Code 9: End to End Bayesian Workflows#

This is a reference notebook for the book Bayesian Modeling and Computation in Python

The textbook is not needed to use or run this code, though the context and explanation is missing from this notebook.

If you’d like a copy it’s available from the CRC Press or from Amazon. ``

import pandas as pd

import arviz as az

import matplotlib.pyplot as plt

import pymc3 as pm

import numpy as np

import theano.tensor as tt

from scipy import stats, optimize

np.random.seed(seed=233423)

sampling_random_seed = 0

az.style.use("arviz-grayscale")

plt.rcParams['figure.dpi'] = 300

Making a Model and Probably More Than One#

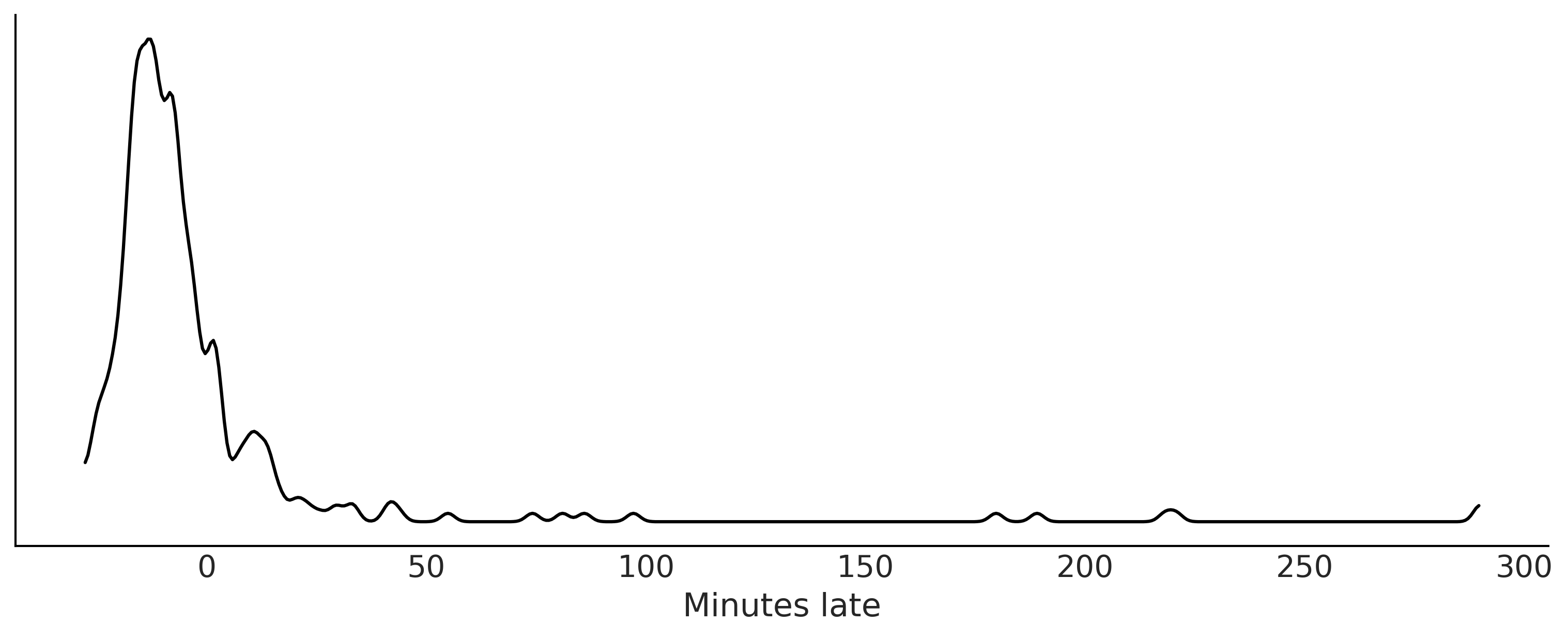

Code 9.1 and Figure 9.2#

df = pd.read_csv("../data/948363589_T_ONTIME_MARKETING.zip", low_memory=False)

fig, ax = plt.subplots(figsize=(10,4))

msn_arrivals = df[(df["DEST"] == 'MSN') & df["ORIGIN"]

.isin(["MSP", "DTW"])]["ARR_DELAY"]

az.plot_kde(msn_arrivals.values, ax=ax)

ax.set_yticks([])

ax.set_xlabel("Minutes late")

plt.savefig('img/chp09/arrivaldistributions.png')

msn_arrivals.notnull().value_counts()

True 336

Name: ARR_DELAY, dtype: int64

Code 9.2#

try:

# This is the real code, just try except block to allow for the whole notebook tor execute

with pm.Model() as normal_model:

normal_mu = ...

normal_sd = ...

normal_delay = pm.SkewNormal("delays", mu=normal_mu,

sd=normal_sd, observed=msn_arrivals)

with pm.Model() as skew_normal_model:

skew_normal_alpha = ...

skew_normal_mu = ...

skew_normal_sd = ...

skew_normal_delays = pm.SkewNormal("delays", mu=skew_normal_mu, sd=skew_normal_sd,

alpha=skew_normal_alpha, observed=msn_arrivals)

with pm.Model() as gumbel_model:

gumbel_beta = ...

gumbel_mu = ...

gumbel_delays = pm.Gumbel("delays", mu=gumbel_mu,

beta=gumbel_beta, observed=msn_arrivals)

except:

pass

Choosing Priors and Predictive Priors#

Code 9.3#

samples = 1000

with pm.Model() as normal_model:

normal_sd = pm.HalfStudentT("sd",sigma=60, nu=5)

normal_mu = pm.Normal("mu", 0, 30)

normal_delay = pm.Normal("delays", mu=normal_mu, sd=normal_sd, observed=msn_arrivals)

normal_prior_predictive = pm.sample_prior_predictive()

with pm.Model() as gumbel_model:

gumbel_beta = pm.HalfStudentT("beta", sigma=60, nu=5)

gumbel_mu = pm.Normal("mu", 0, 20)

gumbel_delays = pm.Gumbel("delays", mu=gumbel_mu, beta=gumbel_beta, observed=msn_arrivals)

gumbel_predictive = pm.sample_prior_predictive()

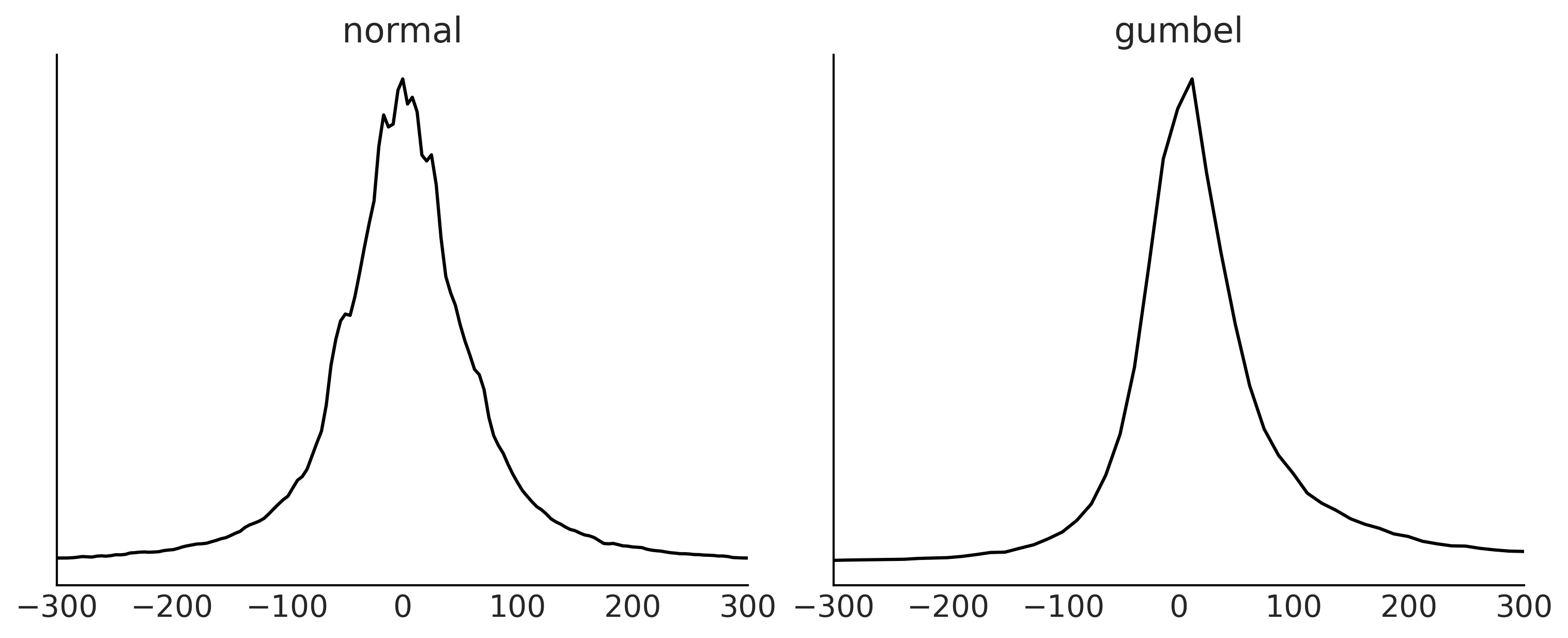

Figure 9.3#

fig, axes = plt.subplots(1, 2, figsize=(10, 4))

prior_predictives = {"normal":normal_prior_predictive, "gumbel": gumbel_predictive }

for i, (label, prior_predictive) in enumerate(prior_predictives.items()):

data = prior_predictive["delays"].flatten()

az.plot_dist(data, ax=axes[i])

axes[i].set_yticks([])

axes[i].set_xlim(-300, 300)

axes[i].set_title(label)

fig.savefig("img/chp09/Airline_Prior_Predictive.png")

Inference and Inference Diagnostics#

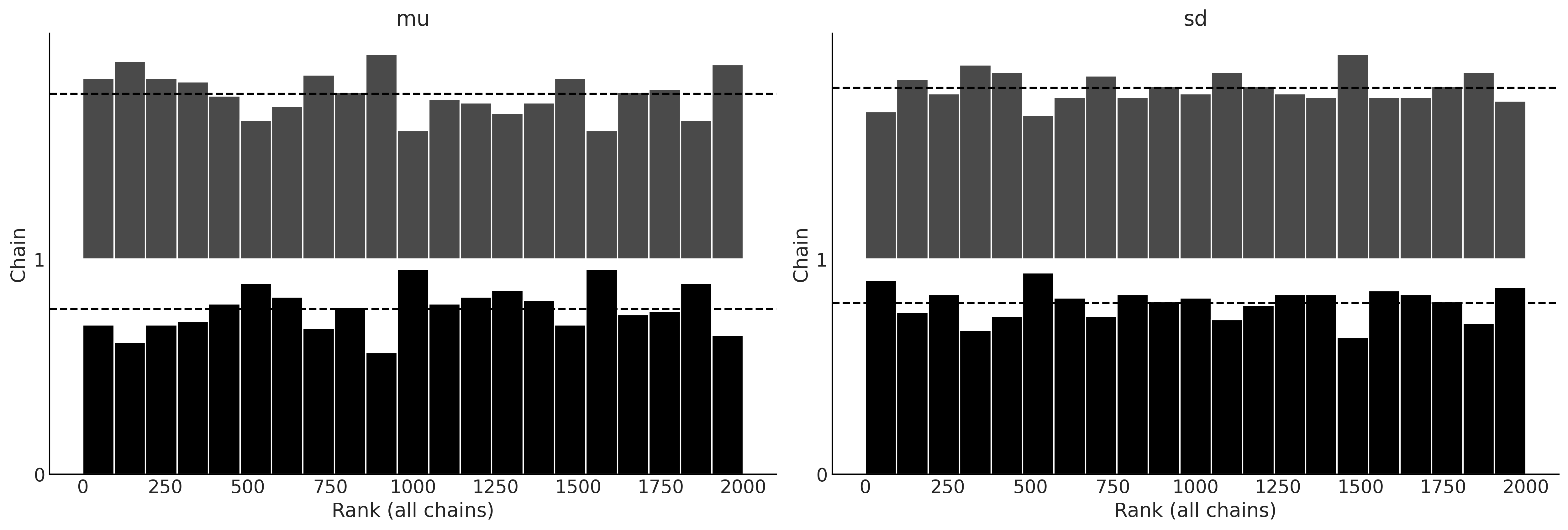

Code 9.4#

with normal_model:

normal_delay_trace = pm.sample(random_seed=0, chains=2)

az.plot_rank(normal_delay_trace)

plt.savefig('img/chp09/rank_plot_bars_normal.png')

/tmp/ipykernel_141130/700159645.py:2: FutureWarning: In v4.0, pm.sample will return an `arviz.InferenceData` object instead of a `MultiTrace` by default. You can pass return_inferencedata=True or return_inferencedata=False to be safe and silence this warning.

normal_delay_trace = pm.sample(random_seed=0, chains=2)

Auto-assigning NUTS sampler...

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (2 chains in 4 jobs)

NUTS: [mu, sd]

100.00% [4000/4000 00:01<00:00 Sampling 2 chains, 0 divergences]

Sampling 2 chains for 1_000 tune and 1_000 draw iterations (2_000 + 2_000 draws total) took 1 seconds.

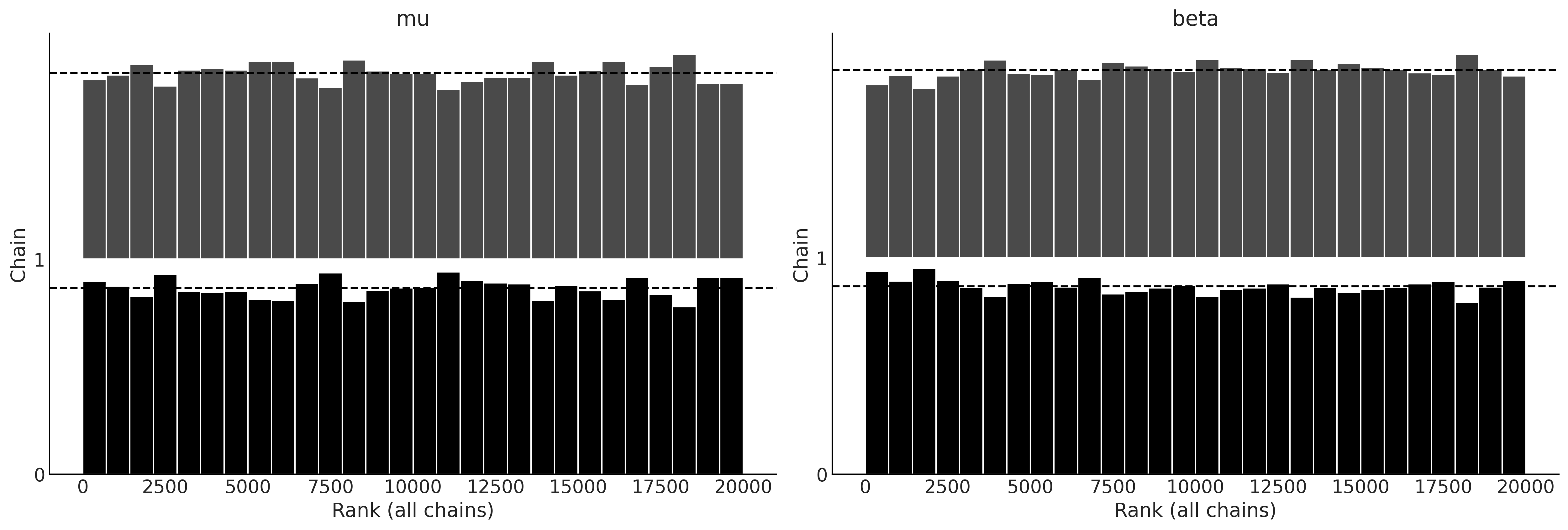

Figure 9.5#

with gumbel_model:

gumbel_delay_trace = pm.sample(random_seed=0, chains=2, draws=10000)

az.plot_rank(gumbel_delay_trace)

plt.savefig('img/chp09/rank_plot_bars_gumbel.png')

/tmp/ipykernel_141130/173437934.py:2: FutureWarning: In v4.0, pm.sample will return an `arviz.InferenceData` object instead of a `MultiTrace` by default. You can pass return_inferencedata=True or return_inferencedata=False to be safe and silence this warning.

gumbel_delay_trace = pm.sample(random_seed=0, chains=2, draws=10000)

Auto-assigning NUTS sampler...

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (2 chains in 4 jobs)

NUTS: [mu, beta]

100.00% [22000/22000 00:05<00:00 Sampling 2 chains, 0 divergences]

Sampling 2 chains for 1_000 tune and 10_000 draw iterations (2_000 + 20_000 draws total) took 5 seconds.

Posterior Plots#

Figure 9.6#

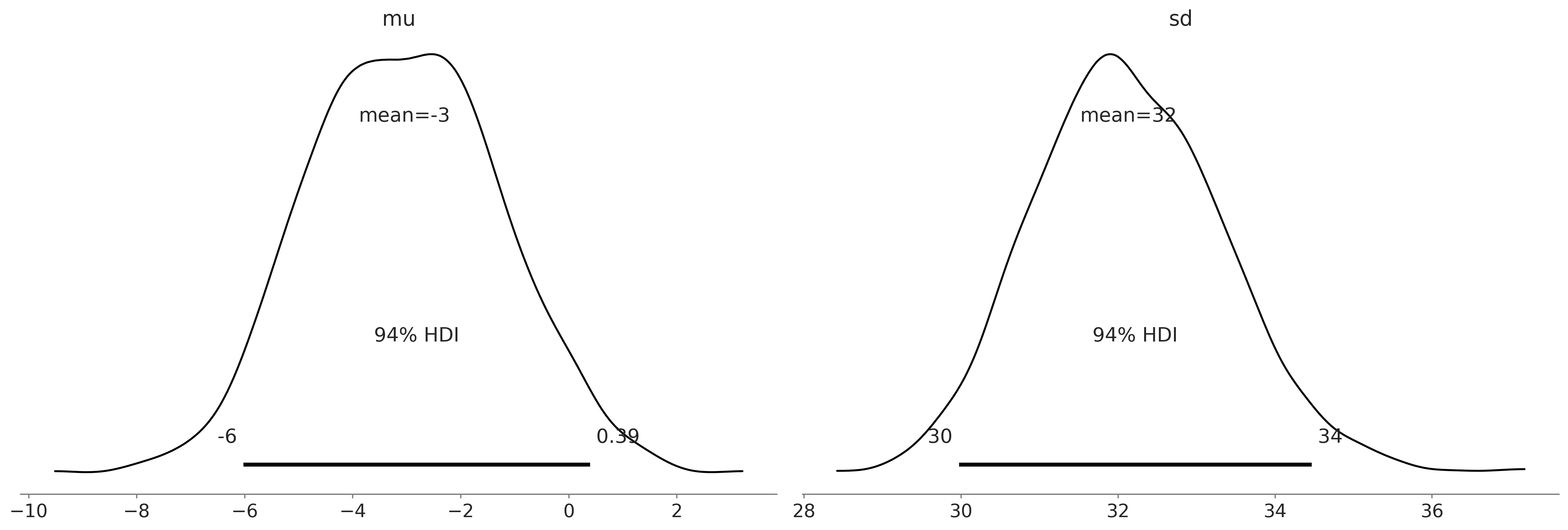

az.plot_posterior(normal_delay_trace)

plt.savefig('img/chp09/posterior_plot_delays_normal.png');

/home/canyon/miniconda3/envs/bmcp/lib/python3.9/site-packages/arviz/data/io_pymc3.py:96: FutureWarning: Using `from_pymc3` without the model will be deprecated in a future release. Not using the model will return less accurate and less useful results. Make sure you use the model argument or call from_pymc3 within a model context.

warnings.warn(

Figure 9.7#

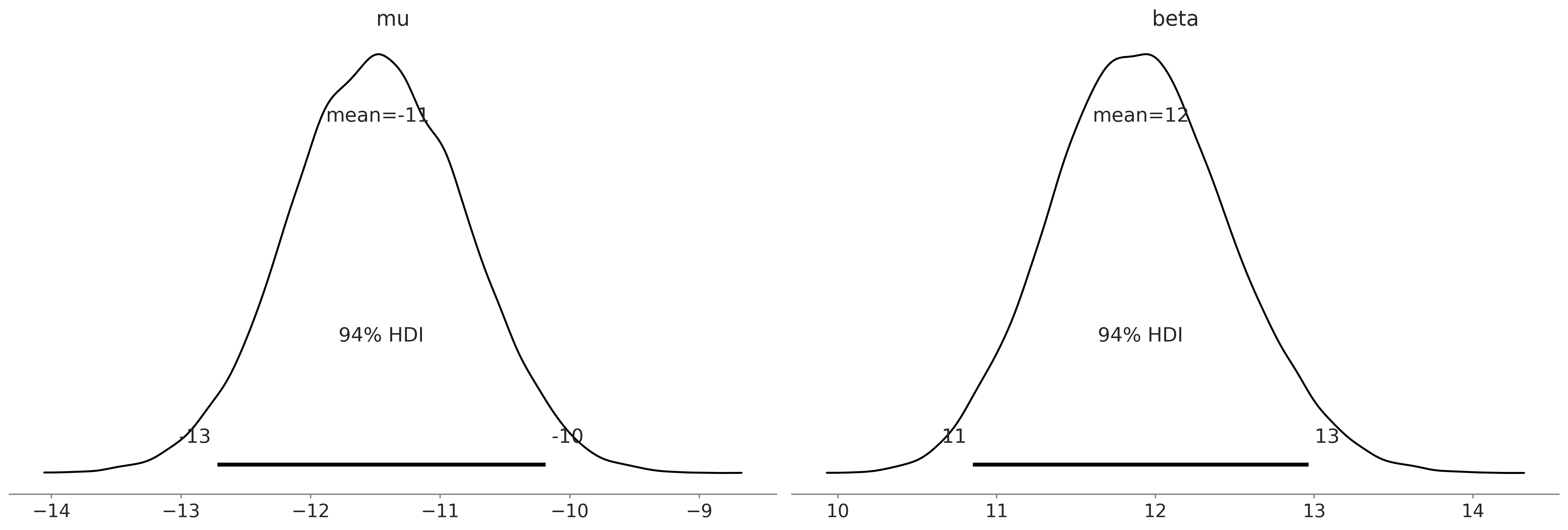

az.plot_posterior(gumbel_delay_trace)

plt.savefig('img/chp09/posterior_plot_delays_gumbel.png');

/home/canyon/miniconda3/envs/bmcp/lib/python3.9/site-packages/arviz/data/io_pymc3.py:96: FutureWarning: Using `from_pymc3` without the model will be deprecated in a future release. Not using the model will return less accurate and less useful results. Make sure you use the model argument or call from_pymc3 within a model context.

warnings.warn(

Evaluating Posterior Predictive Distributions#

Code 9.5#

with normal_model:

normal_delay_trace = pm.sample(random_seed=0)

normal_post_pred_check = pm.sample_posterior_predictive(normal_delay_trace, random_seed=0)

normal_data = az.from_pymc3(trace=normal_delay_trace, posterior_predictive=normal_post_pred_check)

/tmp/ipykernel_141130/2703936732.py:2: FutureWarning: In v4.0, pm.sample will return an `arviz.InferenceData` object instead of a `MultiTrace` by default. You can pass return_inferencedata=True or return_inferencedata=False to be safe and silence this warning.

normal_delay_trace = pm.sample(random_seed=0)

Auto-assigning NUTS sampler...

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [mu, sd]

100.00% [8000/8000 00:01<00:00 Sampling 4 chains, 0 divergences]

Sampling 4 chains for 1_000 tune and 1_000 draw iterations (4_000 + 4_000 draws total) took 1 seconds.

100.00% [4000/4000 00:02<00:00]

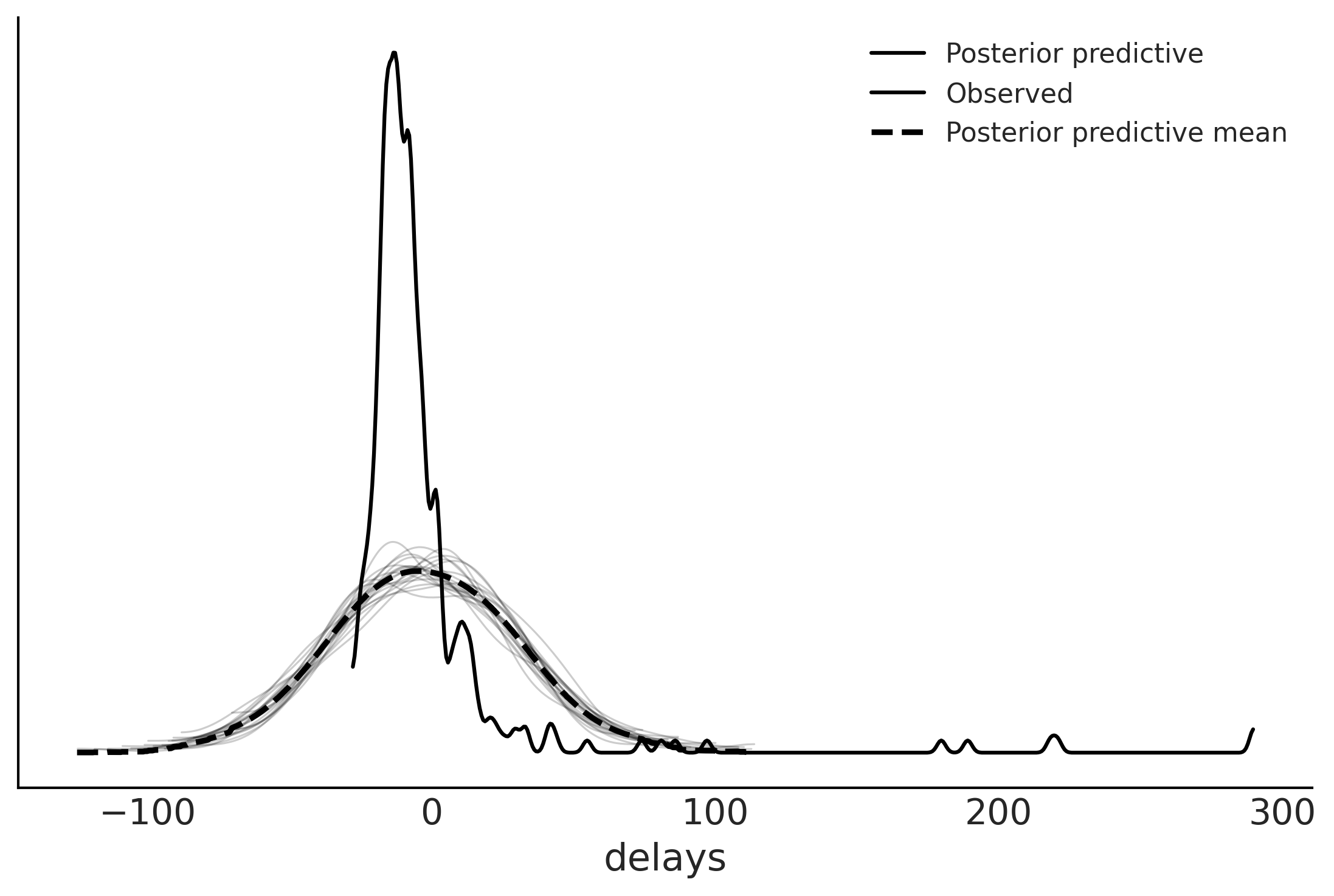

fig, ax = plt.subplots()

az.plot_ppc(normal_data, observed=True, num_pp_samples=20, ax=ax)

array([<AxesSubplot:xlabel='delays'>], dtype=object)

Gumbel Posterior Predictive#

with gumbel_model:

gumbel_post_pred_check = pm.sample_posterior_predictive(gumbel_delay_trace, random_seed=0)

gumbel_data = az.from_pymc3(trace=gumbel_delay_trace, posterior_predictive=gumbel_post_pred_check)

100.00% [20000/20000 00:05<00:00]

gumbel_data

arviz.InferenceData

-

- chain: 2

- draw: 10000

- chain(chain)int640 1

array([0, 1])

- draw(draw)int640 1 2 3 4 ... 9996 9997 9998 9999

array([ 0, 1, 2, ..., 9997, 9998, 9999])

- mu(chain, draw)float64-11.73 -11.73 ... -11.42 -12.0

array([[-11.72557194, -11.73207953, -11.88802422, ..., -11.6428163 , -12.32595871, -11.4247297 ], [-11.29462912, -11.69957094, -11.31910032, ..., -11.85237284, -11.41730207, -11.99712656]]) - beta(chain, draw)float6412.38 11.71 11.68 ... 12.35 11.91

array([[12.38449171, 11.70637023, 11.68447093, ..., 11.81750321, 10.59786029, 11.87224045], [12.23056892, 11.39189119, 11.98843791, ..., 12.31979166, 12.34786735, 11.90938563]])

- created_at :

- 2021-12-21T00:10:47.179307

- arviz_version :

- 0.11.2

- inference_library :

- pymc3

- inference_library_version :

- 3.11.4

- sampling_time :

- 5.16235613822937

- tuning_steps :

- 1000

<xarray.Dataset> Dimensions: (chain: 2, draw: 10000) Coordinates: * chain (chain) int64 0 1 * draw (draw) int64 0 1 2 3 4 5 6 7 ... 9993 9994 9995 9996 9997 9998 9999 Data variables: mu (chain, draw) float64 -11.73 -11.73 -11.89 ... -11.85 -11.42 -12.0 beta (chain, draw) float64 12.38 11.71 11.68 12.1 ... 12.32 12.35 11.91 Attributes: created_at: 2021-12-21T00:10:47.179307 arviz_version: 0.11.2 inference_library: pymc3 inference_library_version: 3.11.4 sampling_time: 5.16235613822937 tuning_steps: 1000xarray.Dataset -

- chain: 2

- draw: 10000

- delays_dim_0: 336

- chain(chain)int640 1

array([0, 1])

- draw(draw)int640 1 2 3 4 ... 9996 9997 9998 9999

array([ 0, 1, 2, ..., 9997, 9998, 9999])

- delays_dim_0(delays_dim_0)int640 1 2 3 4 5 ... 331 332 333 334 335

array([ 0, 1, 2, ..., 333, 334, 335])

- delays(chain, draw, delays_dim_0)float64-5.399 1.811 ... -2.091 -8.277

array([[[ -5.39918599, 1.81073042, -3.2946677 , ..., 0.89360377, 5.43627698, 5.35459582], [-15.23911763, -11.54325394, -4.33765624, ..., -2.32076318, -10.73548035, -9.68943292], [ -3.47878177, -23.31334874, 7.18210296, ..., 12.09764485, -6.92212629, -26.47491552], ..., [ 19.62744814, -21.42421504, 10.95284825, ..., -9.71709578, 5.33410699, -38.74991123], [ -8.76684998, 2.28239284, 0.91624338, ..., -0.84032181, -26.65570676, -21.96005532], [ 18.23822167, -23.22701479, -24.07056654, ..., 7.50796401, 9.20984217, -10.16932615]], [[-25.08656409, 32.29002703, 1.4286298 , ..., -22.77197238, 6.02545546, -26.94436752], [-13.05694047, 11.19104228, -8.43757867, ..., -8.17775168, -21.09001986, -9.65141766], [ 13.68550605, -10.24803391, -19.32074521, ..., -10.30054528, -18.63370128, -5.15608323], ..., [ -4.68054661, -4.30929148, 14.00107491, ..., -5.42925437, 40.87039118, -12.66036448], [-11.35656758, -18.34786932, 10.53413128, ..., 3.04157587, -9.58325394, 10.6535498 ], [ 15.59245375, -24.92554845, -18.61216491, ..., -2.3732099 , -2.09126357, -8.27722622]]])

- created_at :

- 2021-12-21T00:10:47.779134

- arviz_version :

- 0.11.2

- inference_library :

- pymc3

- inference_library_version :

- 3.11.4

<xarray.Dataset> Dimensions: (chain: 2, draw: 10000, delays_dim_0: 336) Coordinates: * chain (chain) int64 0 1 * draw (draw) int64 0 1 2 3 4 5 6 ... 9994 9995 9996 9997 9998 9999 * delays_dim_0 (delays_dim_0) int64 0 1 2 3 4 5 6 ... 330 331 332 333 334 335 Data variables: delays (chain, draw, delays_dim_0) float64 -5.399 1.811 ... -8.277 Attributes: created_at: 2021-12-21T00:10:47.779134 arviz_version: 0.11.2 inference_library: pymc3 inference_library_version: 3.11.4xarray.Dataset -

- chain: 2

- draw: 10000

- delays_dim_0: 336

- chain(chain)int640 1

array([0, 1])

- draw(draw)int640 1 2 3 4 ... 9996 9997 9998 9999

array([ 0, 1, 2, ..., 9997, 9998, 9999])

- delays_dim_0(delays_dim_0)int640 1 2 3 4 5 ... 331 332 333 334 335

array([ 0, 1, 2, ..., 333, 334, 335])

- delays(chain, draw, delays_dim_0)float64-3.534 -3.902 ... -3.621 -3.579

array([[[-3.53439048, -3.90187189, -4.44373716, ..., -3.53897951, -3.64047448, -3.62150725], [-3.48017251, -3.88477064, -4.47279416, ..., -3.4853666 , -3.59787227, -3.57844796], [-3.47562643, -3.89313767, -4.48514071, ..., -3.4864381 , -3.6023663 , -3.56959192], ..., [-3.49086634, -3.88248397, -4.46118802, ..., -3.49282385, -3.60169973, -3.58979294], [-3.37381152, -3.90245873, -4.58894495, ..., -3.40512617, -3.55286045, -3.47393295], [-3.49952651, -3.87189112, -4.44334915, ..., -3.49370874, -3.59743377, -3.6039606 ]], [[-3.53031076, -3.87513381, -4.42036493, ..., -3.52048713, -3.61630371, -3.63183326], [-3.45473541, -3.87567622, -4.48657637, ..., -3.4588874 , -3.5763833 , -3.56008234], [-3.51091932, -3.86939578, -4.431172 , ..., -3.50150279, -3.6013569 , -3.61626774], ..., [-3.52732413, -3.90675173, -4.45466208, ..., -3.53605546, -3.64079446, -3.61204157], [-3.53696591, -3.88492316, -4.42446686, ..., -3.53145411, -3.62788608, -3.63300298], [-3.49229563, -3.90442959, -4.48207113, ..., -3.50649604, -3.62055516, -3.57932918]]])

- created_at :

- 2021-12-21T00:10:47.778088

- arviz_version :

- 0.11.2

- inference_library :

- pymc3

- inference_library_version :

- 3.11.4

<xarray.Dataset> Dimensions: (chain: 2, draw: 10000, delays_dim_0: 336) Coordinates: * chain (chain) int64 0 1 * draw (draw) int64 0 1 2 3 4 5 6 ... 9994 9995 9996 9997 9998 9999 * delays_dim_0 (delays_dim_0) int64 0 1 2 3 4 5 6 ... 330 331 332 333 334 335 Data variables: delays (chain, draw, delays_dim_0) float64 -3.534 -3.902 ... -3.579 Attributes: created_at: 2021-12-21T00:10:47.778088 arviz_version: 0.11.2 inference_library: pymc3 inference_library_version: 3.11.4xarray.Dataset -

- chain: 2

- draw: 10000

- chain(chain)int640 1

array([0, 1])

- draw(draw)int640 1 2 3 4 ... 9996 9997 9998 9999

array([ 0, 1, 2, ..., 9997, 9998, 9999])

- energy(chain, draw)float641.414e+03 1.414e+03 ... 1.413e+03

array([[1413.56759516, 1413.66645317, 1412.51776952, ..., 1413.15605825, 1417.31906336, 1415.53834784], [1415.43695773, 1413.68710622, 1412.78072417, ..., 1413.29482656, 1413.0416688 , 1413.24467953]]) - lp(chain, draw)float64-1.413e+03 ... -1.413e+03

array([[-1412.92279264, -1412.39209418, -1412.50542257, ..., -1412.33552248, -1415.65781452, -1412.31284368], [-1412.55101939, -1412.67841777, -1412.3605102 , ..., -1412.93059786, -1412.707442 , -1412.64082321]]) - diverging(chain, draw)boolFalse False False ... False False

array([[False, False, False, ..., False, False, False], [False, False, False, ..., False, False, False]]) - perf_counter_diff(chain, draw)float640.0001988 0.0003637 ... 0.000469

array([[0.00019882, 0.00036374, 0.00019469, ..., 0.00035138, 0.00035864, 0.00039643], [0.00037191, 0.00037544, 0.00035086, ..., 0.00042214, 0.00052719, 0.00046898]]) - perf_counter_start(chain, draw)float646.522e+04 6.522e+04 ... 6.522e+04

array([[65216.67777274, 65216.67806359, 65216.67851561, ..., 65221.25840127, 65221.25884183, 65221.25932031], [65216.74270444, 65216.74317043, 65216.74363424, ..., 65221.18862741, 65221.18914466, 65221.18976756]]) - acceptance_rate(chain, draw)float641.0 0.8449 0.9614 ... 1.0 0.9627

array([[1. , 0.84489221, 0.96144218, ..., 1. , 0.50463615, 1. ], [0.49189175, 0.75136164, 1. , ..., 1. , 1. , 0.96273944]]) - step_size_bar(chain, draw)float641.091 1.091 1.091 ... 1.088 1.088

array([[1.09064275, 1.09064275, 1.09064275, ..., 1.09064275, 1.09064275, 1.09064275], [1.08797744, 1.08797744, 1.08797744, ..., 1.08797744, 1.08797744, 1.08797744]]) - process_time_diff(chain, draw)float640.0001989 0.0003638 ... 0.0004691

array([[0.00019886, 0.00036381, 0.00019477, ..., 0.00035144, 0.00035879, 0.00039647], [0.00037207, 0.00037544, 0.00035088, ..., 0.00042222, 0.00052731, 0.0004691 ]]) - step_size(chain, draw)float640.9806 0.9806 ... 1.028 1.028

array([[0.98061996, 0.98061996, 0.98061996, ..., 0.98061996, 0.98061996, 0.98061996], [1.02810693, 1.02810693, 1.02810693, ..., 1.02810693, 1.02810693, 1.02810693]]) - tree_depth(chain, draw)int641 2 1 2 2 2 2 2 ... 2 2 1 2 2 2 2 2

array([[1, 2, 1, ..., 2, 2, 2], [2, 2, 2, ..., 2, 2, 2]]) - n_steps(chain, draw)float641.0 3.0 1.0 3.0 ... 3.0 3.0 3.0 3.0

array([[1., 3., 1., ..., 3., 3., 3.], [3., 3., 3., ..., 3., 3., 3.]]) - energy_error(chain, draw)float64-0.2766 -0.2273 ... -0.02728

array([[-0.27655277, -0.22733678, 0.03932085, ..., -0.32739556, 0.58803383, -0.72010242], [ 0. , -0.04548605, -0.10043066, ..., -0.16728129, -0.09807469, -0.02727579]]) - max_energy_error(chain, draw)float64-0.2766 0.4516 ... -0.209 0.1007

array([[-0.27655277, 0.45164441, 0.03932085, ..., -0.32739556, 1.32713678, -0.72010242], [ 0.73470561, 0.77202735, -0.10043066, ..., -0.39173419, -0.20904696, 0.10073477]])

- created_at :

- 2021-12-21T00:10:47.183586

- arviz_version :

- 0.11.2

- inference_library :

- pymc3

- inference_library_version :

- 3.11.4

- sampling_time :

- 5.16235613822937

- tuning_steps :

- 1000

<xarray.Dataset> Dimensions: (chain: 2, draw: 10000) Coordinates: * chain (chain) int64 0 1 * draw (draw) int64 0 1 2 3 4 5 ... 9995 9996 9997 9998 9999 Data variables: (12/13) energy (chain, draw) float64 1.414e+03 1.414e+03 ... 1.413e+03 lp (chain, draw) float64 -1.413e+03 ... -1.413e+03 diverging (chain, draw) bool False False False ... False False perf_counter_diff (chain, draw) float64 0.0001988 0.0003637 ... 0.000469 perf_counter_start (chain, draw) float64 6.522e+04 6.522e+04 ... 6.522e+04 acceptance_rate (chain, draw) float64 1.0 0.8449 0.9614 ... 1.0 0.9627 ... ... process_time_diff (chain, draw) float64 0.0001989 0.0003638 ... 0.0004691 step_size (chain, draw) float64 0.9806 0.9806 ... 1.028 1.028 tree_depth (chain, draw) int64 1 2 1 2 2 2 2 2 ... 2 2 1 2 2 2 2 2 n_steps (chain, draw) float64 1.0 3.0 1.0 3.0 ... 3.0 3.0 3.0 energy_error (chain, draw) float64 -0.2766 -0.2273 ... -0.02728 max_energy_error (chain, draw) float64 -0.2766 0.4516 ... -0.209 0.1007 Attributes: created_at: 2021-12-21T00:10:47.183586 arviz_version: 0.11.2 inference_library: pymc3 inference_library_version: 3.11.4 sampling_time: 5.16235613822937 tuning_steps: 1000xarray.Dataset -

- delays_dim_0: 336

- delays_dim_0(delays_dim_0)int640 1 2 3 4 5 ... 331 332 333 334 335

array([ 0, 1, 2, ..., 333, 334, 335])

- delays(delays_dim_0)float64-14.0 1.0 10.0 ... -9.0 -5.0 -17.0

array([-14., 1., 10., -15., -19., -4., -11., 15., 13., 41., -14., -25., -5., -19., -23., -15., -5., -10., -13., 2., -1., 8., -7., -13., -3., -2., -6., -6., -5., -3., -2., 3., 1., 5., -7., 7., -2., -3., -7., -10., -9., -6., 20., -9., 30., -12., -2., -8., -6., 11., 13., -5., -23., -11., -12., 3., -16., 23., -2., -14., -8., -11., 3., -23., -6., -15., -10., 55., -4., -1., -14., -19., 11., -15., -12., -18., -14., 8., 11., 6., 0., -19., -23., -11., -20., -20., -22., -9., 6., -17., 2., -15., -13., -13., -20., -18., -15., -13., -25., -5., -9., -2., -25., -5., -5., -21., 97., -14., -19., -28., -17., 26., 3., -8., 2., 8., 12., -18., -16., -16., -8., 1., 3., -4., -8., 8., -17., 44., -15., -13., -24., -16., -3., -10., -8., -8., -21., -13., -9., -13., -20., -7., -9., -16., -16., -23., -17., -16., -12., -22., -18., -7., -18., -21., -11., -11., -13., 290., 218., -21., -20., -8., -14., -17., 221., -9., -12., -8., -3., -13., -7., 3., 1., 2., 33., -6., -10., -9., 1., 0., 180., 81., -12., -26., -11., -19., -13., -5., -12., -6., -15., -14., 1., 0., -8., -5., -4., 0., -20., -13., -10., -25., -10., -19., -4., -23., -16., -7., -16., 12., 15., 11., -9., 13., -7., 2., -14., -10., -17., -15., -25., -25., -14., -16., -27., -13., -7., -17., -14., 86., -24., -17., -16., 10., 1., -18., 189., 3., -10., -11., -13., -9., -15., -4., -9., 17., -18., -9., -13., -17., -9., -15., -16., -13., -11., -7., -8., -15., 33., -24., 17., 10., 4., -10., -3., -2., 42., -5., 14., 20., -11., -14., -8., -7., 29., -12., -14., -7., -18., 14., 14., -22., -5., -19., -15., -18., -19., -9., -16., -12., -12., -12., -6., -11., -8., -18., -12., -16., -7., -14., -15., -3., -8., 9., -13., -15., -10., 9., -18., 22., -11., -17., -17., -2., -12., -25., 3., -12., 74., -17., -7., -14., -8., -8., -12., 0., -7., -6., -21., -16., -15., -2., -13., -9., -5., -17.])

- created_at :

- 2021-12-21T00:10:47.779793

- arviz_version :

- 0.11.2

- inference_library :

- pymc3

- inference_library_version :

- 3.11.4

<xarray.Dataset> Dimensions: (delays_dim_0: 336) Coordinates: * delays_dim_0 (delays_dim_0) int64 0 1 2 3 4 5 6 ... 330 331 332 333 334 335 Data variables: delays (delays_dim_0) float64 -14.0 1.0 10.0 ... -9.0 -5.0 -17.0 Attributes: created_at: 2021-12-21T00:10:47.779793 arviz_version: 0.11.2 inference_library: pymc3 inference_library_version: 3.11.4xarray.Dataset

Figure 9.8#

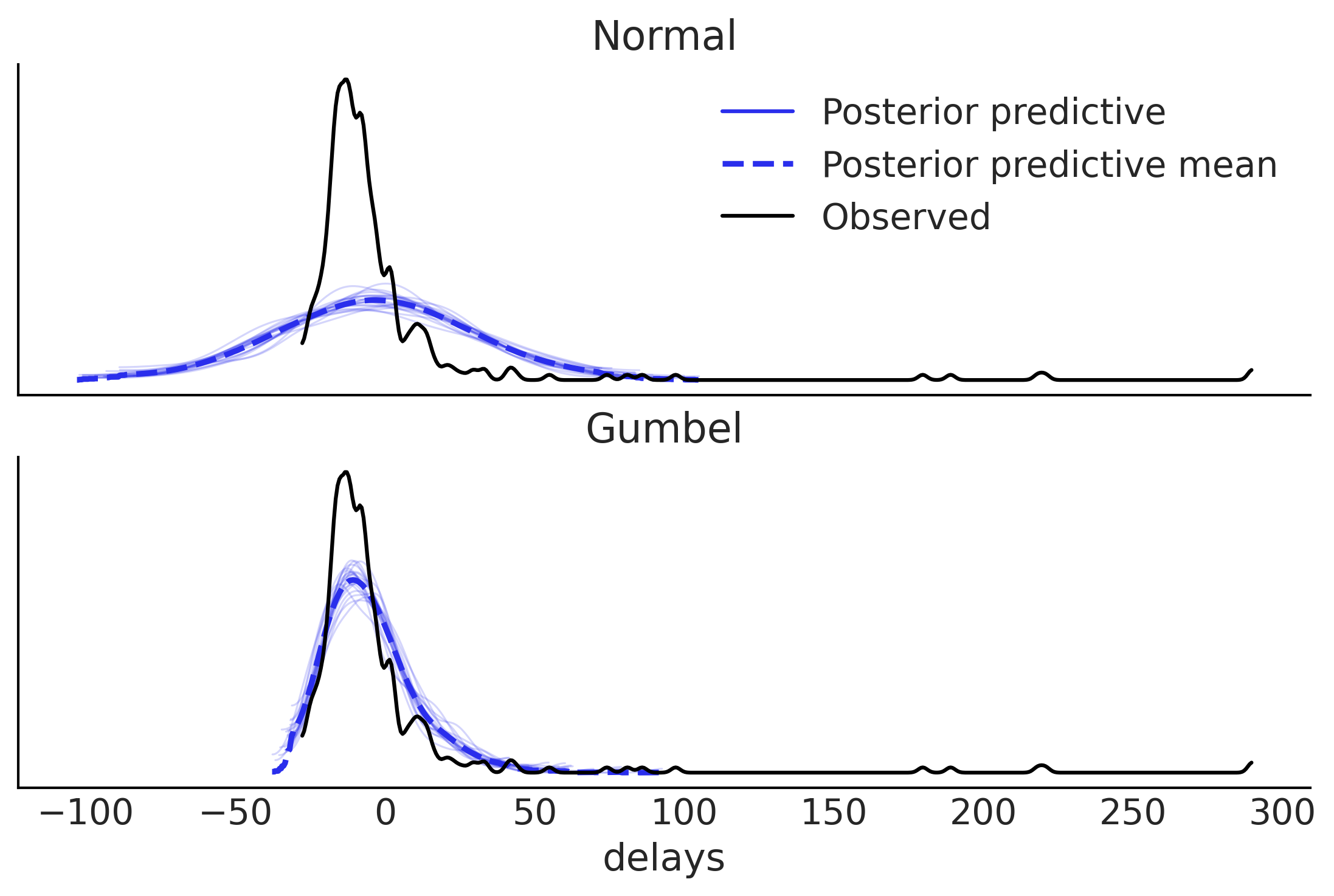

fig, ax = plt.subplots(2,1, sharex=True)

az.plot_ppc(normal_data, observed=False, num_pp_samples=20, ax=ax[0], color="C4")

az.plot_kde(msn_arrivals, ax=ax[0], label="Observed");

az.plot_ppc(gumbel_data, observed=False, num_pp_samples=20, ax=ax[1], color="C4")

az.plot_kde(msn_arrivals, ax=ax[1], label="Observed");

ax[0].set_title("Normal")

ax[0].set_xlabel("")

ax[1].set_title("Gumbel")

ax[1].legend().remove()

plt.savefig("img/chp09/delays_model_posterior_predictive.png")

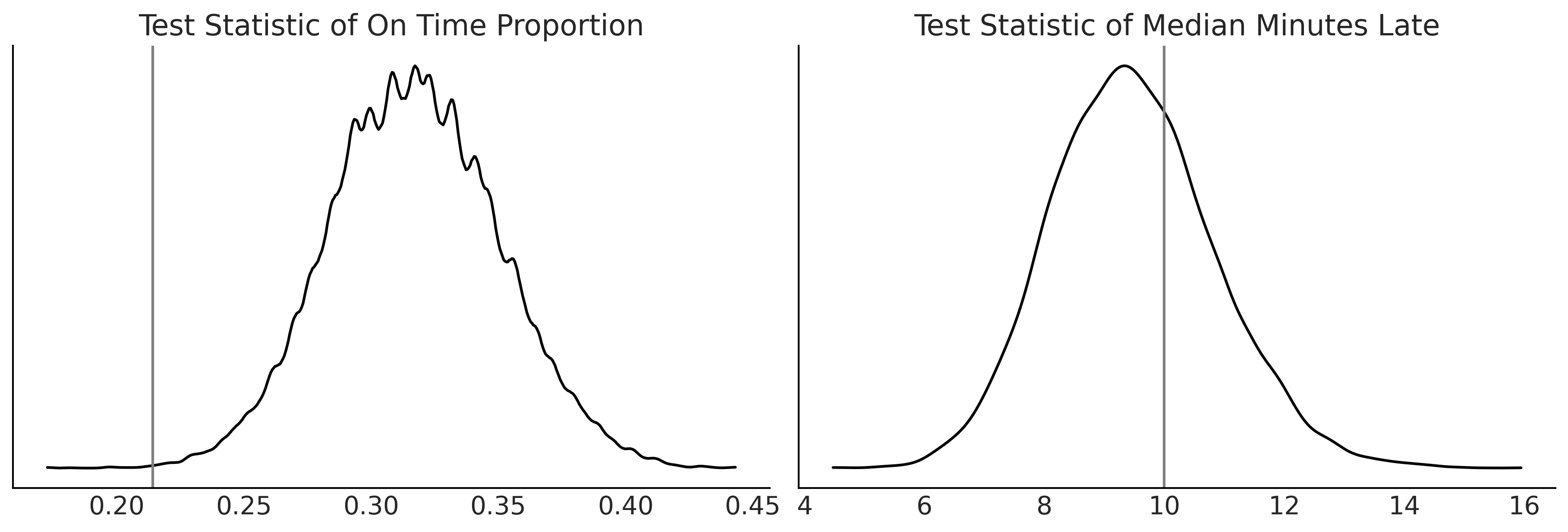

Figure 9.9#

gumbel_late = gumbel_data.posterior_predictive["delays"].values.reshape(-1, 336).copy()

dist_of_late = (gumbel_late > 0).sum(axis=1) / 336

fig, axes = plt.subplots(1,2, figsize=(12,4))

gumbel_late = gumbel_data.posterior_predictive["delays"].values.reshape(-1, 336).copy()

dist_of_late = (gumbel_late > 0).sum(axis=1) / 336

az.plot_dist(dist_of_late, ax=axes[0])

percent_observed_late = (msn_arrivals > 0).sum() / 336

axes[0].axvline(percent_observed_late, c="gray")

axes[0].set_title("Test Statistic of On Time Proportion")

axes[0].set_yticks([])

gumbel_late[gumbel_late < 0] = np.nan

median_lateness = np.nanmedian(gumbel_late, axis=1)

az.plot_dist(median_lateness, ax=axes[1])

median_time_observed_late = msn_arrivals[msn_arrivals >= 0].median()

axes[1].axvline(median_time_observed_late, c="gray")

axes[1].set_title("Test Statistic of Median Minutes Late")

axes[1].set_yticks([])

plt.savefig("img/chp09/arrival_test_statistics_for_gumbel_posterior_predictive.png")

Model Comparison#

Code 9.6#

compare_dict = {"normal": normal_data,"gumbel": gumbel_data}

comp = az.compare(compare_dict, ic="loo")

comp

/home/canyon/miniconda3/envs/bmcp/lib/python3.9/site-packages/arviz/stats/stats.py:145: UserWarning: The default method used to estimate the weights for each model,has changed from BB-pseudo-BMA to stacking

warnings.warn(

/home/canyon/miniconda3/envs/bmcp/lib/python3.9/site-packages/arviz/stats/stats.py:655: UserWarning: Estimated shape parameter of Pareto distribution is greater than 0.7 for one or more samples. You should consider using a more robust model, this is because importance sampling is less likely to work well if the marginal posterior and LOO posterior are very different. This is more likely to happen with a non-robust model and highly influential observations.

warnings.warn(

| rank | loo | p_loo | d_loo | weight | se | dse | warning | loo_scale | |

|---|---|---|---|---|---|---|---|---|---|

| gumbel | 0 | -1410.341706 | 5.846255 | 0.000000 | 1.000000e+00 | 45.130865 | 0.000000 | False | log |

| normal | 1 | -1653.653643 | 21.616843 | 243.311937 | 1.761862e-10 | 65.189335 | 27.416848 | True | log |

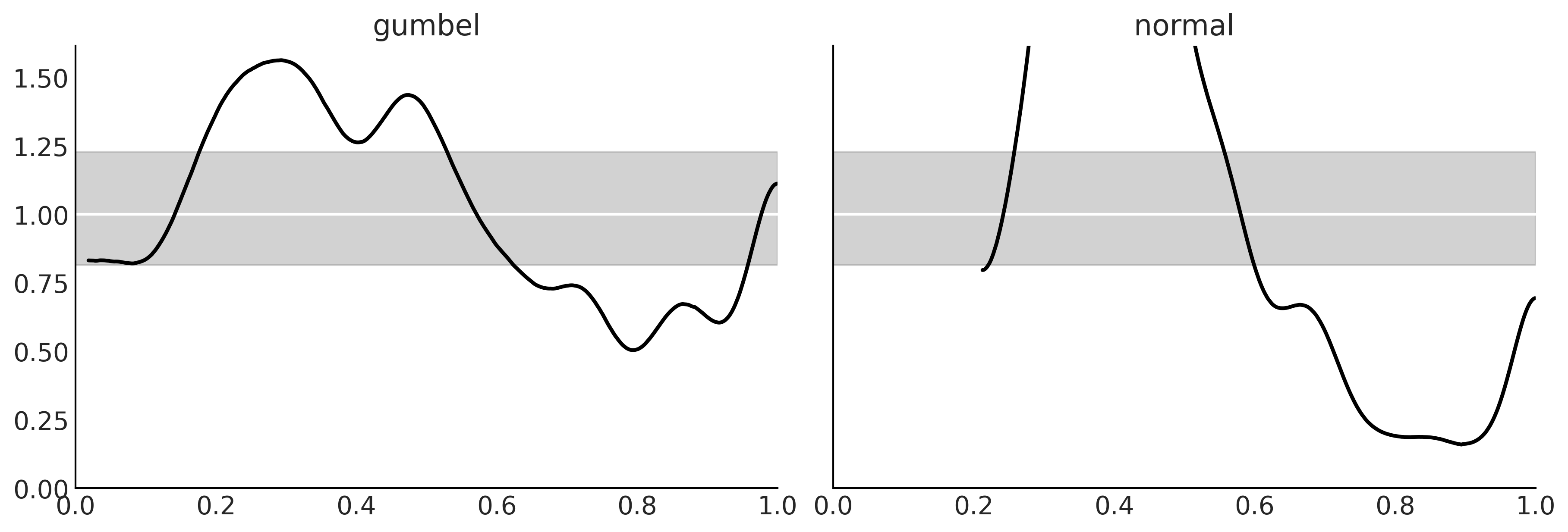

Figure 9.10#

_, axes = plt.subplots(1, 2, figsize=(12, 4), sharey=True)

for label, model, ax in zip(("gumbel", "normal"),(gumbel_data, normal_data), axes):

az.plot_loo_pit(model, y="delays", legend=False, use_hdi=True, ax=ax)

ax.set_title(label)

plt.savefig('img/chp09/loo_pit_delays.png')

Table 9.1#

cmp_dict = {"gumbel": gumbel_data,

"normal": normal_data}

cmp = az.compare(cmp_dict)

cmp

/home/canyon/miniconda3/envs/bmcp/lib/python3.9/site-packages/arviz/stats/stats.py:145: UserWarning: The default method used to estimate the weights for each model,has changed from BB-pseudo-BMA to stacking

warnings.warn(

/home/canyon/miniconda3/envs/bmcp/lib/python3.9/site-packages/arviz/stats/stats.py:655: UserWarning: Estimated shape parameter of Pareto distribution is greater than 0.7 for one or more samples. You should consider using a more robust model, this is because importance sampling is less likely to work well if the marginal posterior and LOO posterior are very different. This is more likely to happen with a non-robust model and highly influential observations.

warnings.warn(

| rank | loo | p_loo | d_loo | weight | se | dse | warning | loo_scale | |

|---|---|---|---|---|---|---|---|---|---|

| gumbel | 0 | -1410.341706 | 5.846255 | 0.000000 | 1.000000e+00 | 45.130865 | 0.000000 | False | log |

| normal | 1 | -1653.653643 | 21.616843 | 243.311937 | 1.761862e-10 | 65.189335 | 27.416848 | True | log |

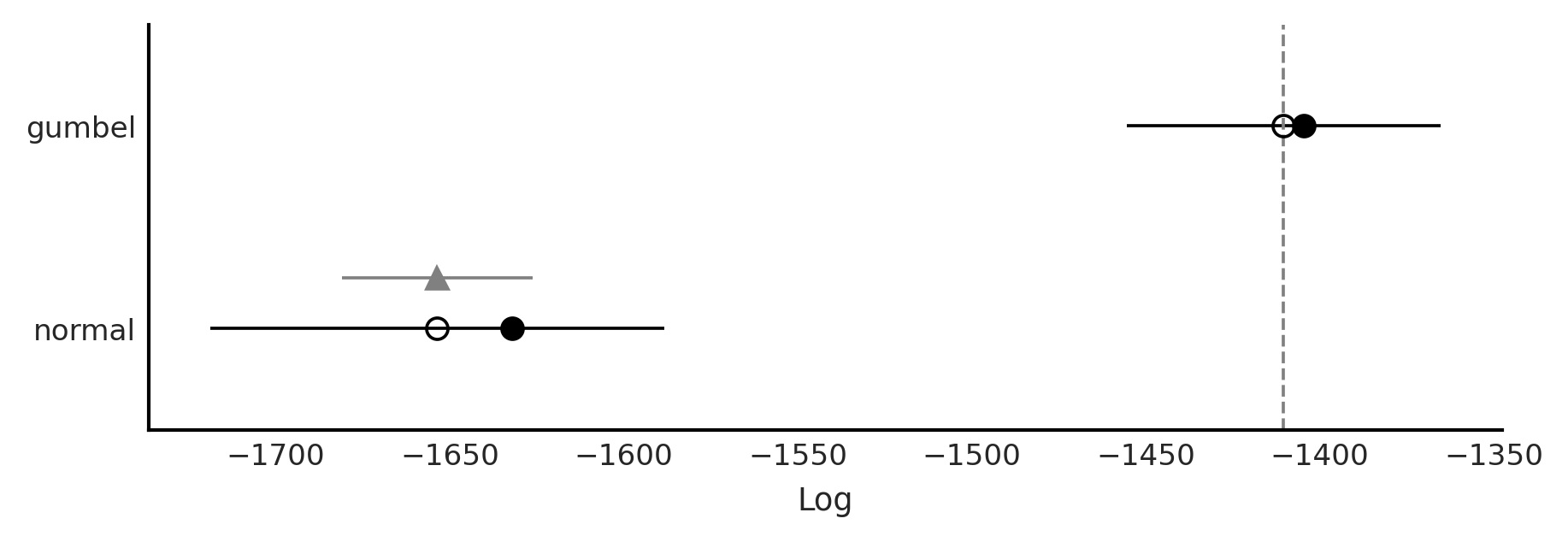

Code 9.7 and Figure 9.12#

az.plot_compare(cmp)

plt.savefig("img/chp09/model_comparison_airlines.png")

Figure 9.12#

/home/canyon/miniconda3/envs/bmcp/lib/python3.9/site-packages/arviz/stats/stats.py:655: UserWarning: Estimated shape parameter of Pareto distribution is greater than 0.7 for one or more samples. You should consider using a more robust model, this is because importance sampling is less likely to work well if the marginal posterior and LOO posterior are very different. This is more likely to happen with a non-robust model and highly influential observations.

warnings.warn(

fig = plt.figure(figsize=(10, 6))

gs = fig.add_gridspec(2, 2)

ax = fig.add_subplot(gs[0, :])

ax1 = fig.add_subplot(gs[1, 0])

ax2 = fig.add_subplot(gs[1, 1])

diff = gumbel_loo.loo_i - normal_loo.loo_i

idx = np.abs(diff) > 4

x_values = np.where(idx)[0]

y_values = diff[idx].values

az.plot_elpd(cmp_dict, ax=ax)

for x, y, in zip(x_values, y_values):

if x != 158:

x_pos = x+4

else:

x_pos = x-15

ax.text(x_pos, y-1, x)

for label, elpd_data, ax in zip(("gumbel", "normal"),

(gumbel_loo, normal_loo), (ax1, ax2)):

az.plot_khat(elpd_data, ax=ax)

ax.set_title(label)

idx = elpd_data.pareto_k > 0.7

x_values = np.where(idx)[0]

y_values = elpd_data.pareto_k[idx].values

for x, y, in zip(x_values, y_values):

if x != 158:

x_pos = x+10

else:

x_pos = x-30

ax.text(x_pos, y, x)

# ttl = ax.title

# ttl.set_position([.5, 10])

ax1.set_ylim(ax2.get_ylim())

ax2.set_ylabel("")

ax2.set_yticks([])

plt.savefig('img/chp09/elpd_plot_delays.png');

/home/canyon/miniconda3/envs/bmcp/lib/python3.9/site-packages/arviz/stats/stats.py:655: UserWarning: Estimated shape parameter of Pareto distribution is greater than 0.7 for one or more samples. You should consider using a more robust model, this is because importance sampling is less likely to work well if the marginal posterior and LOO posterior are very different. This is more likely to happen with a non-robust model and highly influential observations.

warnings.warn(

Reward Functions and Decisions#

posterior_pred = gumbel_data.posterior_predictive["delays"].values.reshape(-1, 336).copy()

Code 9.8#

@np.vectorize

def current_revenue(delay):

"""Calculates revenue """

if delay >= 0:

return 300*delay

return np.nan

Code 9.9#

def revenue_calculator(posterior_pred, revenue_func):

revenue_per_flight = revenue_func(posterior_pred)

average_revenue = np.nanmean(revenue_per_flight)

return revenue_per_flight, average_revenue

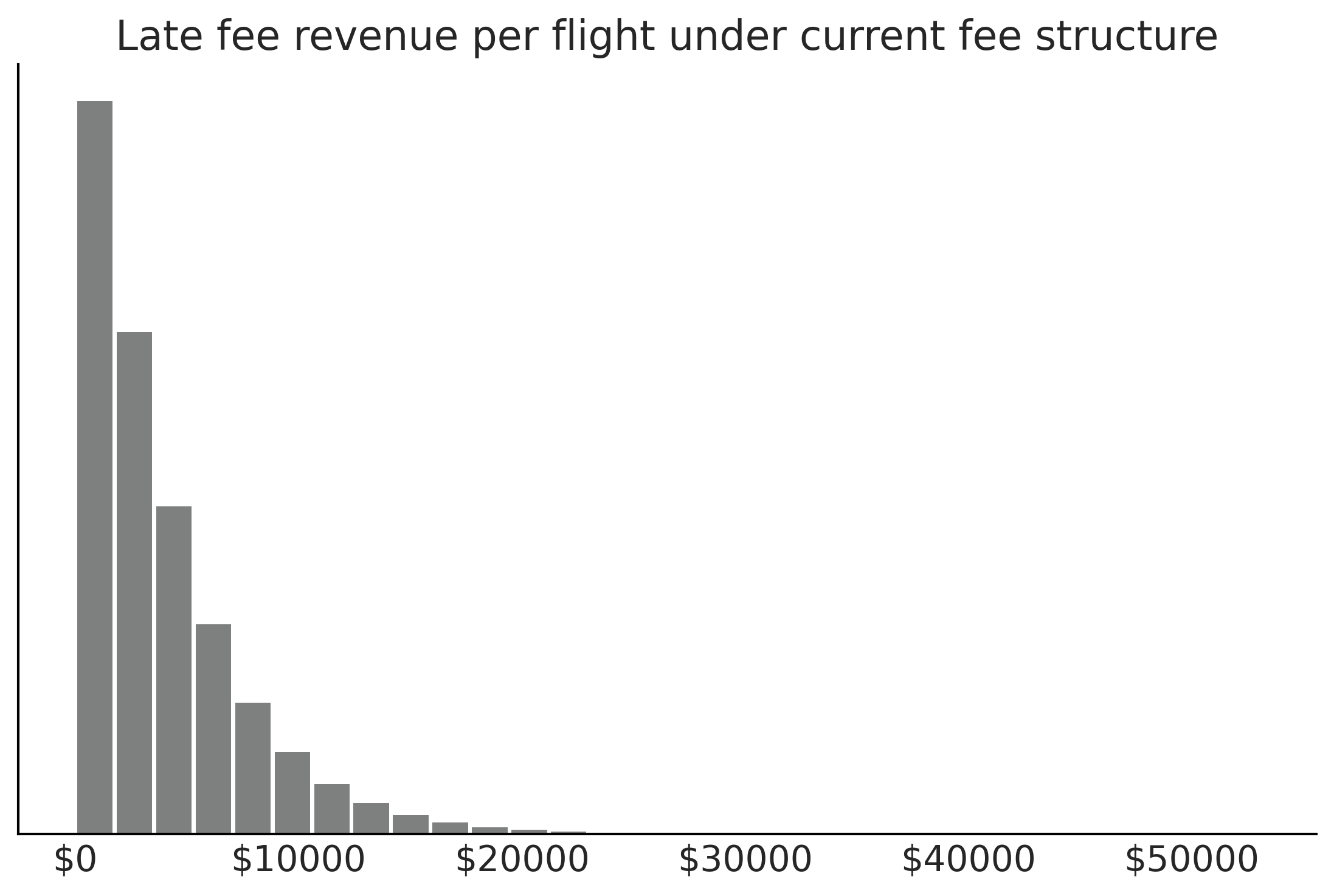

revenue_per_flight, average_revenue = revenue_calculator(posterior_pred, current_revenue)

average_revenue

3930.8899204759587

Figure 9.13#

fig, ax = plt.subplots()

ax.hist(revenue_per_flight.flatten(), bins=30, rwidth=.9, color="C2" )

ax.set_yticks([])

ax.set_title("Late fee revenue per flight under current fee structure")

ax.xaxis.set_major_formatter('${x:1.0f}')

plt.savefig("img/chp09/late_fee_current_structure_hist.png")

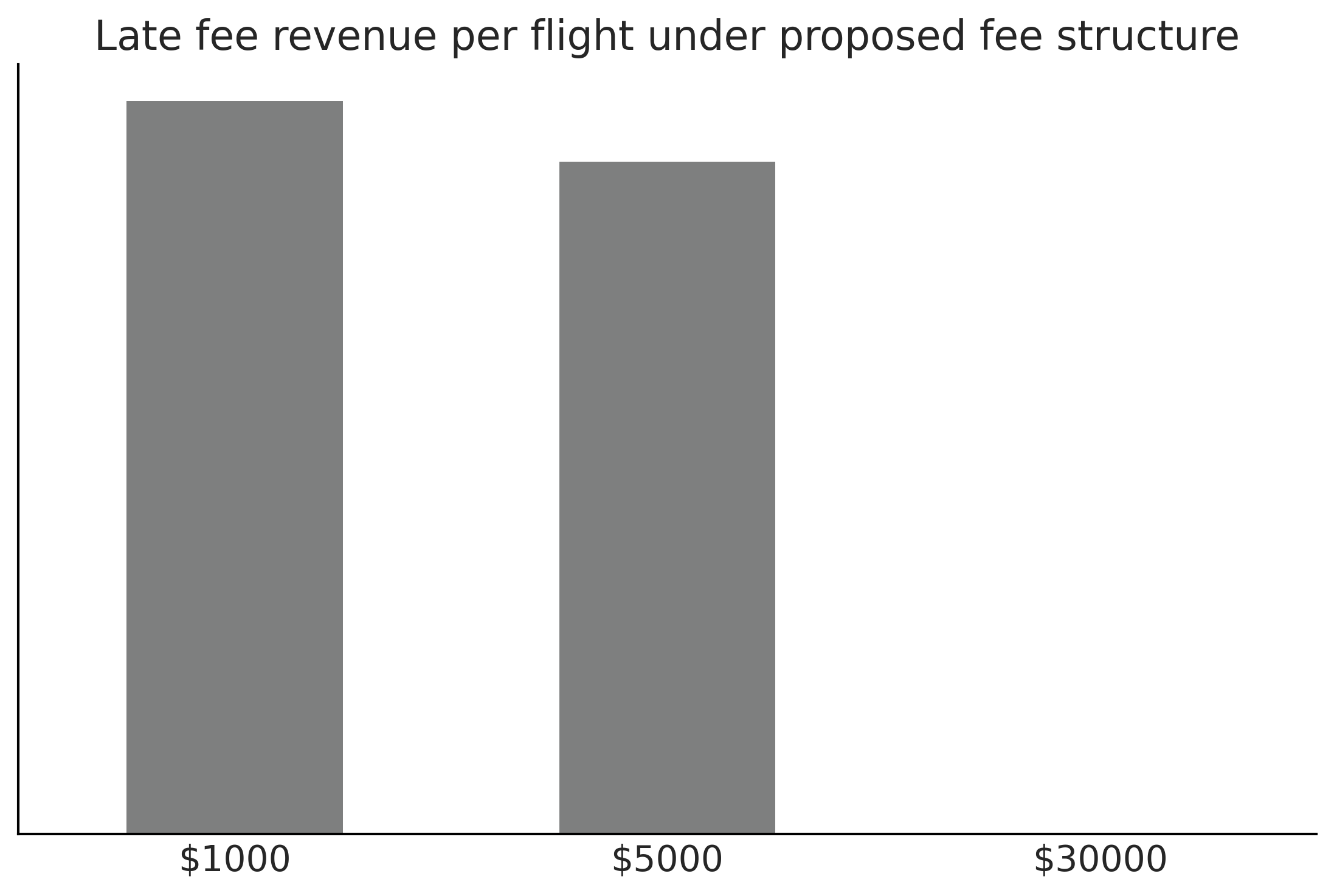

Code 9.10#

@np.vectorize

def proposed_revenue(delay):

"""Calculates revenue """

if delay >= 100:

return 30000

elif delay >= 10:

return 5000

elif delay >= 0:

return 1000

else:

return np.nan

revenue_per_flight_proposed, average_revenue_proposed = revenue_calculator(posterior_pred, proposed_revenue)

average_revenue_proposed

2921.977902254481

Sharing the Results With a Particular Audience#

Figure 9.14#

fig, ax = plt.subplots()

counts = pd.Series(revenue_per_flight_proposed.flatten()).value_counts()

counts.index = counts.index.astype(int)

counts.plot(kind="bar", ax=ax, color="C2")

ax.set_title("Late fee revenue per flight under proposed fee structure")

ax.set_yticks([]);

ax.tick_params(axis='x', labelrotation = 0)

ax.set_xticklabels([f"${i}" for i in counts.index])

plt.savefig("img/chp09/late_fee_proposed_structure_hist.png");

Table 9.2#

counts

1000 1110310

5000 1018490

30000 648

dtype: int64

counts/counts.sum()*100

1000 52.140743

5000 47.828827

30000 0.030430

dtype: float64

Experimental Example: Comparing Between Two Groups#

composites_df = pd.read_csv("../data/CompositeTensileTest.csv")

unidirectional = composites_df["Unidirectional Ultimate Strength (ksi)"].values

bidirectional = composites_df["Bidirectional Ultimate Strength (ksi)"].values

Code 9.11#

with pm.Model() as unidirectional_model:

sd = pm.HalfStudentT("sd_uni", 20)

mu = pm.Normal("mu_uni", 120, 30)

uni_ksi = pm.Normal("uni_ksi", mu=mu, sd=sd, observed=unidirectional)

# prior_uni = pm.sample_prior_predictive()

trace = pm.sample(draws=5000)

uni_data = az.from_pymc3(trace=trace)

/tmp/ipykernel_141130/4059400571.py:8: FutureWarning: In v4.0, pm.sample will return an `arviz.InferenceData` object instead of a `MultiTrace` by default. You can pass return_inferencedata=True or return_inferencedata=False to be safe and silence this warning.

trace = pm.sample(draws=5000)

Auto-assigning NUTS sampler...

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [mu_uni, sd_uni]

100.00% [24000/24000 00:03<00:00 Sampling 4 chains, 0 divergences]

Sampling 4 chains for 1_000 tune and 5_000 draw iterations (4_000 + 20_000 draws total) took 4 seconds.

/home/canyon/miniconda3/envs/bmcp/lib/python3.9/site-packages/arviz/data/io_pymc3.py:96: FutureWarning: Using `from_pymc3` without the model will be deprecated in a future release. Not using the model will return less accurate and less useful results. Make sure you use the model argument or call from_pymc3 within a model context.

warnings.warn(

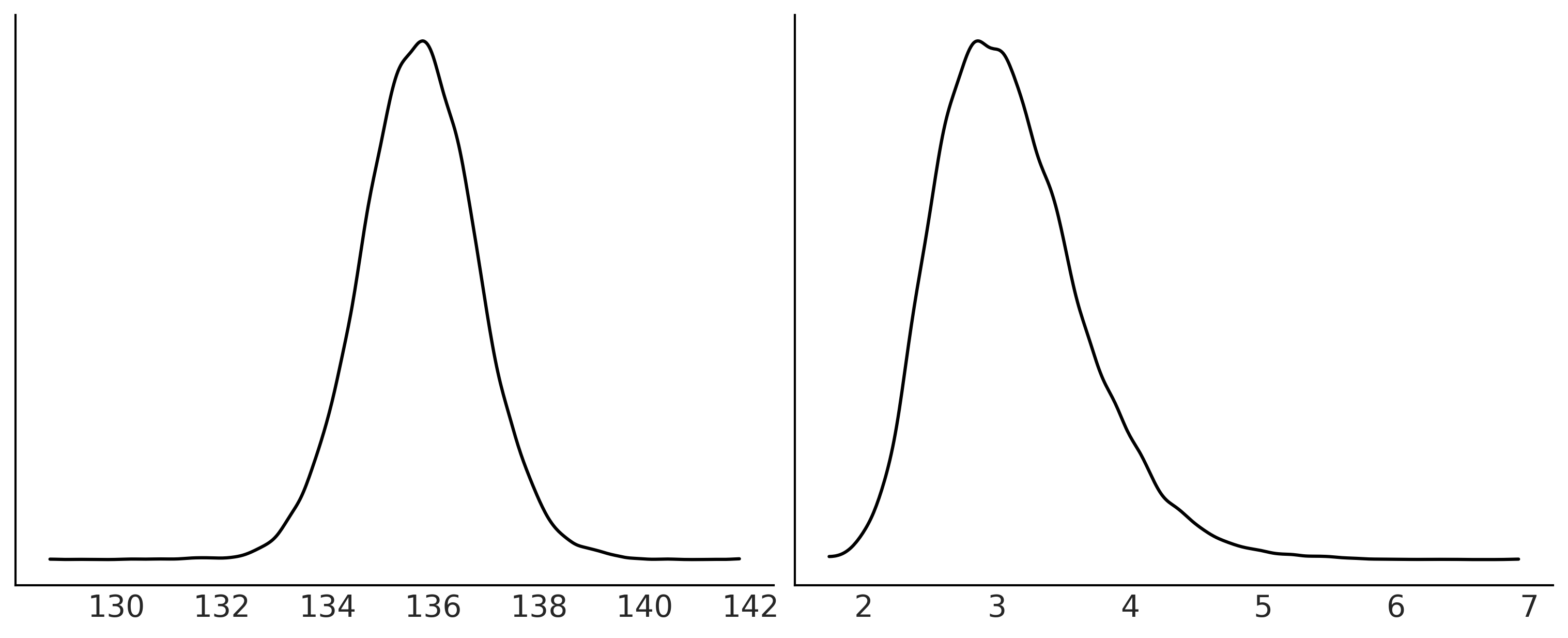

fig, axes = plt.subplots(1, 2, figsize=(10, 4))

az.plot_kde(uni_data.posterior["mu_uni"], ax=axes[0]);

az.plot_kde(uni_data.posterior["sd_uni"], ax=axes[1]);

axes[0].set_yticks([])

axes[1].set_yticks([])

fig.savefig("img/chp09/kde_uni.png")

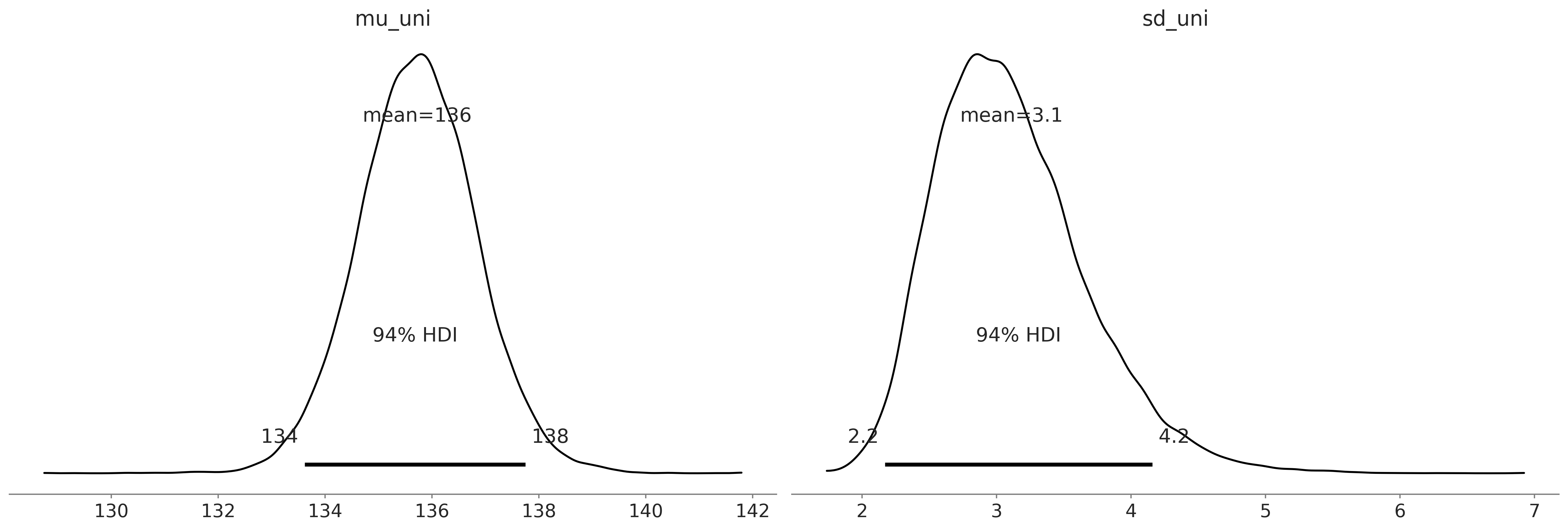

Code 9.12 and Figure 9.15#

az.plot_posterior(uni_data);

plt.savefig("img/chp09/posterior_uni.png")

Code 9.13#

μ_m = 120

μ_s = 30

σ_low = 10

σ_high = 30

with pm.Model() as model:

uni_mean = pm.Normal('uni_mean', mu=μ_m, sd=μ_s)

bi_mean = pm.Normal('bi_mean', mu=μ_m, sd=μ_s)

uni_std = pm.Uniform('uni_std', lower=σ_low, upper=σ_high)

bi_std = pm.Uniform('bi_std', lower=σ_low, upper=σ_high)

ν = pm.Exponential('ν_minus_one', 1/29.) + 1

λ1 = uni_std**-2

λ2 = bi_std**-2

group1 = pm.StudentT('uni', nu=ν, mu=uni_mean, lam=λ1, observed=unidirectional)

group2 = pm.StudentT('bi', nu=ν, mu=bi_mean, lam=λ2, observed=bidirectional)

diff_of_means = pm.Deterministic('Difference of Means', uni_mean - bi_mean)

diff_of_stds = pm.Deterministic('Difference of Stds', uni_std - bi_std)

effect_size = pm.Deterministic('Effect Size',

diff_of_means / np.sqrt((uni_std**2 + bi_std**2) / 2))

t_trace = pm.sample(draws=10000)

compare_data = az.from_pymc3(trace)

/tmp/ipykernel_141130/3744684942.py:27: FutureWarning: In v4.0, pm.sample will return an `arviz.InferenceData` object instead of a `MultiTrace` by default. You can pass return_inferencedata=True or return_inferencedata=False to be safe and silence this warning.

trace = pm.sample(draws=10000)

Auto-assigning NUTS sampler...

Initializing NUTS using jitter+adapt_diag...

Multiprocess sampling (4 chains in 4 jobs)

NUTS: [ν_minus_one, bi_std, uni_std, bi_mean, uni_mean]

100.00% [44000/44000 00:10<00:00 Sampling 4 chains, 0 divergences]

Sampling 4 chains for 1_000 tune and 10_000 draw iterations (4_000 + 40_000 draws total) took 12 seconds.

/home/canyon/miniconda3/envs/bmcp/lib/python3.9/site-packages/arviz/data/io_pymc3.py:96: FutureWarning: Using `from_pymc3` without the model will be deprecated in a future release. Not using the model will return less accurate and less useful results. Make sure you use the model argument or call from_pymc3 within a model context.

warnings.warn(

Code 9.14#

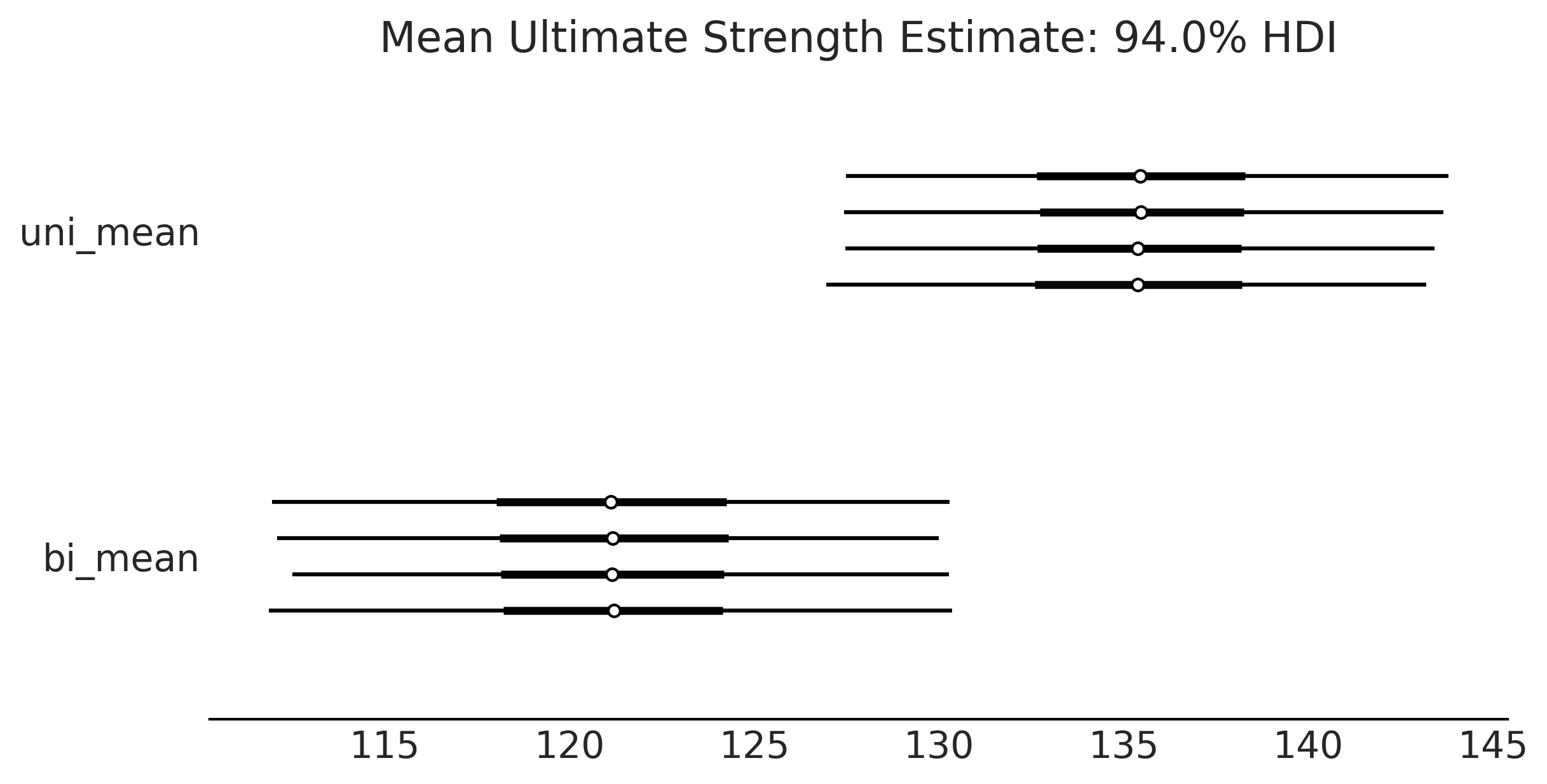

axes = az.plot_forest(trace, var_names=['uni_mean','bi_mean'], figsize=(8, 4));

axes[0].set_title("Mean Ultimate Strength Estimate: 94.0% HDI")

plt.savefig("img/chp09/Posterior_Forest_Plot.png")

Code 9.15 and Figure 9.17#

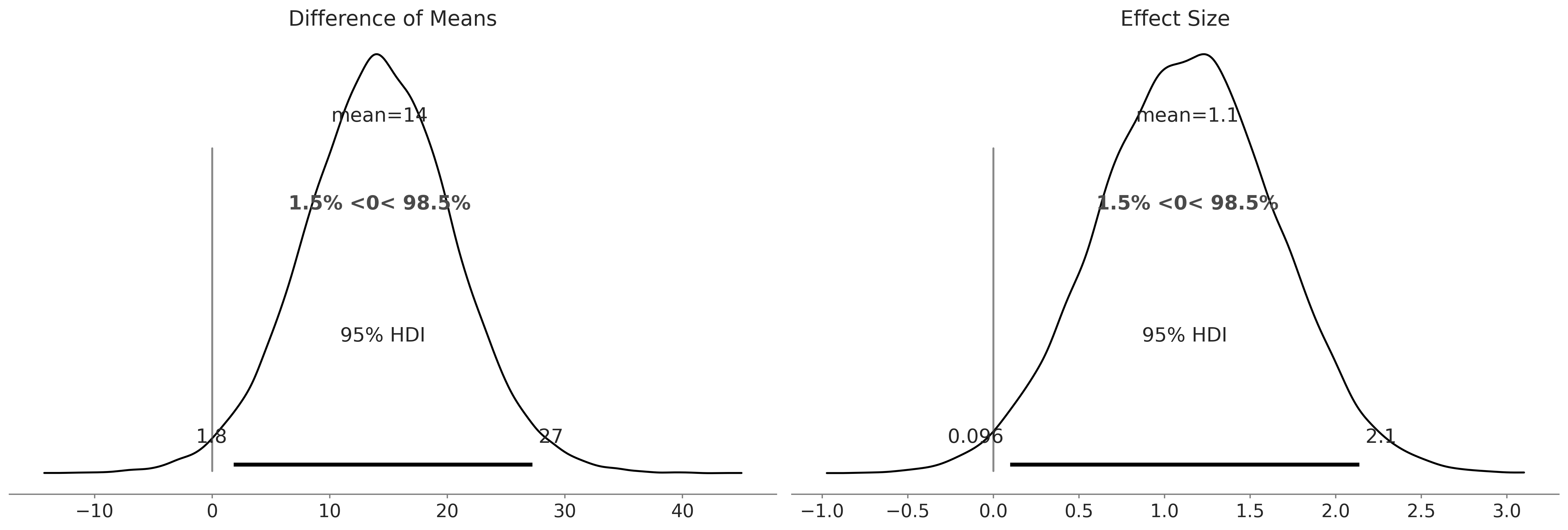

az.plot_posterior(trace, var_names=['Difference of Means','Effect Size'], hdi_prob=.95, ref_val=0);

plt.savefig("img/chp09/composite_difference_of_means.png")

/home/canyon/miniconda3/envs/bmcp/lib/python3.9/site-packages/arviz/data/io_pymc3.py:96: FutureWarning: Using `from_pymc3` without the model will be deprecated in a future release. Not using the model will return less accurate and less useful results. Make sure you use the model argument or call from_pymc3 within a model context.

warnings.warn(

Code 9.16#

az.summary(t_trace, kind="stats")

/home/canyon/miniconda3/envs/bmcp/lib/python3.9/site-packages/arviz/data/io_pymc3.py:96: FutureWarning: Using `from_pymc3` without the model will be deprecated in a future release. Not using the model will return less accurate and less useful results. Make sure you use the model argument or call from_pymc3 within a model context.

warnings.warn(

| mean | sd | hdi_3% | hdi_97% | |

|---|---|---|---|---|

| uni_mean | 135.419 | 4.302 | 127.457 | 143.675 |

| bi_mean | 121.188 | 4.806 | 112.111 | 130.283 |

| uni_std | 12.197 | 2.450 | 10.000 | 16.550 |

| bi_std | 13.268 | 3.229 | 10.000 | 19.283 |

| ν_minus_one | 36.507 | 30.447 | 0.218 | 92.225 |

| Difference of Means | 14.232 | 6.434 | 1.831 | 26.158 |

| Difference of Stds | -1.071 | 4.073 | -9.935 | 6.548 |

| Effect Size | 1.133 | 0.522 | 0.127 | 2.083 |