do not need to add a penalization term. Computing \(\text{ELPD}_\text{LOO-CV}\) in (11.51) is very costly as we need to compute \(n\) posteriors. Fortunately if the \(n\) observations are conditionally independent we can approximate Equation (11.51) with Equation (11.52) [137, 138]:

where \(w\) is a vector of normalized weights.

To compute \(w\) we used importance sampling, this is a technique for estimating properties of a particular distribution \(f\) of interest, given that we only have samples from a different distribution \(g\). Using importance sampling makes sense when sampling from \(g\) is easier than sampling from \(f\). If we have a set of samples from the random variable \(X\) and we are able to evaluate \(g\) and \(f\) pointwise, we can compute the importance weights as:

Computationally, it goes as follow:

Draw \(N\) samples \(x_i\) from \(g\)

Calculate the probability of each sample \(g(x_i)\)

Evaluate \(f\) over the \(N\) samples \(f(x_i)\)

Calculate the importance weights \(w_i = \frac{f(x_i)}{g(x_i)}\)